RBS 2007 Annual Report Download - page 188

Download and view the complete annual report

Please find page 188 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Financial statements

RBS Group • Annual Report and Accounts 2007

186

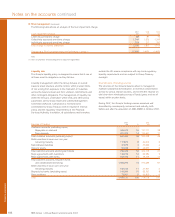

Notes on the accounts continued

•Mitigation techniques to reduce the potential for loss: credit

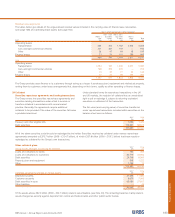

risk may be mitigated by the taking of financial or physical

security, the assignment of receivables or the use of credit

derivatives, guarantees, risk participations, credit insurance,

set off or netting.

•Risk systems and data quality: systems are well organised to

produce timely, accurate and complete inputs for risk

reporting and to administer key credit processes.

•Analysis and reporting: portfolio analysis and reporting are

used to ensure the identification of emerging concentration

risks and adverse movements in credit risk quality.

•Stress testing: stress testing forms an integral part of

portfolio analysis, providing a measure of potential

vulnerability to exceptional but plausible economic and

geopolitical events which assists management in the

identification of risk not otherwise apparent in more benign

circumstances. Stress testing informs risk appetite decisions.

•Portfolio management: active management of portfolio

concentrations as measured by risk reporting and stress

testing, where credit risk may be mitigated through

promoting asset sales, buying credit protection or curtailing

risk appetite for new transactions.

•Credit stewardship: customer transaction monitoring and

management is a continuous process, ensuring performance

is satisfactory and that documentation, security and

valuations are complete and up to date.

•Problem debt identification: policies and systems encourage

the early identification of problems and the employment of

specialised staff focused on collections and problem debt

management.

•Provisioning: independent assessment using best practice

models for collective and latent loss. Professional evaluation

is applied to individual cases, to ensure that such losses are

comprehensively identified and adequately provided for.

•Recovery: maximising the return to the Group through the

recovery process.

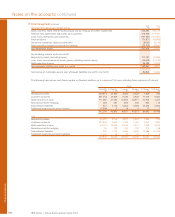

Credit risk models

Credit risk models are used throughout the Group to support

the analytical elements of the credit risk management

framework, in particular the risk assessment part of the credit

approval process, ongoing monitoring as well as portfolio

analysis and reporting. Credit risk models used by the Group

can be broadly grouped into three categories.

•Probability of default (“PD”): the likelihood that a customer

will fail to make full and timely repayment of credit

obligations over a one year time horizon. Customers are

assigned an internal credit grade which corresponds to

probability of default. Every customer credit grade across all

grading scales in the Group can be mapped to a Group

level credit grade (see page 74).

•Exposure at default (“EAD”): such models estimate the

expected level of utilisation of a credit facility at the time of

a borrower’s default. The EAD is typically higher than the

current utilisation (e.g. in the case where further drawings

are made on a revolving credit facility prior to default) but

will not typically exceed the total facility limit.

•Loss given default (“LGD”): models estimate the economic

loss that may occur in the event of default, being the debt

that cannot be recovered. The Group’s LGD models take into

account the type of borrower, facility and any risk mitigation

such as security or collateral held.

Loan impairment

The Group classifies impaired assets as either Risk Elements

in Lending (REIL) or Potential Problem Loans (PPL). REIL

represents non-accrual loans, loans that are accruing but

are past due 90 days and restructured loans. PPL represents

impaired assets which are not included in REIL but where

information about possible credit problems cause management

to have serious doubts about the future ability of the borrower

to comply with loan repayment terms.

Both REIL and PPL are reported gross of the value of any

security held, which could reduce the eventual loss should it

occur, and gross of any provision marked. Therefore impaired

assets which are highly collateralised, such as mortgages, will

have a low coverage ratio of provisions held against reported

impaired balance.

31 Risk management (continued)