Bank of America 2002 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

44 BANK OF AMERICA 2002

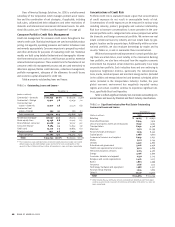

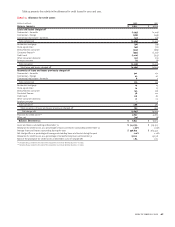

TABLE 13 Nonperforming Assets(1)

December 31

(Dollars in millions)

2002 2001

Commercial – domestic $ 2,781 $ 3,123

Commercial – foreign 1,359 461

Commercial real estate – domestic 161 240

Commercial real estate – foreign 33

Total commercial 4,304 3,827

Residential mortgage 612 556

Home equity lines 66 80

Direct/Indirect consumer 30 27

Consumer finance 19 9

Foreign consumer 67

Total consumer 733 679

Total nonperforming loans 5,037 4,506

Foreclosed properties 225 402

Total nonperforming assets $ 5,262 $ 4,908

(1) In 2002, $668 in interest income was contractually due on nonperforming loans and troubled debt restructured loans. Of this amount, $193 was actually recorded as interest income in 2002.

The Corporation has been devoting particular attention to

Argentina and Brazil, which have been significantly impacted by

negative global economic pressure.

Throughout 2001, Argentina’s economy and political environ-

ment deteriorated sharply, finally ending in December 2001 with the

collapse of the Argentine peso. As a result of these events, at the end

of 2001, the Argentine government defaulted on its obligations and

during all of 2002, local companies faced serious difficulties servicing

their debt. In response to the economic climate in Argentina, the

Corporation reduced its credit exposure in the country in 2002 by

$280 million to $465 million. Of that $465 million, $339 million

represented traditional credit exposure (loans, letters of credit, etc.)

predominantly to Argentine subsidiaries of foreign multinational

corporations. Additional credit exposure was attributable to $62 mil-

lion in Argentina government bonds. Net charge-offs in 2002 totaled

$113 million. The allowance for credit losses associated with out-

standing loans and leases related to Argentina was $154 million at

December 31, 2002.

In response to uncertain economic conditions in Brazil, the

Corporation has reduced its credit exposure by 53 percent to $1.2 bil-

lion at December 31, 2002. The decline was due to loan maturities and

lower level of local issuer risk. Of this amount, $562 million repre-

sented traditional credit exposure (loans, letters of credit, etc.) and

$290 million was Brazilian government securities. Derivatives expo-

sure totaled $55 million. The allowance for credit losses related to

Brazil consisted of $60 million related to traditional credit expo-

sure.

An additional $6 million is reserved for derivatives exposure.

Nonperforming Assets and Net Charge-offs

We routinely review the loan and lease portfolio to determine if any

credit exposure should be placed on nonperforming status. An asset

is placed on nonperforming status when it is determined that princi-

pal and interest are not expected to be fully collected in accordance

with its contractual terms. Nonperforming asset levels, presented in

Table 13, continue to be adversely affected by the weakened eco-

nomic environment. Sales of nonperforming assets during 2002

totaled $543 million, comprised of $296 million of nonperforming

commercial loans, $105 million of nonperforming residential

mortgage loans and $142 million of foreclosed properties.

In 2001 and continuing in 2002 sporadic large single company

events and issues in certain industries have impacted nonperform-

ing assets and consequently our provision for credit losses. These

losses resulted from a multitude of factors including business failures

as a result of financial reporting fraud, the prolonged weak economic

environment and industry specific issues. It is difficult to predict the

timing of such event risk and as a consequence the timing and

amount of loss potential is more difficult to estimate.

Nonperforming commercial – domestic loans decreased $342 mil-

lion to 2.65 percent of commercial – domestic loans at December 31,

2002 from 2.64 percent at December 31, 2001. Nonperforming commer-

cial – foreign loans increased $898 million to 6.83 percent of com-

mercial – foreign loans at December 31, 2002 from 2.00 percent at

December 31, 2001. The increase was primarily attributable to media

and telecommunications services firms located in Western Europe and

in Latin America.

Credit exposure to companies in the telecommunications

service industry that were in bankruptcy at December 31, 2002

totaled $190 million, with associated reserves of $44 million. Net

charge-offs associated with credit exposure to these telecommunica-

tions services companies were $105 million for 2002.

At December 31, 2002 and 2001, Argentine nonperforming loans

were $278 million and $40 million, respectively. Nonperforming loans

in Brazil were $90 million at December 31, 2002 compared to $2 mil-

lion at December 31, 2001.

Within the consumer portfolio, nonperforming loans increased

$54 million to $733 million, or 0.37 percent of consumer loans, at

December 31, 2002 from $679 million or 0.41 percent at December 31,

2001, primarily due to higher levels of residential mortgage loans

being held in the portfolio, partially offset by the sale of nonperforming

residential mortgage loans during the first quarter of 2002.

The Corporation also had approximately $4 million and $48 mil-

lion of troubled debt restructured loans at December 31, 2002 and

2001, respectively, that were accruing interest and were not included

in nonperforming assets.