Bank of America 2002 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 87

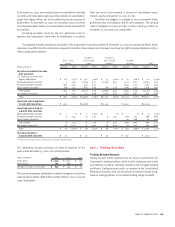

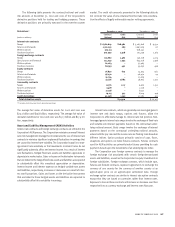

The following table presents the contract/notional and credit

risk amounts at December 31, 2002 and 2001 of the Corporation’s

derivative positions held for trading and hedging purposes. These

derivative positions are primarily executed in the over-the-counter

market. The credit risk amounts presented in the following table do

not consider the value of any collateral held but take into considera-

tion the effects of legally enforceable master netting agreements.

Derivatives(1)

December 31, 2002 December 31, 2001

Contract/ Credit Contract/ Credit

(Dollars in millions)

Notional Risk Notional Risk

Interest rate contracts

Swaps $ 6,781,629 $ 18,981 $ 5,267,608 $ 9,550

Futures and forwards 2,510,259 283 1,663,109 67

Written options 973,113 – 678,242 –

Purchased options 907,999 3,318 704,159 2,165

Foreign exchange contracts

Swaps 175,680 2,460 140,778 2,274

Spot, futures and forwards 724,039 2,535 654,026 2,496

Written options 81,263 – 57,963 –

Purchased options 80,395 452 55,050 496

Equity contracts

Swaps 16,830 679 14,504 562

Futures and forwards 48,470 – 46,970 44

Written options 19,794 – 21,009 –

Purchased options 23,756 2,885 28,902 2,511

Commodity contracts

Swaps 11,776 1,117 6,600 1,152

Futures and forwards 3,478 – 2,176 –

Written options 12,158 – 8,231 –

Purchased options 19,115 347 8,219 199

Credit derivatives 92,098 1,253 57,182 631

Total derivative assets $ 34,310 $ 22,147

(1) Includes both long and short derivative positions.

The average fair value of derivative assets for 2002 and 2001 was

$25.3 billion and $19.8 billion, respectively. The average fair value of

derivative liabilities for 2002 and 2001 was $17.3 billion and $17.4 bil-

lion, respectively.

Asset and Liability Management (ALM) Activities

Interest rate contracts and foreign exchange contracts are utilized in the

Corporation’s ALM process. The Corporation maintains an overall interest

rate risk management strategy that incorporates the use of interest rate

contracts to minimize significant unplanned fluctuations in earnings that

are caused by interest rate volatility. The Corporation’s goal is to man-

age interest rate sensitivity so that movements in interest rates do not

significantly adversely affect net interest income. As a result of interest

rate fluctuations, hedged fixed-rate assets and liabilities appreciate or

depreciate in market value. Gains or losses on the derivative instruments

that are linked to the hedged fixed-rate assets and liabilities are expected

to substantially offset this unrealized appreciation or depreciation.

Interest income and interest expense on hedged variable-rate assets

and liabilities, respectively, increases or decreases as a result of inter-

est rate fluctuations. Gains and losses on the derivative instruments

that are linked to these hedged assets and liabilities are expected to

substantially offset this variability in earnings.

Interest rate contracts, which are generally non-leveraged generic

interest rate and basis swaps, options and futures, allow the

Corporation to effectively manage its interest rate risk position. Non-

leveraged generic interest rate swaps involve the exchange of fixed-rate

and variable-rate interest payments based on the contractual under-

lying notional amount. Basis swaps involve the exchange of interest

payments based on the contractual underlying notional amounts,

where both the pay rate and the receive rate are floating rates based on

different indices. Option products primarily consist of caps, floors,

swaptions and options on index futures contracts. Futures contracts

used for ALM activities are primarily index futures providing for cash

payments based upon the movements of an underlying rate index.

The Corporation uses foreign currency contracts to manage the

foreign exchange risk associated with certain foreign-denominated

assets and liabilities, as well as the Corporation’s equity investments in

foreign subsidiaries. Foreign exchange contracts, which include spot,

futures and forward contracts, represent agreements to exchange the

currency of one country for the currency of another country at an

agreed-upon price on an agreed-upon settlement date. Foreign

exchange option contracts are similar to interest rate option contracts

except that they are based on currencies rather than interest rates.

Exposure to loss on these contracts will increase or decrease over their

respective lives as currency exchange and interest rates fluctuate.