Bank of America 2002 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

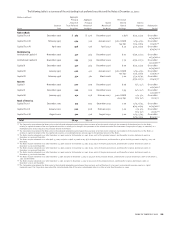

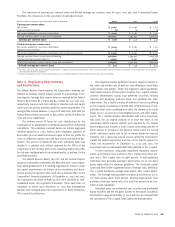

BANK OF AMERICA 2002 91

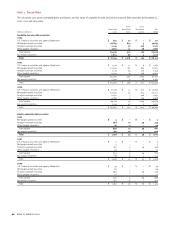

December 31, 2002 December 31, 2001

Total Principal Principal Principal Total Principal Principal Principal

Amount of Amount of Loans Amount of Amount of Amount of Loans Amount of

Loans and Past Due Nonperforming Loans and Past Due Nonperforming

(Dollars in millions)

Leases 90 Days or More

(1)

Loans Leases 90 Days or More

(1)

Loans

Commercial – domestic $ 105,053 $ 132 $ 2,781 $ 120,159 $ 175 $ 3,123

Commercial – foreign 19,912 – 1,359 23,039 6 461

Commercial real estate – domestic 19,910 91 161 22,271 40 240

Commercial real estate – foreign 295 – 3 383 – 3

Total commercial 145,170 223 4,304 165,852 221 3,827

Residential mortgage 108,197 – 612 78,203 14 556

Home equity lines 23,236 – 66 22,107 – 80

Direct/Indirect consumer 31,068 56 30 30,317 67 27

Consumer finance 8,384 61 19 12,652 46 9

Credit card 29,461 502 – 27,186 475 –

Foreign consumer 1,971 – 6 2,092 – 7

Total consumer 202,317 619 733 172,557 602 679

Total managed loans and leases 347,487 $ 842 $ 5,037 338,409 $ 823 $ 4,506

Loans in revolving securitizations (4,732) (9,256)

Total held loans and leases $ 342,755 $329,153

Year Ended December 31, 2002 Year Ended December 31, 2001

Average Average

Loans and Loans and Loans and Loans and

Leases Leases Net Net Loss Leases Leases Net Net Loss

(Dollars in millions)

Outstanding Losses Ratio

(2)

Outstanding Losses Ratio

(2)

Commercial – domestic $ 110,073 $ 1,471 1.34% $135,750 $ 1,949 1.44%

Commercial – foreign 21,287 521 2.45 26,492 208 0.78

Commercial real estate – domestic 21,161 37 0.18 24,607 39 0.16

Commercial real estate – foreign 408 – – 348 – –

Total commercial 152,929 2,029 1.33 187,197 2,196 1.17

Residential mortgage 97,204 42 0.04 81,472 26 0.03

Home equity lines 22,807 26 0.11 22,013 19 0.09

Direct/Indirect consumer 30,264 210 0.69 30,374 250 0.82

Consumer finance 10,533 255 2.42 27,709 1,026 3.70

Credit card 27,352 1,443 5.28 24,637 1,174 4.76

Other consumer – domestic – 36 n/m – 50 n/m

Foreign consumer 2,021 5 0.25 2,222 5 0.22

Total consumer 190,181 2,017 1.06 188,427 2,550 1.35

Total managed loans and leases 343,110 $ 4,046 1.18% 375,624 $ 4,746 1.26%

Loans in revolving securitizations (6,291) (10,177)

Total held loans and leases $336,819 $365,447

n/m = not meaningful

(1) Excludes consumer real estate loans (which are placed on nonperforming status at 90 days past due).

(2) The net loss ratio is calculated by dividing managed loans and leases net losses by average managed loans and leases outstanding for each loan and lease category.

The Corporation reviews its loan and lease portfolio on a

managed basis. Managed loans and leases are defined as on-balance

sheet loans and leases as well as securitized credit card loans. New

advances under these previously securitized balances will be recorded

on the Corporation’s balance sheet after the revolving period of the

securitization, which has the effect of increasing loans on the

Corporation’s balance sheet and increasing net interest income and

charge-offs, with a corresponding reduction in noninterest income.

Portfolio balances, delinquency and historical loss amounts of the

managed loan and lease portfolio for 2002 and 2001 were as follows: