RBS 2007 Annual Report Download - page 233

Download and view the complete annual report

Please find page 233 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

231

RBS Group • Annual Report and Accounts 2007

Additional information

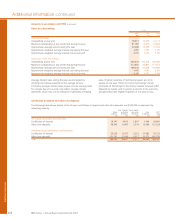

Economic and monetary environment

The Group’s earnings are affected by the economic and

monetary environment in its key markets (UK, US, Eurozone

and Asia Pacific).

Global financial markets entered a period of unprecedented

strain in the second half of 2007, with reference interbank

lending rates spiking sharply and parts of the short-term

money market seizing up. This temporarily tightened monetary

conditions, affecting credit supply and denting investor risk

appetite, at a time when a slowdown in global economic

activity had started. After a series of individual efforts, central

banks in Canada, the Eurozone, Switzerland, the UK and the

US intervened in concert to improve liquidity conditions in

money markets in December. This measure was successful in

bringing interest rate spreads in interbank markets back

towards historic averages, but uncertainties about the full

impact on the real economy and the future evolution of debt

markets remain.

The UK interest rate cycle peaked in 2007, with the Monetary

Policy Committee (MPC) first hiking the Bank Rate from 5% to

5.75% in three successive 25bps moves in January, May and

July, before cutting it back to 5.50% in December and most

recently to 5.25% in February. The rate increases were due to a

combination of above-trend growth at 3.1% and CPI-inflation

exceeding the official target of 2% for most of the year on the

back of high commodity prices. Upside risks to inflation over

the medium-term prevailed, preventing the MPC from cutting

more aggressively in response to the liquidity squeeze in

financial markets in December. On balance, monetary

conditions were probably in restrictive territory in 2007, which

is expected to lead to slower growth in 2008. Sterling’s 6%

depreciation on a trade-weighted basis only partly offset the

dampening impact from strains in money markets and high

inflation-adjusted interest rates, which only started to fall

towards the end of the year.

US monetary conditions were close to neutral at the start of

2007, with policy rates on hold at 5.25% until the onset of the

liquidity crisis in August. A marked slowdown in the US

housing market, deterioration in consumer and business

confidence and the liquidity squeeze in financial markets

prompted the Federal Open Market Committee (FOMC) to

bring the federal funds rate down to 4.25% by the end of the

year. Despite a 10% decline in the value of the dollar on a

trade-weighted basis and the resulting stimulus for US exports,

the overall outlook for the US economy darkened materially in

the first two months of 2008. The FOMC continued to react

aggressively in the face of more evidence of downside risks to

economic growth, and further reduced the policy rate by

125bps at two meetings in January, bringing it to 3.00% at the

end of February 2008. Even though CPI-inflation ran above 4%

by the end of 2007, US bond markets did not seem overly

concerned about rising inflationary pressure in the longer term,

as the long-end of the yield curve shifted downwards too.

Against the backdrop of robust demand, and an upward trend

in CPI-inflation, the European Central Bank raised the official

refinancing rate twice in the first half of 2007, from 3.5% to

4%, and staying on hold for the rest of the year. Rapid

economic growth in emerging market economies resulted in

strong demand for Eurozone export goods, despite a 5%

trade-weighted appreciation of the euro. Overall, the Eurozone

appeared to be less affected by the liquidity squeeze than the

UK or the US, partly because domestic demand had been less

reliant on credit.

Asia Pacific was the most dynamic region in 2007, with

economic growth outpacing the rate of expansion recorded in

other regions. Exports remained the main driver of economic

growth, resulting in a large current account surplus, and

corresponding inflows of foreign exchange into the region.

Some countries in the region continued to manage their

currencies, to prevent appreciation. This loosening of monetary

conditions boosted domestic investment. Inflationary pressures

started to emerge, possibly requiring a tighter stance of

monetary policy further out.

In addition to influencing the level of effective demand

countries face, exchange rates affect earnings reported by the

Group’s non-UK subsidiaries, and the value of non-sterling

denominated assets and liabilities. Sterling remained strong

against the dollar in 2007, gaining another 1%, but slipped by

8% against the euro. These movements have mixed effects on

the Group’s reported earnings, assets and liabilities, boosting

their sterling-value when denominated in euro but depressing

their sterling-value when denominated in dollars.

Supervision and regulation

1. United Kingdom

1.1 Authorised firms in the Group

The UK Financial Services Authority (FSA) is the

consolidated supervisor of the Group and the Royal Bank.

As at 31 December 2007, 31 companies in the Group

(excluding subsidiaries of the ABN AMRO Group),

spanning a range of financial services sectors (banking,

insurance and investment business), were authorised to

conduct financial activities regulated by the FSA.

The UK authorised banks in the Group include the Royal

Bank, NatWest, Coutts & Co and Ulster Bank Ltd.

Wholesale activities, other than Group Treasury activities,

are concentrated in the Group’s Corporate Markets division

and are undertaken under the names of the Royal Bank

and NatWest. UK retail banking activities are managed by

the Retail Markets division. The exception is Ulster Bank

Ltd, which is run as a separate division within the Group.

Ulster Bank Ltd provides banking services in Northern

Ireland while the banking service to the Republic of Ireland

is provided by Ulster Bank Ireland Ltd which is primarily

supervised by the Irish Financial Services Regulatory

Authority.