Philips 2005 Annual Report Download - page 190

Download and view the complete annual report

Please find page 190 of the 2005 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

Philips Annual Report 2005190

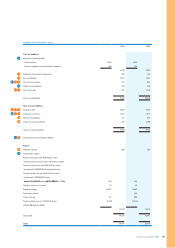

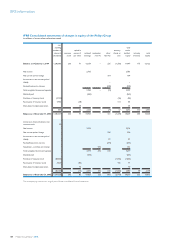

Cashowstatements

Cashowstatementshavebeenpreparedusingtheindirectmethod

in accordance with the requirements of IAS 7 ‘Cash Flow Statements’.

Cashowsinforeigncurrencieshavebeentranslatedintoeurosusing

the weighted average rates of exchange for the periods involved.

Cashowsfromderivativeinstrumentsthatareaccountedforasfair

valuehedgesorcashowhedgesareclassiedinthesamecategory

asthecashowsfromthehedgeditems.Cashowsfromderivative

instruments for which hedge accounting has been discontinued are

classiedconsistentwiththenatureoftheinstrumentasfromthe

date of discontinuance.

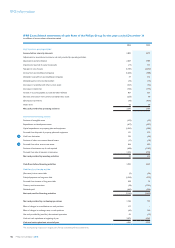

Use of estimates

Thepreparationofnancialstatementsrequiresmanagementtomake

estimates and assumptions that affect amounts reported in the consolidated

nancialstatementsinordertoconformtogenerallyacceptedaccounting

principles. Actual results could differ from those estimates.

Application of IFRS 1

With regard to the options that are offered in IFRS 1 ‘First-time Adoption

of International Financial Reporting Standards’ the Company has chosen

to use the options that are offered by IFRS 1 as described below.

ForemployeebenetsunderIAS19‘EmployeeBenets’theCompany

has chosen to recognize all cumulative actuarial gains and losses at

January 1, 2004. In accordance with IFRS 1 such recognition has

occurred directly in equity.

The cumulative translation differences related to foreign entities

within equity are deemed to be zero at January 1, 2004. Accordingly,

these cumulative translation differences were included in retained

earnings in the IFRS opening balance sheet. This also will have the

effect that upon disposal of a foreign entity only cumulative translation

differences that arose after January 1, 2004 can be recognized in the

result upon disposal.

Business combinations that were recognized before January 1, 2004

will not be restated to IAS 22/IFRS 3 ‘Business Combinations’.

Share-based payment transactions that were granted on or before

November 7, 2002 are recognized in accordance with the

requirements of standard IFRS 2 ‘Share-based payments’, which is

effective as from that date. Consequently, the Company applies the

exemption as offered by IRFS 1 to apply IFRS 2 to all share-based

payment grants that had not vested as at the date of transition to IFRS.

•

•

•

•

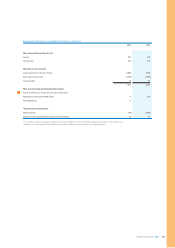

New IFRS accounting standards

The IASB and its interpretation committee IFRIC issued several

pronouncements during 2005, of which the following are applicable to

the Company.

In April 2005 the IASB issued an amendment to IAS 39 under the

heading “Cash Flow Hedge Accounting of Forecast Intragroup

Transactions”. The amendment allows hedge accounting for highly

probableforecastintragrouptransactionsinconsolidatednancial

statements. The Company adopted this amendment and applied the early

application provision to all periods presented. The effect of application

ofthisamendmenttotheIFRSnancialstatementsisnotmaterial.

In August 2005 the IASB issued the new Standard IFRS 7 ‘Financial

Instruments’: Disclosures. The standard requires disclosure of the

signicanceofnancialinstrumentsforanentity’spositionand

performance, and qualitative and quantitative information on risks arising

fromnancialinstruments.TheStandardbecomeseffectivefrom2007

onwards. The effect on the Company’s disclosure is expected to be

limited because many of the required disclosures are already supplied.

In September 2005 the IASB’s interpretation committee IFRIC issued

Interpretation6‘LiabilitiesarisingfromParticipatinginaSpecicMarket

– Waste Electrical and Electronic Equipment’. This Interpretation concerns

the recognition of liabilities resulting from the European Union’s

Directive on Waste Electrical and Electronic Equipment (WEEE), which

came into effect on February 13, 2003. Member States were required

to transform the Directive into national law by August 13, 2004. Under

this Directive, costs of disposing of electrical and electronic equipment

used by households in an environmentally acceptable manner are borne

by producers. The Directive stipulates that the producers of that type of

equipmentwhoareinthemarketinaperiodspeciedintheapplicable

nationallegislation(themeasurementperiod)mustnancecostsrelated

to waste management for equipment that was sold to private households

before August 13, 2005, the so-called historical waste. For other waste,

such as related to equipment sold after August 13, 2005 (future waste)

or equipment sold to others than households, the Directive provides

thatproducersareresponsiblefornancingwastemanagementcosts.

The Directive allows the Member States to allow producers to charge

theircustomersavisiblefeefornancingwastemanagement.

IFRIC Interpretation 6 is solely related to historical waste and has

mandated that no liability shall arise for historical waste held by

private households other than for waste costs for equipment in the

measurement period.

The Company is a provider of equipment that falls under the EU

Directive, particularly in the segments Lighting, Consumer Electronics,

Domestic Appliances and Personal Care, and Medical Systems. As at the

endof2005,anumberofstatesincludingsignicantEUMemberStates

did not yet have their national legislation in place. Accordingly, the

Company was not able to reliably estimate all effects of the WEEE

Directive with respect to future waste. In as far as the historical waste is

concerned, which is covered by Interpretation 6, the Company concluded

that the effects on the income statement are not material as at the end

of 2005. This is mainly caused by the fact that the costs are compensated

by fees charged to the customers. Also for the coming years the effects

are estimated to be limited on the assumption that all Member States

will allow visible fees to be charged to the customers. With respect to

future waste, however, the effects may become material over time, as

we will have to reserve for waste management costs for all products

that fall under the Directive and that were or will be sold after the

dates of enactment in local laws of the EU Member States. Over the

next years when products will be returned and disposed, the estimated

cost of future waste management is expected to increase as a function

of the expected life of the products and return rates. These expected

costs will be charged to the income statement and a provision will be

made in the balance sheet in as far amounts can be reliably estimated

andrepresentexpectedoutowsofassetsfortheCompany.

IFRS information