Bank of America 2002 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

|

|

BANK OF AMERICA 2002 101

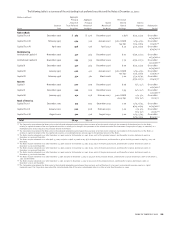

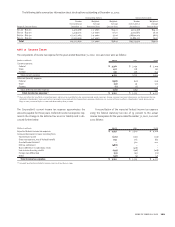

Qualified Nonqualified Postretirement

Pension Plan Pension Plans Health and Life Plans

(Dollars in millions)

2002 2001 2002 2001 2002 2001

Change in fair value of plan assets

(Primarily listed stocks, fixed income and real estate)

Fair value at January 1 $ 8,264 $8,652 $– $– $194 $ 208

Actual return on plan assets (722) (154) ––(13) (14)

Company contributions 700 500 39 98 84 69

Plan participant contributions ––––49 41

Acquisition/transfer –16 ––––

Benefits paid (724) (750) (39) (98) (133) (110)

Fair value at December 31 $ 7,518 $8,264 $– $– $181 $194

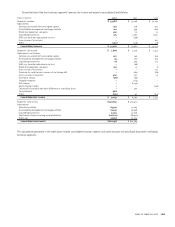

Change in projected benefit obligation

Projected benefit obligation at January 1 $ 7,606 $ 8,011 $ 529 $ 534 $ 944 $ 840

Service cost 199 202 27 22 11 11

Interest cost 540 560 44 40 67 64

Plan participant contributions ––––49 41

Plan amendments 6–(4) 2829

Actuarial loss (gain) –(434) 108 9112 69

Acquisition/transfer –17 –20 ––

Effect of curtailments ––(15) –––

Effect of special termination benefits ––2–––

Benefits paid (724) (750) (39) (98) (133) (110)

Projected benefit obligation at December 31 $ 7,627 $7,606 $ 652 $ 529 $1,058 $ 944

Funded status at December 31

Accumulated Benefit Obligation (ABO) $ 7,264 $7,263 $573 $ 459 $ N/A $ N/A

Overfunded (unfunded) status of ABO 254 1,001 (573) (459) N/A N/A

Provision for future salaries 363 343 79 70 N/A N/A

Projected Benefit Obligation (PBO) 7,627 7,606 652 529 1,058 944

Overfunded (unfunded) status of PBO $ (109) $ 658 $ (652) $ (529) $ (877) $ (750)

Unrecognized net actuarial loss 2,422 954 168 86 147 45

Unrecognized transition obligation ––11323 355

Unrecognized prior service cost 419 468 21 61 46 44

Prepaid (accrued) benefit cost $2,732 $2,080 $ (462) $ (381) $ (361) $ (306)

Weighted average assumptions at December 31

Discount rate 6.75% 7.25% 6.75% 7.25% 6.75% 7.25%

Expected return on plan assets 8.50 10.00 N/A N/A 8.50 10.00

Rate of compensation increase 4.00 4.00 4.00 4.00 N/A N/A

Net periodic pension benefit cost for the years ended December 31, 2002, 2001 and 2000, included the following components:

Qualified Pension Plan Nonqualified Pension Plans

(Dollars in millions)

2002 2001 2000 2002 2001 2000

Components of net periodic pension benefit cost (income)

Service cost $ 199 $ 202 $ 153 $27 $22 $10

Interest cost 540 560 519 44 40 39

Expected return on plan assets (746) (876) (813) –––

Amortization of transition obligation (asset) –(2) (4) ––1

Amortization of prior service cost 55 54 38 10 11 10

Recognized net actuarial loss –––11 79

Recognized loss (gain) due to settlements and curtailments –– (11) 26 6–

Net periodic pension benefit cost (income) $48 $ (62) $ (118) $ 118 $86 $69

The following table summarizes the changes in fair value of

plan assets, changes in projected benefit obligations (PBO), the

funded status of the PBO and the weighted average assumptions for

the pension plans and postretirement plans for the years ended

December 31, 2002 and 2001. Prepaid and accrued benefit costs are

reflected in other assets and other liabilities, respectively, in the

Consolidated Balance Sheet. For the Pension Plan, the asset valua-

tion method recognizes 60 percent of the market gains or losses in

the first year, with the remaining 40 percent spread equally over the

next four years. For both the Pension Plan and the Postretirement

Health and Life Plans, the expected long-term return on plan assets

will be 8.50% for 2003.