Bank of America 2002 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 45

Commercial – domestic loans past due 90 days or more and still

interest were $223 million and $215 million at December 31, 2002 and

2001, respectively. Consumer loans past due 90 days or more and still

accruing interest were $541 million and $459 million at December 31,

2002 and 2001, respectively.

As a matter of corporate practice, we do not discuss specific client

relationships; however, due to the publicity and interest surrounding

Enron Corporation and its related entities (Enron), we made an excep-

tion. In the fourth quarter of 2001, our total exposure to Enron was

$503 million before a charge-off of $210 million, as well as a $21 million

write-off of Enron securities related to a collateralized loan obligation.

During 2002, the Corporation had an additional $48 million of charge-

offs related to Enron. The Corporation’s exposure (after charge-offs)

related to Enron was $185 million and $272 million at December 31,

2002 and 2001, respectively, of which $136 million and $184 million

was secured. Nonperforming loans related to Enron were $159 million

and $226 million at December 31, 2002 and 2001, respectively.

The Corporation also has other assets that represent possible

credit risk. Included in Other Assets are loans held for sale and lever-

aged lease partnership interests of $13.8 billion and $387 million,

respectively, at December 31, 2002 and $8.4 billion and $485 million,

respectively, at December 31, 2001. Included in these balances are

nonperforming loans held for sale and leveraged lease partnership

interests of $118 million and $2 million, respectively, at December 31,

2002 and $1.0 billion and $0, respectively, at December 31, 2001.

The Corporation utilizes actual loan net charge-offs in its analysis

of the adequacy of the allowance for credit losses. Net charge-offs are

presented in Table 15.

Commercial – domestic loan net charge-offs decreased $478 mil-

lion in 2002 compared to 2001, primarily due to lower domestic gross

charge-offs in Global Corporate and Investment Banking and Commercial

Banking and higher recoveries, partially offset by charge-offs related to

one large credit in the Private Bank.

Commercial – foreign loan net charge-offs increased $313 million

in 2002 compared to 2001, primarily due to charge-offs in emerging

markets including Argentina, as well as in telecommunications serv-

ices, media, and utilities industries in Western Europe.

Net charge-offs on consumer finance loans decreased $771 mil-

lion in 2002 compared to 2001, primarily due to $635 million in exit-

related charge-offs in the third quarter of 2001 as well as continued

runoff in the portfolio.

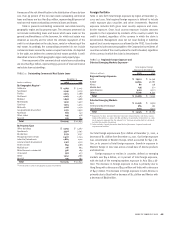

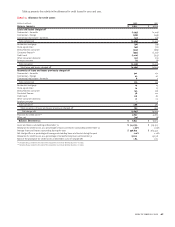

Table 14 presents the additions to and reductions in nonperforming assets in the commercial and consumer portfolios during 2002 and 2001.

TABLE 14 Nonperforming Assets Activity

(Dollars in millions)

2002 2001

Balance, January 1 $ 4,908 $ 5,457

Commercial

Additions to nonperforming assets:

New nonaccrual loans and foreclosed properties 4,963 4,797

Advances on loans 244 197

Total commercial additions 5,207 4,994

Reductions in nonperforming assets:

Paydowns, payoffs and sales (2,171) (2,065)

Returns to performing status (149) (313)

Charge-offs(1) (2,354) (2,289)

Total commercial reductions (4,674) (4,667)

Total commercial net additions to nonperforming assets 533 327

Consumer

Additions to nonperforming assets:

New nonaccrual loans and foreclosed properties 1,694 2,723

Total consumer additions 1,694 2,723

Reductions in nonperforming assets:

Paydowns, payoffs and sales (957) (881)

Returns to performing status (886) (1,360)

Charge-offs(1) (107) (261)

Transfers (to) from assets held for sale(2,3) 77 (1,097)

Total consumer reductions (1,873) (3,599)

Total consumer net reductions in nonperforming assets (179) (876)

Total net additions to (reductions in) nonperforming assets 354 (549)

Balance, December 31 $ 5,262 $ 4,908

(1) Certain loan products, including commercial credit card, consumer credit card and consumer non-real estate loans, are not classified as nonperforming; therefore, the charge-offs on

these loans are not included above.

(2) Includes assets held for sale that were foreclosed and transferred to foreclosed properties.

(3) Transfers in 2001 were primarily related to the exit of the subprime real estate lending business.

Commercial – domestic loans past due 90 days or more and still accruing