RBS 2007 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

137

RBS Group • Annual Report and Accounts 2007

Financial statements

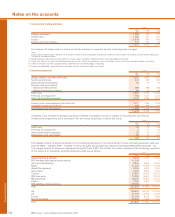

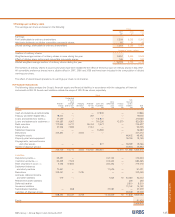

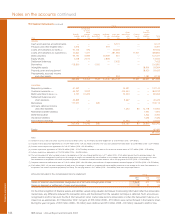

The Group’s valuation of the super senior asset-backed CDO

exposures takes into consideration outputs from a proprietary

model, market data and appropriate valuation adjustments.

There is significant subjectivity in the valuation with very little

market activity to provide support for fair value levels at which

willing buyers and sellers would transact.

The Group’s proprietary model predicts the expected cash

flows of the underlying mortgages using assumptions about

future macroeconomic conditions (including house price

appreciation and depreciation) and defaults/delinquencies on

these underlying mortgages derived from publicly available

data. The resulting cash flows are discounted using a risk

adjusted rate.

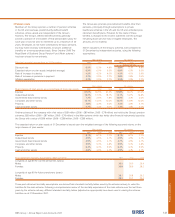

Alternative valuations have been produced using reasonably

possible alternative assumptions about macroeconomic

conditions including house price appreciation and depreciation,

and the effect of regional variations. In addition, the discount

rate applied to the model output has been stressed. The output

from using these alternative assumptions has been compared

with inferred pricing from other published data.

The Group believes that reasonably possible alternative

assumptions could reduce or increase predicted cumulative

losses from the model by up to 20%. Using these alternative

assumptions would reduce the fair value by up to £385 million

or increase the fair value by up to £235 million.

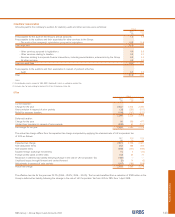

Other debt securities – where observable market prices for a

particular debt security are not available, the fair value will

typically be determined with reference to observable market

transactions in other credit related products including debt

securities and credit derivatives. Assumptions are made about

the relationship between the individual debt security and the

available benchmark data. Using differing assumptions about

this relationship would result in different fair values for these

assets. Using reasonably possible alternative assumptions for

credit spread (taking into account the underlying currency,

tenor and rating) would reduce the fair value by up to £88

million or increase the fair value by up to £109 million.

Derivatives – derivatives are priced using quoted prices for the

same or similar instruments where these are available.

However, the majority of derivatives are valued using pricing

models. Inputs for these models are usually observed directly

in the market, or derived from observed prices. However, it is

not always possible to observe or corroborate all model inputs.

Unobservable inputs used are based on estimates taking into

account a range of available information including historic

analysis, historic traded levels, market practice, comparison to

other relevant benchmark observable data and consensus

pricing data. Using reasonably possible alternative

assumptions, principally correlations, including the relative

impact of unobservable inputs as compared to those which

may be observed, would reduce the fair value by up to £80

million or increase the fair value by up to £80 million.

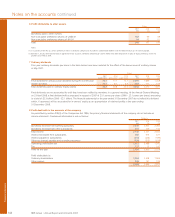

Other portfolios – other than the portfolios discussed above,

there are other financial instruments which are held at fair

value determined from data which are not market observable,

or incorporating material adjustments to market observed data.

Using reasonably possible alternative assumptions appropriate

to the financial asset or liability in question, such as credit

spreads, derivative inputs and equity correlations, would

reduce the fair value by up to £119 million or increase the fair

value by up to £117 million.