Bank of America 2002 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

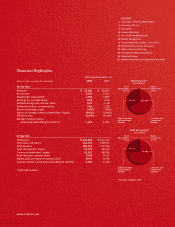

we pursue our long-term goal of 7% to 9% annual revenue

growth. Earnings per share (EPS) were $5.91, shareholder

value added (SVA) was $3.76 billion, and return on equity

(ROE) was 19.4%; these results compared, respectively,

to $4.18, $3.09 billion and 14.0% in 2001.

The result is a stock price for your company that continues

to climb. In 2002, it increased 10.5% to $69.57 at year-end,

a strong gain on top of a 2001 increase of 37%. Over a

three-year period, Bank of America ranks number one in its

peer group with a 15.9% average total shareholder return,

including both stock price gains and dividends.

Returning capital to shareholders continues to be a

priority. In October, the board approved a 7% increase in

the quarterly dividend to $0.64, or $2.56 annually, repre-

senting a 3.7% dividend yield based on our stock price at

the end of the year. In addition, we repurchased 109 million

shares of stock in 2002, and the board authorized further

repurchases of up to 130 million shares within 24 months

at its January 22, 2003 meeting.

As in 2001, our Consumer and Commercial Banking

business (CCB) led the way for our company, with par-

ticularly strong growth in card income, mortgage banking

income and deposits. Our results in these businesses

demonstrate the tremendous strength of CCB as a growth

engine for our company.

CCB posted earnings of $6.09 billion, up from $4.95

billion a year earlier. Revenue growth in CCB was 9%,

including growth of 8% in card income and 27% in mortgage

banking income. Average deposits grew 6% and consumer

loans increased 16%. We also achieved significant growth in

our customer base as net new checking accounts increased by

more than half a million and active users of Online Banking

surged to more than 4.7 million. Commercial loan levels

declined 12% as companies paid down loan balances.

We also took steps this year to open new markets and

to expand our customer base in the consumer and small

business segments.

Last fall, we announced plans to open up to 550 new

banking centers over the next three years, including 15

new banking centers in Chicago in the coming year.

Banking centers continue to be the dominant channel

for the creation of new banking relationships, and we

are opening these centers in markets that offer the best

potential for new growth.

In December, we agreed to purchase a 24.9% stake in

Grupo Financiero Santander Serfin (GFSS), the subsidiary

of Santander Central Hispano in Mexico, for $1.6 billion.

GFSS is the third-largest and most profitable banking

organization in Mexico. The transaction is expected to close

in the first quarter of 2003.

This investment was driven by our desire to better

serve Hispanic customers within our U.S. franchise and to

increase our presence in all our Hispanic communities. Our

relationship with GFSS will enable us to better understand

our Hispanic customers, enhance our products and services

and position Bank of America as the bank of choice for the

Mexican-American population in our key markets. Finally,

the investment met our stated financial hurdles and will be

accretive to earnings in 2003.

Our Global Corporate and Investment Banking business

(GCIB), by focusing on clients in industry sectors with

high growth potential and where we have specific expertise,

gained market share in almost all of its major product and

service categories. In particular, we gained ground in

advisory services, equity offerings, convertibles, high-grade

debt and asset-backed securities.

Global Treasury Services continued to provide a strong,

steady income stream for GCIB with a 26% increase in net

income. Investment banking fees of $1.5 billion fell only

3% from last year, even as fees across the industry fell by

double digits. Despite strong performance in GCIB relative

to our competitors, lower demand in market-sensitive

businesses (including a significant decline in trading profits),

coupled with continued high credit losses, resulted in net

income of $1.72 billion, a 12% decline from last year.

Results in the Asset Management Group (AMG) also were

deeply affected by the challenging economy generally and the

double-digit decline in the stock market specifically. Net income

from AMG fell 23% from a year ago to $404 million, primarily

due to weak market activity and one large credit charge-off.

These results masked important accomplishments for the

business. Our mutual funds investment results put us among

the leading performers in 2002, and assets under management

remained stable at $310 billion while, again, major market

indices fell sharply. AMG also made strong gains on its great-

est priority: expanding distribution by increasing the number

of advisors serving clients. Our goal was to increase our force

of financial advisors by 20% — a goal we surpassed in 2002.

3

BANK OF AMERICA 2002