RBS 2007 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

59

RBS Group • Annual Report and Accounts 2007

Business review

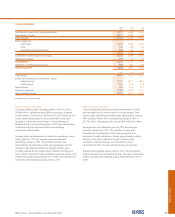

Citizens

2007 2006 2005

£m £m £m

Net interest income 1,975 2,085 2,122

Non-interest income 1,147 1,232 1,142

Total income 3,122 3,317 3,264

Direct expenses

– staff costs 741 803 819

– other 717 751 739

1,458 1,554 1,558

Contribution before impairment losses 1,664 1,763 1,706

Impairment losses 341 181 131

Operating profit 1,323 1,582 1,575

US$bn US$bn US$bn

Total assets 161.1 162.2 158.8

Loans and advances to customers – gross

– mortgages 19.1 18.6 18.8

– home equity 35.9 34.5 31.8

– other consumer 21.7 23.2 24.8

– corporate and commercial 37.6 32.7 29.2

Customer deposits 115.0 106.8 106.3

Customer deposits (excluding wholesale funding) 105.0 101.8 105.2

Risk-weighted assets 114.4 113.1 106.4

Average exchange rate – US$/£ 2.001 1.844 1.820

Spot exchange rate – US$/£ 2.004 1.965 1.721

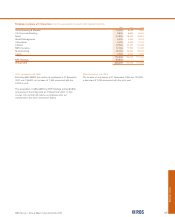

2007 compared with 2006

Against the background of weaker housing and credit market

conditions, Citizens’ franchise demonstrated resilience in 2007,

with a particularly good performance in corporate and

commercial banking. Modest growth in net interest margins

and strong fee growth in several products lifted income by 2%

to $6,249 million which, coupled with tight cost control,

resulted in contribution before impairment losses growing by

2% to $3,329 million. However, impairment losses increased

from 0.31% of loans and advances to 0.60%, resulting in a

decrease in operating profit of 9% to $2,647 million. In sterling

terms, total income decreased by 6% to £3,122 million and

operating profit fell by 16% to £1,323 million.

Net interest income rose by 3% to $3,954 million. Average

loans and advances to customers increased by 4%, with

strong growth in corporate and commercial lending, up 13%,

with close attention being paid to our risk appetite in light of

prevailing market conditions. Average customer deposits

increased by 1% but deposit margins narrowed as a result of

deposit pricing competition and continued migration from low-

cost checking accounts and liquid savings to higher-cost

products. Notwithstanding this migration, Citizens’ net interest

margin increased slightly to 2.80% in 2007, compared with

2.72% in 2006, thanks in part to improved lending spreads in

the latter part of the year.

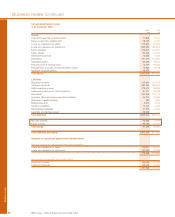

Non-interest income rose by 1% to $2,295 million. Business

and corporate fees rose strongly, with good results especially

in foreign exchange, interest rate derivatives and cash

management, driven by increasing cooperation with RBS

Corporate Markets. Good progress was also made in credit

card issuing, where we increased our customer base by 20%,

and in merchant acquiring, where RBS Lynk achieved

significant growth, processing 30% more transactions than in

2006 and expanding its merchant base by 5%.

In response to more difficult market conditions Citizens

intensified cost discipline, with a reduction in headcount

helping to limit total expense growth to 2%, despite

enhancements to infrastructure and processes as well as

continued investment in growth opportunities including mid-

corporate banking, contactless debit cards and merchant

acquiring.

Rising losses and increased provisions lifted impairment costs

from $333 million in 2006 to $682 million in 2007. Against a

background of weaker economic activity the Citizens portfolio

is performing well, although we have experienced a reversion

from the very low levels of impairment seen in recent years,

reflecting both the planned expansion of our commercial loan

book and the impact of a softer housing market. There has

also been an increase in reserving. The average FICO scores

on our consumer portfolios, including home equity lines of

credit, remain in excess of 700, with 97% of lending secured.

Average loan-to-value ratios at the end of 2007 were 58% on

our residential mortgage book and 74% on our home equity

book.