RBS 2007 Annual Report Download - page 187

Download and view the complete annual report

Please find page 187 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

RBS Group • Annual Report and Accounts 2007 185

Financial statements

Continuing involvement

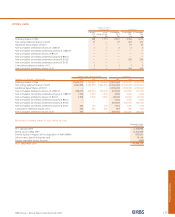

In certain securitisations of US residential mortgages,

substantially all the risks and rewards have been neither

transferred nor retained, but the Group has retained control, as

defined by IFRS, of the assets and continues to recognise the

assets to the extent of its continuing involvement which takes

the form of retaining certain subordinated bonds issued by the

securitisation SPEs. These bonds have differing rights and,

depending on their terms, they may expose the Group to

interest rate risk where they carry a fixed coupon or to credit

risk depending on the extent of their subordination. Certain

bonds entitle the Group to additional interest if the portfolio

performs better than expected and others give the Group the

right to prepayment penalties received on the securitised

mortgages. At 31 December 2007, securitised assets were

£18.1 billion (2006 – £37.3 billion); retained interests £1,037

million (2006 – £930 million); subordinated assets £314 million

(2006 – £694 million) and related liabilities £314 million (2006 –

£694 million).

Derecognition

Other securitisations of the Group’s financial assets in the US

qualify for derecognition as substantially all the risks and rewards

of the assets have been transferred. The Group continues to

recognise any retained interests in the securitisation vehicles.

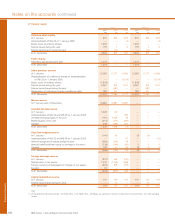

Financial risk management policies and objectives

The Group Board of directors sets the overall risk appetite and

philosophy; the risk and capital framework underpins delivery

of the Board’s strategy.

Risk and capital

It is the Group’s policy to optimise return to shareholders while

maintaining a strong capital base and credit rating to support

business growth and meet regulatory capital requirements at

all times.

Risk appetite is measured as the maximum level of retained

risk the Group will accept to deliver its business objectives.

Risk appetite is generally defined through both quantitative and

qualitative techniques including stress testing, risk

concentration, value-at-risk and risk underwriting criteria,

ensuring that appropriate principles, policies and procedures

are in place and applied.

The main financial risks facing the Group are as follows:

•Credit risk: is the risk arising from the possibility that the

Group will incur losses from the failure of customers to meet

their obligations.

•Funding and liquidity risk: is the risk that the Group is unable

to meet its obligations as they fall due.

•Market risk: the Group is exposed to market risk because of

positions held in its trading portfolios and its non-trading

businesses.

•Equity risk: gains or losses on equity investments.

•Insurance risk: the Group is exposed to insurance risk, either

directly through its businesses or through using insurance as

a tool to mitigate other risk exposures.

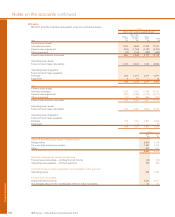

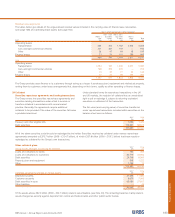

Credit risk

Credit risk is managed to achieve sustainable and superior

risk-reward performance while maintaining exposures within

acceptable risk appetite parameters. This is achieved through

the combination of governance, policies, systems and controls,

underpinned by sound commercial judgement as described

below.

•Policies and risk appetite: policies provide a clear framework

for the assessment, approval, monitoring and management

of credit risk where risk appetite sets the tolerance of loss.

Limits are used to manage concentration risk by single

name, sector and country.

•Decision makers: credit authority is granted to independent

persons or committees with the appropriate experience,

seniority and commercial judgement. Credit authority is not

extended to relationship managers. Specialist internal credit

risk departments independently oversee the credit process

and make credit decisions or recommendations to the

appropriate credit committee.

•Models: credit models are used to measure and assess risk

decisions and to aid on-going monitoring. Measures, such

as Probability of Default, Exposure at Default, Loss Given

Default (see page 186) and Expected Loss are calculated

using duly authorised models. All credit models are subject

to independent review prior to implementation and existing

models are reviewed on at least an annual basis.

31 Risk management