RBS 2007 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Business review

81

RBS Group • Annual Report and Accounts 2007

Short positions in various securities are held primarily by RBS

Greenwich Capital in the US, RBS Global Banking & Markets

and by ABN AMRO Global Markets. Excluding ABN AMRO,

the level of funding from short term unsecured debt issuance,

bank deposits (excluding repos) and short positions has

increased by £62.0 billion (44%) to represent 23% of total

funding at 31 December 2007. Including ABN AMRO, such

short-term wholesale borrowing has added £175.3 billion to

that figure, to represent 26% of total funding in the enlarged

balance sheet.

Net customer activity

Excluding ABN AMRO, net customer lending, excluding repos,

rose by £14.7 billion (17%) over the course of 2007 as the

growth in loans and advances to customers continued to

exceed growth in customer accounts, thus increasing

commensurately the reliance on wholesale market funding to

support loan growth.

Including ABN AMRO, net customer lending, excluding repos,

has added £43.5 billion, reducing the ratio of loans and

advances to customer accounts to 126.6%.

Including Excluding

ABN AMRO ABN AMRO

2007 2007 2006 2005

Net customer activity £m £m £m £m

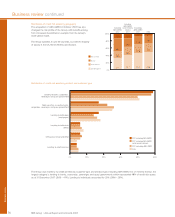

Loans and advances to customers (gross, excluding reverse repos) 693,331 468,942 407,918 372,223

Customer accounts (excluding repos) 547,449 366,538 320,238 294,113

Customer lending less customer accounts 145,882 102,404 87,680 78,110

Loans and advances to customers as a % of customer accounts (excluding repos) 126.6% 127.9% 127.4% 126.6%

Management of term structure

The Group evaluates on a regular basis its structural liquidity

risk and applies a variety of balance sheet management and

term funding strategies to maintain this risk within its normal

policy parameters.

The degree of maturity mismatch within the overall long-term

structure of the Group’s assets and liabilities is managed

within internal policy guidelines, to ensure that term asset

commitments may be funded on an economic basis over their

life. In managing its overall term structure, the Group analyses

and takes into account the effect of retail and corporate

customer behaviour on actual asset and liability maturities

where they differ materially from the underlying contractual

maturities.

Stress testing

In August 2007, a systemic liquidity stress event was triggered

by difficulties in the US sub-prime mortgage market which then

spread more widely to the global asset-backed market and

impacted adversely the overall supply and cost of funding and

liquidity for other than very short-term maturities. RBS has

managed its liquidity position through those market conditions,

increased its liquidity cushion and remains able fully to meet its

funding needs.

The Group performs stress tests to simulate how events may

impact its funding and liquidity capabilities. Such tests inform

the overall balance sheet structure and help define prudent

limits for control of the risk arising from the mismatch of

maturities across the balance sheet and from undrawn

commitments and other contingent obligations. The nature of

stress tests is kept under review in line with evolving market

conditions.

Contingency funding plans are maintained to anticipate and

respond to any approaching or actual material deterioration in

market conditions. The Group remains confident that it can

manage its liquidity requirements effectively under such

circumstances.

Daily management

The primary focus of the daily management activity is to

ensure access to sufficient liquidity to meet cash flow

obligations within key time horizons, in particular out to one

month ahead.

The short-term maturity structure of the Group’s liabilities and

assets is managed daily to ensure that all material or potential

cash flow obligations, arising from undrawn commitments and

other contingent obligations can be met. Potential sources

include cash inflows from maturing assets, new borrowing or

the sale of various debt securities held (after allowing for

appropriate haircuts).

Short-term liquidity risk is generally managed on a

consolidated basis with internal liquidity mismatch limits set for

all subsidiaries and non-UK branches which have material

local treasury activities, thereby assuring that the daily

maintenance of the Group’s overall liquidity risk position is not

compromised. ABN AMRO, Citizens Financial Group and RBS

Insurance manage liquidity locally, given different regulatory

regimes, subject to review by Group Treasury. As integration of

ABN AMRO’s businesses within the Group proceeds, the

liquidity risk policies, parameters and metrics used will be

progressively aligned within a single framework.