RBS 2007 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

55

RBS Group • Annual Report and Accounts 2007

Business review

2006 compared with 2005

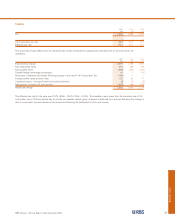

Retail has delivered a good performance in 2006, achieving

4% growth in total income to £7,566 million. Contribution before

impairment losses was up by 6% to £5,140 million, contribution

by 3% to £3,830 million, and operating profit by 2% to £2,250

million.

We have advanced in personal banking, with good growth in

savings and investment products combined with effective cost

control and improvements in the quality of our lending book.

Credit card recruitment and unsecured personal lending

continues to be focused on lower risk segments, with reduced

emphasis on acquisition through direct marketing.

We have continued to expand our customer franchise, growing

our personal current account base by 232,000 in 2006 as a

result of our sustained focus on quality and customer service.

We continue to have the highest share of customers switching

current accounts from other banks, and are now joint leader in

the personal current account market. RBS is first and NatWest

is joint second among major high street banks in Great Britain

for the percentage of main current account customers that are

“extremely satisfied” overall.

Net interest income increased by 4% to £4,108 million, with

faster growth in deposits helping to mitigate lower unsecured

lending volumes. Net interest margin improved slightly in the

second half.

Average customer deposit balances were 9% higher, driven by

personal savings balances up 12% and accelerating growth in

business deposits, up 7%. Average mortgage lending was up

8%, with stronger volumes in the second half leading to a 7%

market share of net lending in that period. Our offset mortgage

product continues to perform well. For the year as a whole,

average personal unsecured lending and credit card lending

was flat, reflecting the slower UK consumer demand and our

concentration on quality business with existing customers. In

the second half we further reduced our activity in the direct

loans market, but unsecured balances from our RBS and NatWest

customers are broadly in line with the first half. Average business

lending rose 5%, reflecting our cautious credit stance.

Non-interest income rose by 4% to £3,458 million. There was

strong growth in our investments and private banking businesses

as well as business banking fees, mitigating the slowdown in

personal loan related insurance income.

Despite investments for future growth, total expenses rose

by just 1%, to £3,518 million, whilst direct expenses were held

flat at £1,938 million. Staff costs increased by 3% to £1,317

million, reflecting sustained investment in customer service and

the expansion of our bancassurance and investment

businesses. We continue to make efficiency gains as a result of

the consolidation of our retail businesses. Other costs, such as

marketing expenses, fell by 6% to £621 million, also benefiting

from consolidation.

Impairment losses increased by 15% to £1,310 million, but

were lower in the second half of the year than in the first. The

year-on-year change in impairment losses slowed from 19% in

the first half to 12% in the second half. Credit card arrears

have stabilised, while the rate of increase in arrears on

unsecured personal loans continued to slow. Mortgage arrears

remain very low – the average loan-to-value ratio of Retail’s

mortgages was 46% overall and 64% on new mortgages

written in 2006. Small business credit quality remains steady.

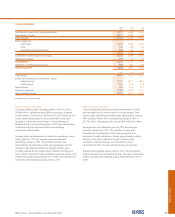

Bancassurance

Bancassurance has had an excellent year with sales

increasing by 56% to £267 million annual premium equivalent.

The growth reflects the continued increase in focus on the

recruitment of Financial Planning Managers, up 25% and

productivity levels, up 43%. Increased sales of collective

investments on the back of a successful ISA season and

strong individual pensions growth, boosted by A-Day, helped

underpin the outturn. Sales of guaranteed bonds were also

particularly strong, and helped support a new business margin

which improved significantly over the period. The product

proposition was strengthened across all lines. Latest market

share data shows an increase from 6.6% to 9.0%. On a UK

GAAP embedded value basis for life assurance, investment

contracts and open ended investment companies, adjusted for

investment market volatility, pre tax profit was £78 million

compared with £42 million in 2005.

Net claims, which include maturities, surrenders and liabilities

to policyholders, were stable at £488 million compared with

£486 million in 2005.

balances. Net interest margin declined modestly, in line with

previous guidance, with savings margins consistent with 2006,

despite increased competition for deposits.

Non-interest income was £3,571 million, 3% ahead of 2006,

with strong growth in investment income offset by lower levels

of direct lending and reduced instances of current account

fees.

Total expenses rose by 2% to £3,578 million, driven by

increased investment in customer-facing staff in branches and

in our bancassurance and investment businesses. Other costs

reduced by 1% to £614 million.

Impairment losses decreased by 9% to £1,196 million,

reflecting the improvement in arrears trends on both credit

cards and unsecured personal loans. Mortgage arrears

remained very low, and we have maintained conservative

lending criteria – the average loan-to-value ratio of Retail’s

mortgages was 46% overall and 63% on new mortgages

written in 2007, and this improved as the year progressed.

Small business credit quality remained good.