Bank of America 2002 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

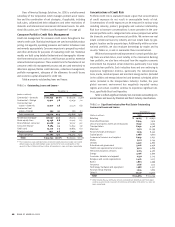

Interest Rate Risk Management

Our ALM process, managed through ALCO, is used to manage interest

rate risk associated with non-trading financial instruments. Interest

rate risk represents the most significant market risk exposure to our

non-trading financial instruments.

Our overall goal is to manage interest rate sensitivity so that

movements in interest rates do not adversely affect net interest

income. Interest rate risk is measured as the potential volatility to our

net interest income caused by changes in market interest rates. In

managing interest rate risk of our non-trading financial instruments

we look at two broad portfolios – non-discretionary and discretionary.

The non-discretionary portfolio consists of our customer-driven loan

and deposit positions and securities required to support legal and

regulatory requirements. To manage the resulting interest rate sensitiv-

ity of the non-discretionary portfolio, we utilize a discretionary portfo-

lio of securities, residential mortgage loans and derivatives.

Strategically positioning our discretionary portfolio allows us to man-

age the interest rate sensitivity in our non-discretionary portfolio.

Complex sensitivity simulations are used to estimate the impact

on net interest income of numerous interest rate scenarios, balance

sheet trends and strategies. These simulations estimate levels of

short-term financial instruments, securities, loans, deposits, borrow-

ings and ALM derivative instruments. In addition, these simulations

incorporate assumptions about balance sheet dynamics such as loan

and deposit growth and pricing, changes in funding mix and asset

and liability repricing and maturity characteristics. In addition to net

interest income sensitivity simulations, market value sensitivity

measures are also utilized.

The Balance Sheet Management division maintains a net interest

income forecast utilizing different rate scenarios, including a most

likely scenario. The most likely scenario is designed around an eco-

nomic forecast that is meant to estimate our expectation of the most

likely path of rates for the upcoming horizon. The Balance Sheet

Management division constantly updates the net interest income

forecast for changing assumptions and differing outlooks based on

actual results.

Net interest income risk is measured based on rate shocks over

different time horizons versus a current stable interest rate environ-

ment. Assumptions used in these calculations are similar to those

used in our corporate planning and forecasting process. The overall

interest rate risk position and strategies are reviewed on an ongoing

basis with ALCO and other committees as appropriate. Table 19 pro-

vides our estimated net interest income at risk over the subsequent

year from December 31, 2002 and 2001 resulting from a 100 basis

point gradual (over 12 months) increase or decrease in interest rates.

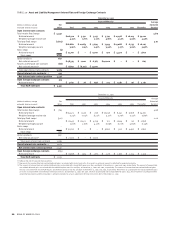

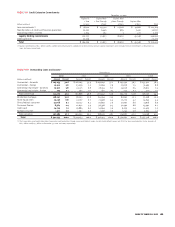

TABLE 19 Estimated Net Interest Income at Risk

-100 bp +100 bp

December 31, 2002 (2.4)% 1.5%

December 31, 2001 (0.8) 0.4

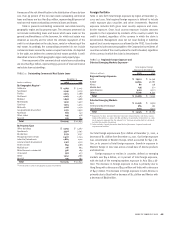

Securities

The securities portfolio is integral to our ALM activities. The decision

to purchase or sell securities is based upon the current assessment of

economic and financial conditions, including the interest rate

environment, liquidity and regulatory requirements and on- and off-

balance sheet positions. The securities portfolio at December 31,

2002 ended down from a year ago. In 2002, we purchased securities of

$146 billion, sold $137 billion and received paydowns of $25 billion.

During the year, we continuously monitored the interest rate risk

position of the portfolio and repositioned the securities portfolio in

order to manage convexity risk and to take advantage of interest rate

fluctuations. Through sales of the securities portfolio, we realized

$630 million in gains on sales of securities during the year.

Residential Mortgage Portfolio

We repositioned the discretionary mortgage loan portfolio to manage

prepayment risk resulting from the unusually low rate environment.

The residential mortgages designated solely for ALM activities grew

primarily through whole loan purchase activity. In 2002, we purchased

$55.0 billion of residential mortgages in the wholesale market for our

discretionary portfolio and interest rate risk management. During the

same period, we sold $22.7 billion of whole mortgage loans and recog-

nized $500 million in gains on the sales.

Interest Rate and Foreign Exchange Derivative Contracts

Interest rate derivative contracts and foreign exchange derivative

contracts are utilized in our ALM process. We use derivatives as an effi-

cient, low-cost tool to manage our interest rate risk. We use derivatives

to hedge or offset the changes in cash flows or market values of our

balance sheet. See Note 5 of the consolidated financial statements for

additional information on the Corporation’s hedging activities.

Our interest rate contracts are generally non-leveraged generic

interest rate and basis swaps, options, futures and forwards. In

addition, we use foreign currency contracts to manage the foreign

exchange risk associated with foreign-denominated assets and

liabilities, as well as our equity investments in foreign subsidiaries.

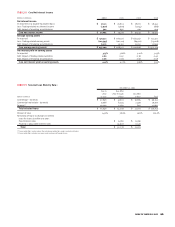

Table 20 reflects the notional amounts, fair value, weighted average

receive fixed and pay fixed rates, expected maturity and estimated

duration of our ALM derivatives at December 31, 2002 and 2001.

Management believes the fair value of the ALM interest rate and for-

eign exchange portfolios should be viewed in the context of the com-

bined discretionary and non-discretionary portfolios.

BANK OF AMERICA 2002 51