Philips 2005 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2005 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

Philips Annual Report 2005134

Accounting policies

Theconsolidatednancialstatementsarepreparedinaccordancewith

generally accepted accounting principles in the United States (US GAAP).

Historical cost is used as the measurement basis unless otherwise indicated.

Consolidation principles

Theconsolidatednancialstatementsincludetheaccountsof

Koninklijke Philips Electronics N.V. (the ‘Company’) and all entities in

which a direct or indirect controlling interest exists through voting

rights or qualifying variable interests. All intercompany balances

andtransactionshavebeeneliminatedintheconsolidatednancial

statements. Net income is reduced by the portion of the earnings of

subsidiaries applicable to minority interests. The minority interests are

disclosed separately in the consolidated statements of income and in

the consolidated balance sheets.

The Company applies Financial Accounting Standards Board (FASB)

Interpretation No. 46(R) ‘Consolidation of Variable Interest Entities’. In

accordance with Interpretation of Accounting Research Bulletin No. 51

‘Consolidated Financial Statements’, the Company consolidates entities

in which variable interests are held to an extent that would require the

Company to absorb a majority of the entity’s expected losses, receive a

majority of the entity’s expected residual returns, or both.

Investments in unconsolidated companies

Investments in companies in which the Company does not have the

abilitytodirectlyorindirectlycontrolthenancialandoperating

decisions,butdoespossesstheabilitytoexertsignicantinuence,are

accounted for using the equity method. Generally, in the absence of

demonstrableproofofsignicantinuence,itispresumedtoexistifat

least 20% of the voting stock is owned. The Company’s share of the net

income of these companies is included in results relating to unconsolidated

companies in the consolidated statements of income. The Company

recognizes an impairment loss when an other-than-temporary decline in

the value of an investment occurs. When the Company’s share of losses

exceeds the carrying amount of an investment accounted for by the

equity method, the Company’s carrying amount of that investment is

reduced to zero and recognition of further losses is discontinued unless

the Company has guaranteed obligations of the investee or is otherwise

committedtoprovidefurthernancialsupportfortheinvestee.

Accounting for capital transactions of a subsidiary or an

unconsolidated company

The Company recognizes dilution gains or losses arising from the sale

or issuance of stock by a consolidated subsidiary or an unconsolidated

entity which the Company is accounting for using the equity method

of accounting in the income statement, unless the Company or the

subsidiary either has reacquired or plans to reacquire such shares. In

such instances, the result of the transaction will be recorded directly

in stockholders’ equity as a non-operating gain or loss.

The dilution gains or losses are presented in the income statement

under Other business income (expenses) if they relate to consolidated

subsidiaries. Dilution gains and losses related to unconsolidated companies

are presented under Results relating to unconsolidated companies.

Foreign currencies

Thenancialstatementsofforeignentitiesaretranslatedintoeuros.

Assets and liabilities are translated using the exchange rates on the

respective balance sheet dates. Income and expense items in the income

statementandcashowstatementaretranslatedatweightedaverage

exchange rates during the year. The resulting translation adjustments

are recorded as a separate component of other comprehensive income

(loss) within stockholders’ equity. Cumulative translation adjustments

are recognized as income or expense upon partial or complete disposal

or substantially complete liquidation of a foreign entity.

The functional currency of foreign entities is generally the local currency,

unless the primary economic environment requires the use of another

currency. When foreign entities conduct their business in economies

consideredtobehighlyinationary,theyrecordtransactionsinthe

Company’s reporting currency (the euro) instead of their local currency.

Gains and losses arising from the translation or settlement of foreign-

currency-denominated monetary assets and liabilities into the local

currency are recognized in income in the period in which they arise.

However, currency differences on intercompany loans that have the

nature of a permanent investment are accounted for as translation

differences as a separate component of other comprehensive income

(loss) within stockholders’ equity.

Derivativenancialinstruments

TheCompanyusesderivativenancialinstrumentsprincipallyin

the management of its foreign currency risks and to a more limited

extent for interest rate and commodity price risks. In compliance

with Statement of Financial Accounting Standards (SFAS) No. 133,

‘Accounting for Derivative Instruments and Hedging Activities’, SFAS

No. 138, ‘Accounting for Certain Derivative Instruments and Certain

Hedging Activities’, and SFAS No. 149 ‘Amendment of Statement 133 on

Derivative Instruments and Hedging Activities’, the Company measures

allderivativenancialinstrumentsbasedonfairvaluesderivedfrom

market prices of the instruments or from option pricing models, as

appropriate. Gains or losses arising from changes in the fair value of

the instruments are recognized in the income statement during the

period in which they arise to the extent that the derivatives have been

designated as a hedge of recognized assets or liabilities, or to the extent

that the derivatives have no hedging designation or are ineffective. The

gains and losses on the designated derivatives substantially offset the

changes in the values of the recognized hedged items, which are also

recognized as gains and losses in the income statement.

Changes in the fair value of a derivative that is highly effective and that

isdesignatedandqualiesasafairvaluehedge,alongwiththelossor

gainonthehedgedasset,orliabilityorunrecognizedrmcommitment

of the hedged item that is attributable to the hedged risk, are recorded

in the income statement.

Changes in the fair value of a derivative that is highly effective and

thatisdesignatedandqualiesasacashowhedge,arerecordedin

accumulated other comprehensive income, until earnings are affected

bythevariabilityincashowsofthedesignatedhedgeditem.Changes

in the fair value of derivatives that are highly effective as hedges and

that are designated and qualify as foreign currency hedges are recorded

in either earnings or accumulated other comprehensive income,

depending on whether the hedge transaction is a fair value hedge or

acashowhedge.

The Company formally assesses, both at the hedge’s inception and on an

ongoing basis, whether the derivatives that are used in hedging transactions

arehighlyeffectiveinoffsettingchangesinfairvaluesorcashowsof

hedged items. When it is established that a derivative is not highly

effective as a hedge or that it has ceased to be a highly effective hedge,

the Company discontinues hedge accounting prospectively. When hedge

accounting is discontinued because it has been established that the

derivativenolongerqualiesasaneffectivefairvaluehedge,theCompany

continues to carry the derivative on the balance sheet at its fair value,

and no longer adjusts the hedged asset or liability for changes in fair

value. When hedge accounting is discontinued because it is probable

that a forecasted transaction will not occur within a period of two

months from the originally forecasted transaction date, the Company

continues to carry the derivative on the balance sheet at its fair value,

and gains and losses that were accumulated in other comprehensive

income are recognized immediately in earnings. In all other situations

in which hedge accounting is discontinued, the Company continues to

carry the derivative at its fair value on the balance sheet, and recognizes

any changes in its fair value in earnings.

For interest rate swaps that are unwound, the gain or loss upon

unwinding is released to income over the remaining life of the underlying

nancialinstruments,basedontherecalculatedeffectiveyield.

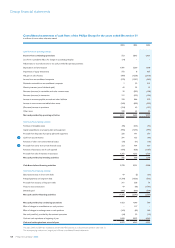

Cash and cash equivalents

Cash and cash equivalents include all cash balances and short-term

highly liquid investments with an original maturity of three months or

less that are readily convertible into known amounts of cash. They are

stated at face value.

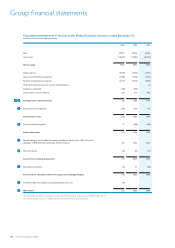

Groupnancialstatements