RBS 2007 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

RBS Group • Annual Report and Accounts 2007

136

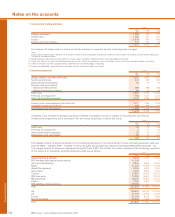

Accounting policies continued

Financial statements

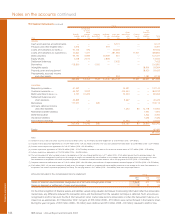

Syndicated loans – syndicated loans are valued by considering

recent syndication prices in the same or similar assets, prices in

the secondary loan market, and with reference to relevant indices

for credit products and credit default swaps such as the LevX,

LCDX, ITraxx and CDX. Assumptions relating to the expected

refinancing period are based on market experience and market

convention. Adjustments to observed prices are made for

differences between instruments, such as counterparty

creditworthiness, term, and quality of any collateral.

The fair value of drawn syndicated loans valued using

techniques other than by considering recent syndication prices

in the same or similar assets and prices in the secondary loan

market was £4,624 million. Using reasonably possible

alternative assumptions about refinancing periods (which were

stressed by one year) and the value attributed to potentially

favourable flexible loan conditions (which are attributed no

value in reported figures) would reduce the fair value by up to

£46 million or increase the fair value by up to £83 million.

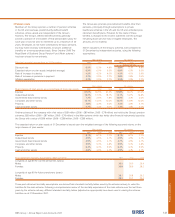

Commercial mortgages – senior and mezzanine commercial

mortgages are loans secured on commercial land and

buildings that were originated or acquired by the Group for

securitisation. Senior commercial mortgages carry a variable

interest rate and mezzanine or more junior commercial

mortgages may carry a fixed or variable interest rate. Factors

affecting the value of these loans may include, but are not

limited to, loan type, underlying property type and geographic

location, loan interest rate,

loan to value ratios, debt service coverage ratios, prepayment

rates, cumulative loan loss information, yields, investor

demand, market volatility since the last securitisation, and

credit enhancement.

Where observable market prices for a particular loan are not

available, the fair value will typically be determined with

reference to observable market transactions in other loans or

credit related products including debt securities and credit

derivatives. Assumptions are made about the relationship

between the loan and the available benchmark data. Using

reasonably possible alternative assumptions for credit spreads

(taking into account all other applicable factors) would reduce

the fair value by up to £52 million or increase the fair value by

up to £49 million.

Super senior tranches of asset-backed CDOs – the Group is a

participant in the US asset-backed securities market: buying

residential mortgage-backed securities (‘RMBS’), including

securities backed by US sub-prime mortgages, and

repackaging them into collateralised debt obligations (‘CDOs’)

for sale to investors. The Group retains exposure to some of

the super senior tranches of these CDOs. In the second half of

2007, rising mortgage delinquencies and expectations of

declining house prices in the US led to a deterioration of the

estimated fair value of these exposures.

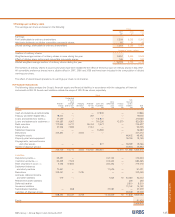

An analysis of the Group’s super senior tranche exposures to

these CDOs is shown below:

High grade Mezzanine

Exposure (£m) 6,420 3,040

Exposure after hedges (£m) 3,073 1,790

Weighted average attachment point (1) 29% 46%

% of underlying RMBS sub-prime assets 69% 91%

Of which originated in:

– 2005 and earlier 24% 23%

– 2006 28% 69%

– 2007 48% 8%

Collateral by rating:

– investment grade 98% 31%

– non-investment grade 2% 69%

Net exposure (£m) 2,581 1,253

Effective attachment point post write down 40% 62%

Note:

(1) Attachment point is the minimum level of losses in a portfolio to which a tranche is exposed, as a percentage of the total notional size of the portfolio. For example, a 5-10%

tranche has an attachment point of 5% and a detachment point of 10%. When the accumulated loss of the reference pool is no more than 5% of the total initial notional of the

pool, the tranche will not be affected. However, when the loss has exceeded 5%, any further loss will be deducted from the tranche’s notional principal until the detachment

point, 10%, is reached.