RBS 2007 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

139

RBS Group • Annual Report and Accounts 2007

Financial statements

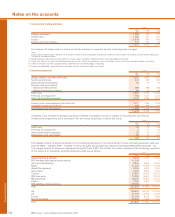

Accounting developments

International Financial Reporting Standards

The International Financial Reporting Interpretations Committee

(‘IFRIC’) issued interpretation IFRIC 11 ‘Group and Treasury

Share Transactions’ in November 2006. Entities which buy their

own shares, or whose shareholders buy shares in the reporting

entity, in order to provide incentives to employees must

account for those incentives on an equity-settled basis.

This principle applies also to the accounting by subsidiaries.

The interpretation is effective for annual accounting periods

beginning on or after 1 March 2007 and is not expected to

have a material effect on the Group or company.

The IFRIC issued interpretation IFRIC 12 ‘Service Concession

Arrangements’ in November 2006. Entities providing

infrastructure and services to governments under concession

arrangements must account for each component of the

arrangement separately. Infrastructure provided under these

arrangements may be recognised as either a financial asset or

an intangible asset. The interpretation is effective for

accounting periods beginning on or after 1 January 2008 and

is not expected to have a material effect on the Group or company.

The IASB issued IFRS 8 ‘Operating Segments’ in November

2006. This will replace IAS 14 ‘Segment Reporting’ for

accounting periods beginning on or after 1 January 2009. IFRS

8 requires entities to report segment information as reported to

management and reconcile it to the financial statements and is

not expected to have a material effect on the Group or company.

The IASB issued a revised IAS 23 ‘Borrowing Costs’ in March

2007. Entities are required to capitalise borrowing costs

attributable to the development or construction of intangible

assets or property plant or equipment. The standard is

effective for accounting periods beginning on or after 1

January 2009 and is not expected to have a material effect on the

Group or company.

The IFRIC issued interpretation IFRIC 13 ‘Customer Loyalty

Programmes’ in June 2007. Entities that provide customers

with benefits ancillary to a sale of goods or services should

apportion the sales proceeds to those benefits on the basis of

relative fair values. The interpretation is effective for accounting

periods beginning on or after 1 July 2008 and is not expected

to have a material effect on the Group or company.

The IFRIC issued interpretation IFRIC 14 ‘IAS 19 – The Limit on

a Defined Benefit Asset, Minimum Funding Requirements and

their Interaction’ in July 2007. The net pension asset that may

be recognised by a sponsoring entity is limited to the amount

to which it has an unconditional right of refund or can be

recovered through the settlement of plan liabilities. Entities

legally bound to minimum funding requirements are required to

take account of those obligations when recognising the net

asset or liability for an employee benefit scheme. The

interpretation is effective for accounting periods beginning on

or after 1 January 2008 and is not expected to have a material

effect on the Group or company.

The IASB issued a revised IAS 1 ‘Presentation of Financial

Statements’ in September 2007 effective for accounting

periods beginning on or after 1 January 2009. The amendments

to the presentation requirements for financial statements are

not expected to have a material effect on the Group or company.

The IASB published a revised IFRS 3 ‘Business Combinations’

and related revisions to IAS 27 ‘Consolidated and Separate

Financial Statements’ following the completion in January 2008

of its project on the acquisition and disposal of subsidiaries.

The standards improve convergence with US GAAP and

provide new guidance on accounting for changes in interests

in subsidiaries. The cost of an acquisition will comprise only

consideration paid to vendors for equity; other costs will be

expensed immediately. Groups will only account for goodwill on

acquisition of a subsidiary; subsequent changes in interest will

be recognised in equity and only on a loss of control will there

be a profit or loss on disposal to be recognised in income.

The changes are effective for accounting periods beginning on

or after 1 July 2009 but both standards may be adopted

together for accounting periods beginning on or after 1 July

2007. These changes will affect the Group's accounting for

future acquisitions and disposals

of subsidiaries.

The IASB published revisions to IAS 32 ‘Financial Instruments:

Presentation’ and consequential revisions to other standards in

February 2008 to improve the accounting for and disclosure of

puttable financial instruments. The revisions are effective for

accounting periods beginning on or after 1 January 2009 but

together they may be adopted earlier. They are not expected

to have a material affect on the Group or the company.