RBS 2007 Annual Report Download - page 198

Download and view the complete annual report

Please find page 198 of the 2007 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Financial statements

RBS Group • Annual Report and Accounts 2007

196

Notes on the accounts continued

31 Risk management (continued)

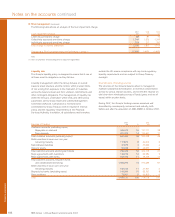

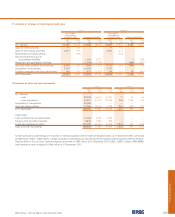

2007 2006 2005

Earned Claims Loss Earned Loss Earned Loss

premiums incurred ratio premiums ratio premiums ratio

£m £m % £m % £m %

Residential property Gross 1,087 894 82 1,121 56 1,098 55

Net 1,020 878 86 1,061 59 1,037 56

Personal motor Gross 3,254 2,616 80 3,384 84 3,312 79

Net 3,161 2,560 81 3,279 85 3,257 80

Commercial property Gross 211 116 55 218 37 212 39

Net 191 115 60 198 38 193 40

Commercial motor Gross 142 107 75 90 69 102 53

Net 133 107 80 88 68 96 46

Other Gross 851 337 40 842 47 853 63

Net 839 340 41 833 49 761 67

Total Gross 5,545 4,070 73 5,655 71 5,577 70

Net 5,344 4,000 75 5,459 73 5,344 71

The Group has no interest rate exposure from general insurance liabilities because provisions for claims under short-term insurance

contracts are not discounted.

Claims reserves

It is the Group’s policy to hold undiscounted claims reserves

(including reserves to cover claims which have been incurred

but not reported (IBNR reserves)) for all classes at a sufficient

level to meet all liabilities as they fall due.

The Group’s focus is on high volume and relatively

straightforward products, for example home and motor. This

facilitates the generation of comprehensive underwriting and

claims data, which are used to accurately price and monitor

the risks accepted.

The following table indicates the diversity of risks underwritten

and the corresponding loss ratios for each major class of

business, gross and net of reinsurance.

Frequency and severity of specific risks and

sources of uncertainty

Most general insurance contracts are written on an annual

basis, which means that the Group’s liability extends for a 12

month period, after which the Group is entitled to decline or

renew or can impose renewal terms by amending the

premium, terms and conditions, or both.

The frequency and severity of claims and the sources of

uncertainty for the key classes that the Group is exposed

to are as follows:

a) Motor insurance contracts (private and commercial)

Claims experience is quite variable, due to a wide range

of factors, but the principal ones are age, sex and driving

experience of the driver, type and nature of vehicle, use of

vehicle and area.

There are many sources of uncertainty that will affect the

Group’s experience under motor insurance, including

operational risk, reserving risk, premium rates not matching

claims inflation rates, the weather, the social, economic and

legislative environment and reinsurance failure risk.

b) Property insurance contracts (residential and commercial)

The major causes of claims for property insurance are

theft, flood, escape of water, fire, storm, subsidence and

various types of accidental damage.

The major source of uncertainty in the Group’s property

accounts is the volatility of weather. Weather in the UK can

affect most of the above perils. Over a longer period, the

strength of the economy is also a factor.

c) Other commercial insurance contracts

Other commercial claims come mainly from business

interruption and loss arising from the negligence of the

insured (liability insurance). Business interruption losses

come from the loss of income, revenue and/or profit as a

result of property damage claims. Liability insurance

includes employers liability and public/products liability.

Liability insurance is written on an occurrence basis, and is

subject to claims that are identified over a substantial

period of time, but where the loss event occurred during

the life of the policy.

Fluctuations in the social and economic climate are a

source of uncertainty in the Group’s business interruption

and general liability accounts. Other sources of uncertainty

are changes in the law, or its interpretation, and reserving

risk. Other uncertainties are significant events (for example

terrorist attacks) and any emerging new heads of damage

or types of claim that are not envisaged when the policy is

written.