Philips 2005 Annual Report Download - page 191

Download and view the complete annual report

Please find page 191 of the 2005 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

Philips Annual Report 2005 191

Reconciliation from IFRS to US GAAP and Dutch GAAP

Previously, under Dutch law (Book 2, Title 9, Netherlands Civil Code referred to as Dutch GAAP) the Company reported single company and

consolidatednancialstatements.ThereforethesenancialstatementsrepresentthepreviousGAAPnancialstatementsasreferredtoinIFRS1

paragraph38.TheCompanyprovidesbothinaccordancewithIFRS1andfortransparencypurposesfortheusersofthenancialstatements,the

following reconciliations from IFRS to US GAAP and Dutch GAAP.

Reconciliation from IFRS to US GAAP

The major differences between IFRS and US GAAP that affect stockholders’ equity and net income are the following:

IFRS requires capitalization and subsequent amortization of development cost if the relevant conditions for capitalization are met, whereas

development cost under US GAAP is recorded as an expense.

StandardsforpensionaccountingaresubstantiallythesameinbothUSGAAPandIFRS.However,onrst-timeadoption,IFRS1allows

recognition of cumulative actuarial gains and losses as per January 1st, 2004. Furthermore, the so-called additional minimum pension liabilities

recognized under US GAAP do not exist in IFRS and IFRS has stricter rules than US GAAP for the recognition of prepaid pension assets.

Under IFRS, goodwill is not amortized as from 2004. Since goodwill was no longer amortized as from 2002 under US GAAP, IFRS has two

additional years of goodwill amortization. This is also a reason for differences in unconsolidated companies under IFRS and US GAAP.

IFRSrequiresup-frontprotrecognitionofoperationalsale-and-leasebacktransactionswhenthesaleisatmarketconditions,whereas

US GAAP requires amortization.

The differences as explained above affect income taxes and therefore deferred income taxes.

The composition of equity under IFRS is affected by the exemption of IFRS 1 that allows including the existing negative cumulative translation

differences of EUR 3.4 billion in retained earnings as per January 1, 2004. As a result of the application of this exemption, the recycling of

translation gains and losses from equity to the income statement differs when comparing US GAAP and IFRS. For 2005, this mainly affected

the results unconsolidated companies.

Reconciliation from US GAAP to Dutch GAAP

For the determination of net income and stockholders’ equity in accordance with Dutch GAAP, the following differences with US GAAP have been

taken into account:

Under US GAAP, SFAS No. 142, goodwill is no longer amortized but is tested for impairment on an annual basis and whenever indicators of

impairment arise. Under Dutch GAAP, goodwill is amortized on a straight-line basis not exceeding 20 years. As a consequence, goodwill

amortization and impairment charges under Dutch GAAP may be different from US GAAP.

Dutch law requires that previously recognized impairment charges for available-for-sale securities are reversed through income when the fair

value of these securities increases to a level that is above the new cost price that was established on recognition of an impairment. In view of this

requirement,other-than-temporaryincreasesinfairvalueofavailable-for-salesecuritiesarerecognizedinnancialincome.USGAAPprohibits

such recognition.

•

•

•

•

•

•

•

•

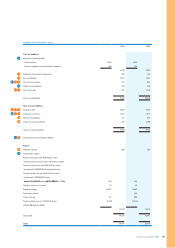

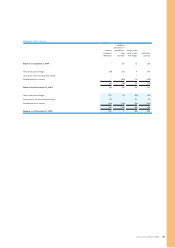

Reconciliation of net income from IFRS to US GAAP and Dutch GAAP

in millions of euros 2004 2005

Net income as per the consolidated statements of

income on an IFRS basis 2,783 3,374

Adjustments to reconcile to US GAAP:

Reversal of c

apitalized product development cost (617) (697)

Reversal of amortization of product development assets

412 467

Reversal of

additional net pensions and other charges 150 114

Financial income and expenses 182 (5)

Adjustment of results of unconsolidated companies (34) (524)

Income tax effect on IFRS adjustments (4) 29

Discontinued operations (15) 91

Other (21) 19

Net income as per the consolidated statements of

income on a US GAAP basis 2,836 2,868

Adjustments to reconcile to Dutch GAAP:

Goodwill amortization net of taxes (439)

Lower impairment charges due to amortization of

goodwill 68

Adjustment on gain on sale of securities/shares due

to lower book value:

-nancialincomeandexpenses (202)

- results relating to unconsolidated companies 34

Reversal of impairment of available-for-sale securities 19

Higher dilution gain LG.Philips LCD due to

amortization of goodwill 20

Net income as per the consolidated statement of

income on a Dutch GAAP basis 2,336

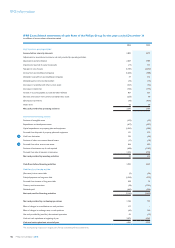

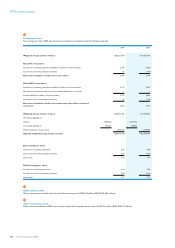

Reconciliation of stockholders’ equity from IFRS to US and Dutch GAAP

in millions of euros Jan. 1,

2004

Dec. 31,

2004

Dec. 31,

2005

Stockholders’ equity as per the

consolidated balance sheets on an IFRS basis

11,947 14,239 16,319

Adjustments to reconcile to US GAAP:

Reversal of capitalized product

development cost (1,212) (1,409) (1,668)

Reversal of pensions and other

postretirementbenets 1,724 1,701 1,749

Goodwill amortization

(until January 1, 2004) 395 355 404

Goodwill capitalization (acquisition-related)

− − 40

Acquisition-related intangibles − − (294)

Unconsolidated companies 234 230 178

Reversal of result recognition sale and

leaseback (107) (102) (80)

Deferred tax effect (201) (123) (57)

Discontinued operations (20) (33) 51

Other 3 2 24

Stockholders’ equity as per the

consolidated balance sheets on a US

GAAP basis 12,763 14,860 16,666

Adjustments to reconcile to Dutch GAAP:

Goodwill amortization net of taxes (1,483) (1,922)

Lower impairment charges due to

amortization of goodwill 746 814

Higher dilution gain LG.Philips LCD due

to amortization of goodwill −20

Adjustment on gain of sale of Atos

Origin shares due to lower book value −34

Adjustment on increase of fair value

securities in connection with lower

book value −32

Translation differences 142 178

Stockholders’ equity as per the

consolidated balance sheets on a Dutch

GAAP basis 12,168 14,016