RBS 2007 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

37

RBS Group • Annual Report and Accounts 2007

Business review

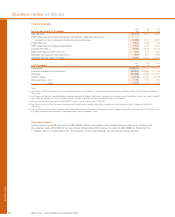

2006 compared with 2005

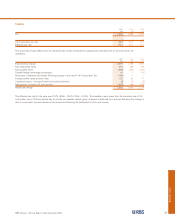

Profit

Profit before tax, purchased intangibles amortisation,

integration costs and net gain on sale of strategic investments

and subsidiaries increased by 14% or £1,163 million, from

£8,251 million to £9,414 million.

Profit before tax was up 16%, from £7,936 million to £9,186

million, reflecting strong organic income growth in all divisions.

Total income

The Group achieved strong growth in income during 2006.

Total income was up 10% or £2,433 million to £28,002 million.

Net interest income increased by 7% to £10,596 million and

represents 38% of total income (2005 – 39%). Average loans

and advances to customers and average customer deposits

grew by 14% and 11% respectively.

Non-interest income increased by 11% to £17,406 million and

represents 62% of total income (2005 – 61%).

Net interest margin

The Group’s net interest margin at 2.47% was down from

2.55% in 2005, due mainly to the business mix effect of growth

in corporate and mortgage lending and the impact of the

flatter US dollar yield curve.

Operating expenses

Operating expenses, excluding purchased intangibles

amortisation and integration costs, rose by 8% to £12,252 million.

Cost:income ratio

The Group’s cost:income ratio was 42.1% compared with

42.4% in 2005.

Net insurance claims

Bancassurance and general insurance claims, after

reinsurance, increased by 3% to £4,458 million reflecting

volume growth.

Impairment losses

Impairment losses were £1,878 million compared with £1,707

million in 2005, an increase of 10%.

Risk elements in lending and potential problem loans

represented 1.57% of gross loans and advances to customers

excluding reverse repos at 31 December 2006 (2005 – 1.60%).

Provision coverage of risk elements in lending and potential

problem loans was 62% compared with 65% at 31 December

2005. This reflects amounts written-off and the changing mix

from unsecured to secured exposures.

Integration

Integration costs were £134 million compared with £458 million

in 2005. Included are costs relating to the integration of First

Active and Charter One, as well as the amortisation of software

costs relating to the integration of Churchill. Integration costs in

2005 included software costs relating to the acquisition of

NatWest which were previously written-off as incurred under

UK GAAP but under IFRS were capitalised and amortised. All

such software was fully amortised by the end of 2005.

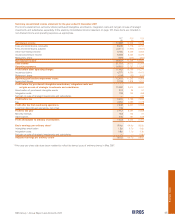

Earnings and dividends*

Basic earnings per ordinary share increased by 15%, from

56.5p to 64.9p. Earnings per ordinary share adjusted for

purchased intangibles amortisation, integration costs and net

gain on sale of strategic investments and subsidiaries

increased by 14%, from 58.6p to 66.7p.

A final dividend of 22.1p per ordinary share was paid, giving a

total dividend for the year of 30.2p, an increase of 25%. The

total dividend was covered 2.2 times by earnings before

purchased intangibles amortisation and integration costs.

*restated for the effect of the bonus issue of ordinary shares in

May 2007.

Balance sheet

Total assets were £871.4 billion at 31 December 2006, 12%

higher than total assets of £776.8 billion at 31 December 2005.

Lending to customers, excluding repurchase agreements and

stock borrowing (“reverse repos”), increased in 2006 by 10%

or £35.7 billion to £404.0 billion. Customer deposits, excluding

repurchase agreements and stock lending (“repos”), grew by

9% or £26.1 billion to £320.2 billion.

Capital ratios at 31 December 2006 were 7.5% (Tier 1) and

11.7% (Total).

Profitability

The adjusted after-tax return on ordinary equity, which is based

on profit attributable to ordinary shareholders before purchased

intangibles amortisation, integration costs and net gain on

sale of strategic investments and subsidiaries, and average

ordinary equity, was 19.0% compared with 18.2% in 2005.