RBS 2007 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

11

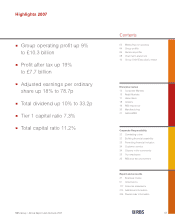

RBS Group • Annual Report and Accounts 2007

For The Royal Bank of Scotland Group, 2007 was

defined by another strong operating performance

and by the acquisition of ABN AMRO.

The diversity and quality of our business platform

enabled us to deliver good financial results, with

operating profit for the enlarged RBS Group rising

by 9% to £10,282 million. Our earnings momentum

remained powerful, notwithstanding the impact of

challenging credit market conditions in the second

half of the year.

Our results demonstrate the resilience of the Group in the face

of testing circumstances. The summer floods came during the

wettest May to July in England and Wales since records began

in 1766. While RBS Insurance responded magnificently to meet

the needs of customers in distress, the impact on profits is

evident. The pace of activity in the US slowed as the housing

market weakened, leading to challenging conditions for Global

Banking & Markets (‘GBM’) and Citizens. Later in the summer

began the dislocation in credit markets, which made the second

half a turbulent period for the financial services sector.

Delivering such a robust financial performance in this

environment is the consequence of action in two areas: over

a number of years we have diversified the Group’s income

streams and last year also saw us benefit from our focus on

credit quality and risk management with our impairments,

excluding ABN AMRO, down 1%.

Our customers and businesses

The Group now serves over 40 million customers in 53 countries

worldwide. In each of those markets we will continue our

relentless focus on customers’ needs.

GBM enjoyed another strong first half performance and took

full advantage of the volatility in the second half to deliver

excellent performances in interest rate and currency trading.

Inevitably, the second half witnessed significantly lower origination

volumes in credit markets and write-downs on US mortgage-

related exposures. Our UK Corporate Banking business enjoyed

another very successful year maintaining its consistent record

of high single-figure income growth and further advancing its

market share from a position of leadership. By continuing to invest

in service quality we have achieved market-leading customer

satisfaction scores and customer numbers increased by 4%.

Retail delivered strong growth in savings and investment

products while maintaining a cautious approach to unsecured

credit. Our success is built on customer satisfaction, and on

this metric RBS and NatWest maintained their lead over the

other major high street banks. Wealth Management’s trajectory

remains very strong. We continued to expand Coutts UK’s

regional franchise and achieved significant growth in Asia-Pacific.

Ulster Bank maintained its strong growth record and we have

continued to invest in the good opportunities for future growth

presented by the Irish market. Citizens further developed its

franchise, increasing its consumer banking customer base by

2% and achieving good results in its growing corporate and

commercial banking operations.

In RBS Insurance, we have built on our strong position as

the UK’s leading personal lines insurer by further sharpening

our focus on selective underwriting of the more profitable

segments, reducing volumes in others. Of course, results were

held back by the floods, but excluding this, operating profit

grew strongly.

Manufacturing is central to the way we operate, underpinning

our determination to deliver service to our customers while

deriving scale benefits achievable from sharing infrastructure,

processes and services across our businesses. We held cost

growth to just 1%, despite continued investment in technology

and property to support increased transaction volumes and

the development of our business.

Capital

The Group’s Tier 1 capital ratio at 31 December was 7.3%

and our total capital ratio 11.2%, within our target ranges.

At the time of the bid for ABN AMRO we indicated our intention

to rebuild our capital ratios. We remain committed to this goal,

and the improved financial returns now expected on the

acquisition will help to accelerate delivery of the Group’s

capital regeneration commitments.

Positioned for growth

This decade has seen considerably stronger economic

growth in the developing world, especially Asia, than in the

West. Trade and capital flows have been the main drivers of

rising prosperity. This growth has spurred demand for many

commodities, notably energy. Within the dynamic Asian

economies, the number of wealthy people is growing and

around the world affluence is increasingly common.