Bank of America 2002 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 41

Because we provide liquidity and credit support to these financ-

ing entities, our credit ratings and changes thereto will affect the

borrowing cost and liquidity of these entities. In addition, significant

changes in counterparty asset valuation and credit standing may also

affect the liquidity of the commercial paper issuance. Disruption in

the commercial paper markets may result in our having to fund under

these commitments and SBLCs discussed above. We manage these

risks, along with all other credit and liquidity risks, within our policies

and practices. See Notes 1 and 8 of the consolidated financial state-

ments for additional discussion of off-balance sheet financing entities.

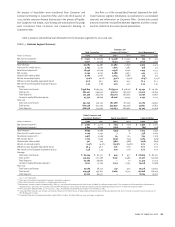

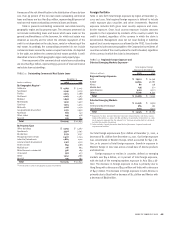

Capital Management

The final component of liquidity risk is capital management, which

focuses on the level of shareholders’ equity. Period-end shareholders’

equity increased from a year ago, driven by net income, shares issued

under employee plans and unrealized gains on securities. These

increases were offset by share repurchases and dividends paid. The

net impact of share repurchases and issuances under employee plans

to earnings per share was $0.11 per share in 2002. We anticipate that

future share repurchases will at least equal shares issued under our

various stock option plans. See Note 14 of the consolidated financial

statements for additional disclosures related to repurchase programs.

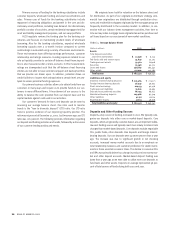

As a regulated financial services company, we are governed by

certain regulatory capital requirements. The regulatory Tier 1 Capital

Ratio was 8.22 percent at December 31, 2002, a decrease of eight

basis points from a year ago. The minimum Tier 1 Ratio required is

four percent. At December 31, 2002, the Corporation was classified

as well-capitalized for regulatory purposes, the highest classification.

Our current estimate of the possible impact on our capital ratios

of the FASB’s new rule on accounting for off-balance sheet financing

entities, as previously discussed, is 25-30 basis points. For additional

information on the regulatory capital ratios along with a description

of the components of risk-based capital, capital adequacy require-

ments and prompt corrective action provisions, see Note 15 of the

consolidated financial statements.

On October 23, 2002, the Board approved a $0.04 per share, or

seven percent, increase in the quarterly common dividend. This

increase brings the common dividend to $0.64 per share for the fourth

quarter of 2002 and $2.44 for the year ended December 31, 2002.

The Corporation from time to time sells put options on its com-

mon stock to independent third parties. The put option program was

undertaken with the goal of partially offsetting the cost of share repur-

chases. At December 31, 2002, there were 6.5 million put options out-

standing with exercise prices ranging from $61.86 per share to $70.72

per share, which expire from February 2003 to July 2003. Should the

outstanding options at December 31, 2002 be exercised in the future,

the per-share cost to the Corporation, net of the premium already

received, will range from $54.87 to $64.07, or a weighted average of

$58.68. The closing market price of the Corporation’s common stock

on December 31, 2002 was $69.57 per share.

Economic capital is allocated to business units based on an

assessment of risk. The allocated amount of capital varies according to

the characteristics of the individual product offerings within the busi-

ness units. Capital is allocated separately based on the following types

of risk: credit, market and operational. Average total economic capital

allocated to business units was $35.1 billion in 2002 and $39.2 billion in

2001. Average unallocated economic capital (not allocated to business

units) was $12.5 billion in 2002 and $9.4 billion in 2001.

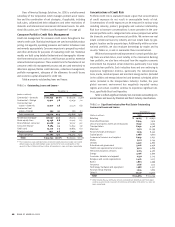

Credit Risk Management

Credit risk arises from the inability of a customer to meet its repay-

ment obligation.Credit risk exists in our outstanding loans and leases,

derivative assets, letters of credit and financial guarantees, accept-

ances and unfunded loan commitments. For additional information on

derivatives and credit extension commitments, see Notes 5 and 13 of

the consolidated financial statements. Credit exposure (defined to

include loans and leases, letters of credit, derivatives, acceptances,

assets held for sale and binding unfunded commitments) associated

with a client represents the maximum loss potential arising from all

these product classifications. Our commercial and consumer credit

extension and review procedures take into account credit exposures

that are both funded and unfunded.

We manage credit risk associated with our business activities

based on the risk profile of the borrower, repayment source and the

nature of underlying collateral given current events and conditions.

At a macro level we segregate our loans in two major groups – com-

mercial and consumer.

Commercial Portfolio Credit Risk Management

Commercial credit risk management begins with an assessment of the

credit risk profile of an individual borrower (or counterparty) based on

an analysis of the borrower’s financial position in conjunction with cur-

rent industry and economic or geopolitical trends. As part of the overall

credit risk assessment of a borrower, each commercial credit exposure

is assigned a risk rating and is subject to approval based on existing

credit approval standards. Risk ratings are a factor in determining the

level of assigned economic capital and the allowance for credit losses.

Credit decisions are determined by the lines of business with approvals

from Risk Management. In making decisions regarding credit we con-

sider risk rating, collateral, and industry and single name concentration

limits while also balancing the total client relationship and SVA.

Credit exposures are continuously monitored by both lines of

business and Risk Management personnel for possible adjustment if

there has been a change in a borrower/counterparty’s ability to per-

form under its obligations. Additionally, we manage the size of our

credit exposure through syndications, loan sales, credit derivatives

and securitizations. These activities play an important role in reducing

credit exposures where it has been determined that credit risk con-

centrations are unacceptable or for other risk mitigation purposes.