Bank of America 2002 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

|

|

102 BANK OF AMERICA 2002

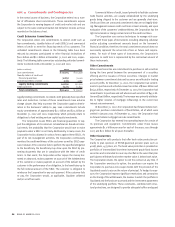

Net periodic postretirement health and life expense was determined

using the “projected unit credit” actuarial method. Gains and losses

for all benefits except postretirement health care are recognized in

accordance with the minimum amortization provisions of the applica-

ble accounting standards. For the postretirement health care plans, 50

percent of the unrecognized gain or loss at the beginning of the fiscal

year (or at subsequent remeasurement) is recognized on a level basis

during the year.

Assumed health care cost trend rates affect the postretirement

benefit obligation and benefit cost reported for the health care plan.

The assumed health care cost trend rates used to measure the

expected cost of benefits covered by the postretirement health care

plans was 10.0 percent for 2003, reducing in steps to 5.0 percent in

2006 and later years. A one-percentage-point increase in assumed

health care cost trend rates would have increased the service and

interest costs and the benefit obligation by $5 million and $61 million,

respectively, in 2002, $6 million and $52 million, respectively, in 2001

and $9 million and $49 million, respectively, in 2000. A one-percent-

age-point decrease in assumed health care cost trend rates would

have lowered the service and interest costs and the benefit obligation

by $4 million and $52 million, respectively, in 2002, $4 million and

$45 million, respectively, in 2001 and $7 million and $40 million,

respectively, in 2000.

Defined Contribution Plans

The Corporation maintains a qualified defined contribution retirement

plan and a nonqualified defined contribution retirement plan. There

are two components of the qualified defined contribution plan, the

Bank of America 401(k) Plan (the “401(k) Plan”): an employee stock

ownership plan (ESOP) and a profit-sharing plan. Prior to 2001, the

ESOP component of the 401(k) Plan featured leveraged ESOP

provisions. See Note 14 of the consolidated financial statements for

additional information on the ESOP provisions.

The Corporation contributed approximately $200 million, $196 mil-

lion, and $163 million for 2002, 2001 and 2000, respectively, in cash and

stock which was utilized primarily to purchase the Corporation’s com-

mon stock under the terms of the 401(k) Plan. At December 31, 2002

and 2001, an aggregate of 44 million shares and 45 million shares,

respectively, of the Corporation’s common stock and 1 million shares and

2 million shares, respectively, of ESOP preferred stock were held by the

Corporation’s 401(k) Plan.

Under the terms of the ESOP Preferred Stock provision, payments

to the plan for dividends on the ESOP Preferred Stock were $5 million

for both 2002 and 2001 and $6 million for 2000. Payments to the plan

for dividends on the ESOP Common Stock were $34 million, $27 mil-

lion, and $22 million during the same periods. Interest incurred to

service the debt of the ESOP Preferred Stock and ESOP Common Stock

amounted to $0.3 million and $3 million for 2001 and 2000, respec-

tively. As of December 31, 2001, all principal and interest associated

with the debt of the ESOP Preferred Stock and ESOP Common Stock

have been repaid.

In addition, certain non-U.S. employees within the Corporation

are covered under defined contribution pension plans that are sepa-

rately administered in accordance with local laws.

NOTE 17 Stock Incentive Plans

At December 31, 2002, the Corporation had certain stock-based

compensation plans which are described below. For all stock-based

compensation awards issued prior to January 1, 2003, the Corporation

applies the provisions of Accounting Principles Board Opinion No. 25,

“Accounting for Stock Issued to Employees,” in accounting for its

stock option and award plans. Stock-based compensation plans

enacted after December 31, 2002 will be accounted for under the

provisions of SFAS 123. For additional information on the accounting

for stock-based compensation plans and pro forma disclosures, see

Note 1 of the consolidated financial statements.

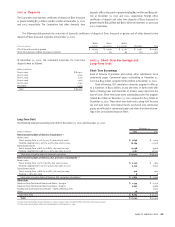

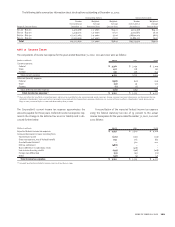

For the years ended December 31, 2002, 2001 and 2000, net periodic postretirement benefit cost included the following components:

(Dollars in millions)

2002 2001 2000

Components of net periodic postretirement benefit cost (income)

Service cost $11 $11 $11

Interest cost 67 65 58

Expected return on plan assets (17) (21) (20)

Amortization of transition obligation 32 32 37

Amortization of prior service cost (credit) 64 (3)

Recognized net actuarial loss (gain) 40 20 (45)

Recognized loss due to settlements and curtailments ––20

Net periodic postretirement benefit cost $139 $ 111 $ 58