Bank of America 2002 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 53

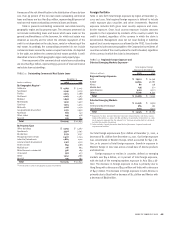

Consistent with our strategy of managing interest rate sensitivity, the net

receive fixed interest rate swap position increased by $11.8 billion to

$54.8 billion at December 31, 2002. This increase primarily occurred in

the last half of 2002. Option products in our ALM process may

include option collars or spread strategies, which involve the buying

and selling of options on the same underlying security or interest rate

index. These strategies may involve caps, floors and options on index

futures contracts.

The Corporation adopted SFAS 133 on January 1, 2001. SFAS 133

requires that all derivative instruments be recorded on the balance

sheet at their fair value. We have not significantly altered our overall

interest rate risk management objective and strategy as a result of

adopting SFAS 133. For further information on SFAS 133, see Note 1 of

the consolidated financial statements.

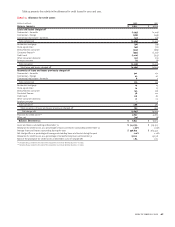

Mortgage Banking Risk

Mortgage production activities create unique interest rate and prepay-

ment risk between the loan commitment date (pipeline) and the date the

loan is sold to the secondary market. To manage interest rate risk, we

enter into various financial instruments including interest rate

swaps, forward delivery contracts, Euro dollar futures and option con-

tracts. The notional amount of such contracts was $25.3 billion at

December 31, 2002 with associated net unrealized losses of $224 mil-

lion. At December 31, 2001, the notional amount of such contracts was

$27.8 billion with associated net unrealized gains of $69 million. These

contracts have an average expected maturity of less than 90 days.

Prepayment risk represents the loss in value associated with a

high rate loan paying off in a low rate environment and the loss of

servicing value when loans prepay. We manage prepayment risk using

various financial instruments including purchased options and swaps.

The notional amounts of such contracts at December 31, 2002 and

2001 were $53.1 billion and $65.1 billion, respectively. The related

unrealized gain was $955 million and $301 million at December 31,

2002 and 2001, respectively. These amounts are included in the

Derivatives table in Note 5 of the consolidated financial statements.

See Note 1 for additional discussion of these financial instruments in

the mortgage banking assets section.

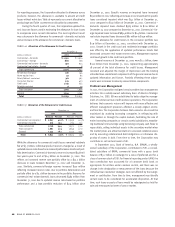

Operational Risk Management

Operational risk is the potential for loss resulting from events involv-

ing people, processes, technology, legal/regulatory issues, external

events, execution and reputation. Successful operational risk man-

agement is particularly important to a diversified financial services

company like ours because of the very nature, volume and complexity

of our various businesses.

In keeping with the corporate governance structure, the lines of

businesses are responsible for all the risks within the business includ-

ing operational risks. Such risks are managed through corporate wide

or business segment specific policies and procedures, controls and

monitoring tools. Examples of these include personnel management

practices, data reconciliation processes, fraud management units,

transaction processing monitoring and analysis, systems interruptions

and new product introduction processes.

The Corporate Operational Risk Executive, reporting to the Chief

Risk Officer, provides oversight to accelerate and facilitate consistency

of effective policies, best practices, controls and monitoring tools for

managing and assessing all types of operational risks across the

company. The Operational Risk Executive also works with the busi-

ness segment executives and their risk counterparts to implement

appropriate policies, processes and assessments at the segment

level. In addition, the Corporate Audit group places special emphasis

on operational risk management processes, at both the corporate

and segment levels, in its assessments and testing.

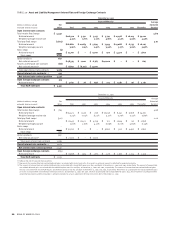

Operational risks fall into two major categories, business specific

and corporate-wide affecting all business lines. Operational Risk

Management plays a different role in each category. For business

specific risks, Operational Risk Management works with the seg-

ments to ensure consistency in policies, processes, and assessments.

With respect to corporate-wide risks, such as information security,

business recovery, legal and compliance, Operational Risk

Management assesses the risks, develops a consolidated corporate

view and communicates that view to the business level.

At the business segment level, there are four business segment

risk executives that are responsible for oversight of all operational

risks in the business segments they support. In their management of

these specific risks, they utilize corporate-wide operational risk poli-

cies, processes, and assessments. A specific example is our manage-

ment of outsourced activities. To ensure that we meet our business

segment objectives and manage the risks associated with these

activities, vendor contracts contain specific corporate standards that

allow for the tracking of service performance levels. In addition, we

also have our Corporate Audit group perform independent assess-

ments of vendor management processes and key vendor processes,

the latter including on-site work at our more significant vendors.

To manage corporate-wide risks, we maintain specialized sup-

port groups, such as Legal, Information Security, Business Recovery,

Supply Chain Management, Finance, Compliance and Technology and

Operations. These groups assist the lines of business in the devel-

opment and implementation of risk management practices specific

to the needs of the individual businesses. An example of such an

effort is our company-wide implementation of the anti-money laun-

dering aspects of the USA Patriot Act.

Operational Risk Management, working in conjunction with sen-

ior business segment executives, has developed two key tools to help

manage, monitor, and summarize operational risk. The first tool the

businesses and executive management utilize is a company-wide

quarterly self-assessment process, which identifies and evaluates the

status of risk issues, including mitigation plans if appropriate. The

goal of this process, which originates at the segment level, is to

ensure that the overall operating environment for segments is being

continuously assessed and appropriately enhanced for changing

conditions. This self-assessment is also used for identifying emerging

operational risk issues and determining how they should be managed

– at the business segment or corporate level. The risks identified in

this process are also integrated into our quarterly financial forecasting

process. The second process is a metrics review of key risk indicators.

Each business has identified metrics for each category of operational

risk noted above. The resulting review is used to identify trends and

issues on both a corporate and a segment level.