RBS 2007 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

RBS Group • Annual Report and Accounts 2007 193

Financial statements

Non-trading

The principal market risks arising from the Group’s non-trading

activities are interest rate risk, currency risk and equity risk.

Treasury activity and mismatches between the repricing of

assets and liabilities in its retail and commercial banking

operations account for most of the non-trading interest rate

risk. Non-trading currency risk derives from the Group’s

investments in overseas subsidiaries, associates and branches.

The Group’s strategic investment in Bank of China, venture capital

portfolio and investments held by its general insurance business

are the principal sources of non-trading equity price risk.

The Group’s portfolios of non-trading financial instruments

mainly comprise loans (including finance leases), debt

securities, equity shares, deposits, certificates of deposit and

other debt securities issued, loan capital and derivatives. To

reflect their distinct nature, the Group’s long-term assurance

assets and liabilities attributable to policyholders have been

excluded from these market risk disclosures.

Interest rate risk

Non-trading interest rate risk arises from the Group’s treasury

activities and retail and commercial banking businesses.

Treasury

The Group’s treasury activities include its money market

business and the management of internal funds flow within the

Group’s businesses. Money market portfolios include cash

instruments (principally debt securities, loans and deposits)

and related hedging derivatives. VaR for the Group’s treasury

portfolios, which relates mainly to interest rate risk including

credit spreads, was £5.5 million at 31 December 2007 (2006 –

£1.5 million). During the year the maximum VaR was £6.4

million (2006 – £4.4 million), the minimum £1.3 million (2006 –

£0.6 million) and the average £3.7 million (2006 – £2.4 million).

Retail and commercial banking

Non-trading interest rate risk is calculated in each business on

the basis of establishing the repricing behaviour of each asset,

liability and off-balance sheet product. For many products, the

actual interest rate repricing characteristics differ from the

contractual repricing. In most cases, the repricing maturity is

determined by the market interest rate that most closely fits the

historical behaviour of the product interest rate. For non-

interest bearing current accounts, the repricing maturity is

determined by the stability of the portfolio. The repricing

maturities used are approved by Group Treasury and divisional

asset and liability committees at least annually. Key

conventions are reviewed annually by GALCO.

A static maturity gap report is produced as at the month-end

for each division, in each functional currency based on the

behaviouralised repricing for each product. It is Group policy

to include in the gap report, non-financial assets and liabilities,

mainly property, plant and equipment and the Group’s capital

and reserves, spread over medium and longer term maturities.

This report also includes hedge transactions, principally

derivatives.

Any residual non-trading interest rate exposures are controlled

by limiting repricing mismatches in the individual business

balance sheets. Potential exposures to interest rate movements

in the medium to long term are measured and controlled using

a version of the same VaR methodology that is used for the

Group’s trading portfolios but without discount factors. Net

accrual income exposures are measured and controlled in

terms of sensitivity over time to movements in interest rates.

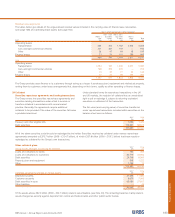

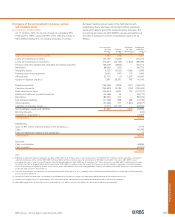

The VaR for the Group’s trading portfolios segregated by type of market risk exposure, including idiosyncratic risk, is presented in the

table below.

2007 2006

Average Period end Maximum Minimum Average Period end Maximum Minimum

Trading £m £m £m £m £m £m £m £m

Interest rate 12.5 15.0 21.8 7.6 8.7 10.2 15.0 5.7

Credit spread 18.8 41.9 45.2 12.6 13.2 14.1 15.7 10.4

Currency 2.6 3.0 6.9 1.1 2.2 2.5 3.5 1.0

Equity 5.4 14.0 22.0 1.4 1.1 1.6 4.4 0.5

Commodity 0.2 0.5 1.6 — 0.2 — 1.1 —

Diversification (28.7) (12.8)

Total trading VaR 21.6 45.7 50.1 13.2 14.2 15.6 18.9 10.4

Trading

The primary focus of the Group’s trading activities is client

facilitation – providing products to the Group’s client base at

competitive prices. The Group also undertakes: market making

– quoting firm bid (buy) and offer (sell) prices with the intention

of profiting from the spread between the quotes; arbitrage –

entering into offsetting positions in different but closely related

markets in order to profit from market imperfections; and

proprietary activity – taking positions in financial instruments as

principal in order to take advantage of anticipated market

conditions. The principal risk factors are interest rates, credit

spreads, equity prices and foreign exchange. Financial

instruments held in the Group’s trading portfolios include, but

are not limited to, debt securities, loans, deposits, equity

shares, securities sale and repurchase agreements and

derivative financial instruments (futures, forwards, swaps and

options). For a discussion of the Group’s accounting policies

for derivative financial instruments, see Accounting policies on

page 130.