Bank of America 2002 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 37

Risk Management Controls

We use various controls to manage risks at the line of business level and

corporate-wide. For example, our planning and forecasting process facil-

itates analysis of results versus plan and provides early indication of

unplanned risk levels. Various line of business risk committees and

forums are comprised of line personnel, Risk Management and other

groups responsible for the internal control infrastructure (i.e. Finance,

Legal, Compliance, Tax and/or Corporate Audit). Limits, the amount of

exposure that may be taken in a product, relationship, region or indus-

try, are set based on metrics thereby aligning our risk goals with those

of each line of business. Models are used to estimate market and net

interest income sensitivity. Modeling is used to estimate both expected

and unexpected credit losses for each product and line of business. We

employ hedging strategies to reduce concentrations and improve port-

folio granularity and to manage interest rate risk in the portfolio. We

have continued to strengthen the linkage between the associate per-

formance management process and individual compensation to help

associates work toward corporate wide goals. Finally, compliance plays

a significant role in aiding our business units in risk management.

Formal processes used in managing risk only represent one

side of the equation. Corporate culture and the actions of our associ-

ates are critical to effective risk management. Through our recently

updated Code of Ethics, we set a high standard for our associates.

The Code of Ethics provides a framework for all of our associates to

conduct themselves with the highest integrity in the delivery of their

product or service to our customers.

The following sections, Liquidity Risk Management, Credit Risk

Management beginning on page 41, Market Risk Management begin-

ning on page 49 and Operational Risk Management beginning on page

53, address in more detail the specific procedures, measures and

analyses of the four categories of risk that we manage.

Liquidity Risk Management

Liquidity Risk

Liquidity is the ongoing ability to accommodate liability maturities and

withdrawals, fund asset growth and otherwise meet contractual obli-

gations through generally unconstrained access to funding at reason-

able market rates. Liquidity management involves maintaining ample

and diverse funding capacity, liquid assets and other sources of cash

to accommodate fluctuations in asset and liability levels due to busi-

ness shocks or unanticipated events.

We manage liquidity at two primary levels. The first level is the

liquidity of the parent company, which is the holding company that

owns the banking and non-banking subsidiaries. The second level is

the liquidity of the banking subsidiaries. The management of liquidity

at both levels is essential because the parent company and banking

subsidiaries each have different funding needs and sources and each

are subject to certain regulatory guidelines and requirements. The

Finance Committee is responsible for establishing our liquidity policy

as well as approving operating and contingency procedures and

monitoring liquidity on an ongoing basis, both of which may be del-

egated to ALCO. Corporate Treasury is responsible for planning and

executing our funding activities and strategy.

A primary objective of liquidity risk management is to provide a

planning mechanism for unanticipated changes in the demand or need

of liquidity created by customer behavior or capital market conditions.

In order to achieve this objective, liquidity management and business

unit activities are managed consistent with a strategy of funding stabil-

ity, flexibility and diversity. We emphasize maximizing and preserving

customer deposits and other customer-based funding sources. Deposit

rates and levels are monitored, and trends and significant changes are

reported to ALCO and the Finance Committee. Deposit marketing

strategies are reviewed for consistency with our liquidity policy objec-

tives. Asset securitization also enhances funding diversity and stability

and is considered a critical source of contingency funding.

We develop and maintain contingency funding plans that sepa-

rately address the parent company and banking subsidiaries liquidity.

These plans evaluate market-based funding capacity under various

levels of market conditions and specify actions and procedures to be

implemented under liquidity stress. Further, these plans address

alternative sources of liquidity, measure the overall ability to fund our

operations and define roles and responsibilities for effectively manag-

ing liquidity through a problem period.

Our borrowing costs and ability to raise funds are directly

impacted by our credit ratings and changes thereto. The credit rat-

ings of the Corporation and Bank of America, N.A. are reflected in

the table below.

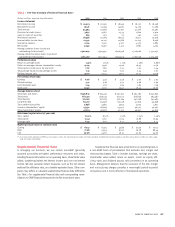

TABLE 4 Credit Ratings

Bank of America Corporation Bank of America, N.A.

Commercial Senior Subordinated

Paper Debt Debt Short-Term Long-Term

Moody’s P-1 Aa2 Aa3 P-1 Aa1

S & P A-1 A+ A A-1+ AA-

Fitch, Inc. F1+ AA- A+ F1+ AA

Primary sources of funding for the parent company include dividends

received from its banking subsidiaries and proceeds from the

issuance of senior and subordinated debt, commercial paper and

equity. Primary uses of funds for the parent company include repay-

ment of maturing debt and commercial paper, share repurchases,

dividends paid to shareholders and subsidiary funding.

Parent company liquidity is maintained at levels sufficient to fund

holding company and non-bank affiliate operations during various

stress scenarios in which access to normal funding sources is dis-

rupted. The primary measure used in assessing the parent company’s

liquidity is “Time to Required Funding” in a stress environment. This

measure assumes that the parent company is unable to generate

funds from debt or equity issuance, receives no dividend income from

subsidiaries, and no longer pays dividends to shareholders. Projected

liquidity demands are met with available liquidity until the liquidity is

exhausted. Under this scenario, the amount of time which elapses

before the current liquid assets are exhausted is considered the Time

to Required Funding. ALCO approves the target range set for this

metric and monitors adherence to the target. In order to remain in the

target range, management uses the Time to Required Funding meas-

urement to determine the timing and extent of future debt issuances

and other actions.