RBS 2007 Annual Report Download - page 194

Download and view the complete annual report

Please find page 194 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Financial statements

RBS Group • Annual Report and Accounts 2007

192

Notes on the accounts continued

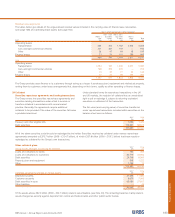

Market risk

Market risk is defined as the risk of loss resulting from adverse

changes in risk factors such as interest rates, foreign currency

and equity prices together with related factors such as market

volatilities.

The Group is exposed to market risk because of positions held

in its trading portfolios as well as its non-trading business

including the Group’s treasury operations.

Value-at-risk (“VaR”)

VaR is a technique that produces estimates of the potential

negative change in the market value of a portfolio over a

specified time horizon at given confidence levels. For internal

risk management purposes, the Group’s VaR assumes a time

horizon of one trading day and a confidence level of 95%. The

Group uses historical simulation models in computing VaR. This

approach, in common with many other VaR models, assumes

that risk factor changes observed in the past are a good

estimate of those likely to occur in the future and is, therefore,

limited by the relevance of the historical data used. The Group’s

method, however, does not make any assumption about the

nature or type of underlying loss distribution. The Group

typically uses the previous 500 trading days of market data.

The Group calculates both general market risk (i.e. the risk due

to movement in general market benchmarks) and idiosyncratic

market risk (i.e. the risk due to movements in the value of

securities by reference to specific issuers) using its VaR models.

The Group’s VaR should be interpreted in light of the

limitations of the methodology used. These limitations include:

•Historical data may not provide the best estimate of the

joint distribution of risk factor changes in the future and

may fail to capture the risk of possible extreme adverse

market movements which have not occurred in the

historical window used in the calculations.

•VaR using a one-day time horizon does not fully capture

the market risk of positions that cannot be liquidated or

hedged within one day.

•VaR using a 95% confidence level does not reflect the

extent of potential losses beyond that percentile.

The Group largely computes the VaR of trading portfolios at

the close of business and positions may change substantially

during the course of the trading day. Further controls are in

place to limit the Group’s intra-day exposure; such as the

calculation of the VaR for selected portfolios. These limitations

and the nature of the VaR measure mean that the Group

cannot guarantee that losses will not exceed the VaR amounts

indicated. The Group undertakes stress testing to identify the

potential for losses in excess of VaR.

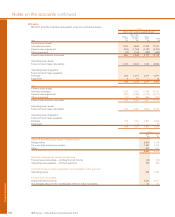

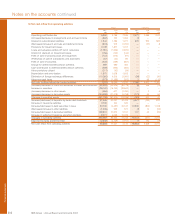

31 Risk management (continued)

Other contractual cash obligations

The table below summarises the Group’s other contractual cash obligations by payment date.

Group

0-3 months 3-12 months 1-3 years 3-5 years 5-10 years 10-20 years

2007 £m £m £m £m £m £m

Operating leases 90 268 655 569 1,060 1,958

Contractual obligations to purchase goods or services 441 1,007 748 199 5 2

531 1,275 1,403 768 1,065 1,960

2006

Operating leases 85 254 624 533 804 1,073

Contractual obligations to purchase goods or services 378 449 969 101 114 39

463 703 1,593 634 918 1,112

The Group’s undrawn formal facilities, credit lines and other commitments to lend were £335,688 million (2006 – £242,655 million).

While the Group has given commitments to provide these funds, some facilities may be subject to certain conditions being met by

the counterparty. The Group does not expect all facilities to be drawn, and some may lapse before drawdown.