RBS 2007 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

RBS Group • Annual Report and Accounts 2007

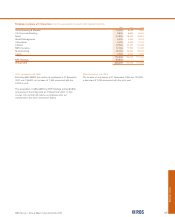

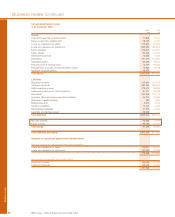

72

Business review continued

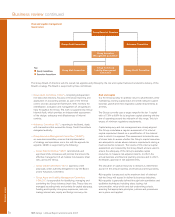

Business review

Credit risk

Credit risk is managed to achieve sustainable and superior

risk-reward performance whilst maintaining exposures within

acceptable risk appetite parameters. This is achieved through

the combination of governance, policies, systems and

controls, underpinned by sound commercial judgement as

described below.

•Policies and risk appetite: policies provide clarity around the

required Group framework for the assessment, approval,

monitoring and management of credit risk where risk

appetite sets the tolerance of loss. Limits are used to

manage concentration risk by single name, sector and

country.

•Decision makers: credit authority is granted to independent

persons or committees with the appropriate experience,

seniority and commercial judgement. Credit authority is not

extended to relationship managers. Specialist internal credit

risk departments independently oversee the credit process

and make credit decisions or recommendations to the

appropriate credit committee.

•Models: credit models are used to measure and assess risk

decisions and to aid on-going monitoring. Measures, such

as Probability of Default, Exposure at Default, Loss Given

Default (see below) and Expected Loss are calculated using

duly authorised models. All credit models are subject to

independent review prior to implementation and existing

models are reviewed on at least an annual basis.

•Mitigation techniques to reduce the potential for loss: credit

risk may be mitigated by the taking of financial or physical

security, the assignment of receivables or the use of credit

derivatives, guarantees, risk participations, credit insurance,

set off or netting.

•Risk systems and data quality: systems are well organised to

produce timely, accurate and complete inputs for risk

reporting and to administer key credit processes.

•Analysis and reporting: portfolio analysis and reporting are

used to ensure the identification of emerging concentration

risks and adverse movements in credit risk quality.

•Stress testing: stress testing forms an integral part of

portfolio analysis, providing a measure of potential

vulnerability to exceptional but plausible economic and

geopolitical events which assists management in the

identification of risk not otherwise apparent in more benign

circumstances. Stress testing informs risk appetite decisions.

•Portfolio management: active management of portfolio

concentrations as measured by risk reporting and stress

testing, where credit risk may be mitigated through

promoting asset sales, buying credit protection or curtailing

risk appetite for new transactions.

•Credit stewardship: customer transaction monitoring and

management is a continuous process, ensuring performance

is satisfactory and that documentation, security and

valuations are complete and up to date.

•Problem debt identification: policies and systems encourage

the early identification of problems and the employment of

specialised staff focused on collections and problem debt

management.

•Provisioning: independent assessment using best practice

models for collective and latent loss. Professional evaluation

is applied to individual cases, to ensure that such losses are

comprehensively identified and adequately provided for.

•Recovery: maximising the return to the Group through the

recovery process.

Basel II

RBS has received agreement (called ‘a waiver’) from the UK

Financial Services Authority to adopt the Advanced Internal

Ratings Based (AIRB) approach for calculating capital

requirements for the majority of the business with effect from

1 January 2008. The Group, therefore, will be one of a small

number of banks whose risk systems and approaches have

achieved the advanced standard for credit, the most

sophisticated available under the new Basel II framework.

The AIRB approach to Basel II is based on the

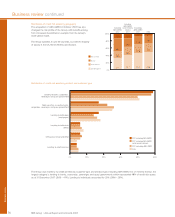

following metrics.

•Probability of default (“PD”): the likelihood that a customer

will fail to make full and timely repayment of credit

obligations over a one year time horizon. Customers are

assigned an internal credit grade which corresponds to

probability of default. Every customer credit grade across all

grading scales in the Group can be mapped to a Group

level credit grade (see page 74).

•Exposure at default (“EAD”): such models estimate the

expected level of utilisation of a credit facility at the time of

a borrower’s default. The EAD is typically higher than the

current utilisation (e.g. in the case where further drawings

are made on a revolving credit facility prior to default) but

will not typically exceed the total facility limit.

•Loss given default (“LGD”): models estimate the economic

loss that may occur in the event of default, being the debt

that cannot be recovered. The Group’s LGD models take into

account the type of borrower, facility and any risk mitigation

such as security or collateral held.