Bank of America 2002 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

42 BANK OF AMERICA 2002

Banc of America Strategic Solutions, Inc. (SSI) is a wholly-owned

subsidiary of the Corporation which manages problem asset resolu-

tion and the coordination of exit strategies, if applicable, including

bulk sales, collateralized debt obligations and other resolutions of

domestic and international commercial distressed assets. For addi-

tional discussion, see “Problem Loan Management” on page 48.

Consumer Portfolio Credit Risk Management

Credit risk management for consumer credit occurs throughout a bor-

rower’s credit cycle. Statistical techniques are used to establish product

pricing, risk appetite, operating processes and metrics to balance risks

and rewards appropriately. Consumer exposure is grouped by product

and other attributes for purposes of evaluating credit risk. Statistical

models are built using detailed behavioral and demographic informa-

tion from external sources such as credit bureaus as well as extensive

internal historical experience. These models form the foundation of our

consumer credit risk management process and are used extensively to

determine approve/decline credit decisions, collections management,

portfolio management, adequacy of the allowance for credit losses

and economic capital allocation for credit risk.

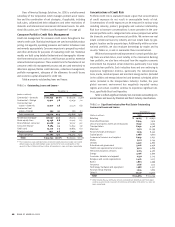

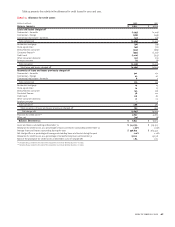

Table 9 presents outstanding loans and leases.

TABLE 9 Outstanding Loans and Leases(1)

December 31

(Dollars in millions)

2002 2001

Commercial – domestic $ 105,053 30.6% $ 118,205 35.9%

Commercial – foreign 19,912 5.8 23,039 7.0

Commercial real

estate – domestic 19,910 5.8 22,271 6.8

Commercial real

estate – foreign 295 0.1 383 0.1

Total commercial 145,170 42.3 163,898 49.8

Residential mortgage 108,197 31.6 78,203 23.8

Home equity lines 23,236 6.8 22,107 6.7

Direct/Indirect consumer 31,068 9.1 30,317 9.2

Consumer finance 8,384 2.4 12,652 3.9

Credit card 24,729 7.2 19,884 6.0

Foreign consumer 1,971 0.6 2,092 0.6

Total consumer 197,585 57.7 165,255 50.2

Total $ 342,755 100.0% $329,153 100.0%

(1) The Corporation used credit derivatives to provide credit protection (single name credit

default swaps, basket credit default swaps and CLOs) for loan counterparties in the

amounts of $16.7 billion and $14.5 billion at December 31, 2002 and 2001, respectively.

Concentrations of Credit Risk

Portfolio credit risk is evaluated toward a goal that concentrations

of credit exposure do not result in unacceptable levels of risk.

Concentrations of credit exposure can be measured in various ways

including industry, product, geography and customer relationship.

Risk due to borrower concentrations is more prevalent in the com-

mercial portfolio and is categorized into various perspectives within

the domestic and foreign commercial portfolio. We review non-real

estate commercial loans by industry and real estate loans by geo-

graphic location and by property type. Additionally, within our inter-

national portfolio, we also evaluate borrowings by region and by

country. Tables 10, 11 and 12 summarize these concentrations.

While we have experienced improvement in certain portfolios dur-

ing these uncertain times, most notably in the Commercial Banking

loan portfolio, we also have witnessed how the negative economic

environment has impacted certain industries, particularly in our large

corporate loan portfolio. Such industries have and are continuing to

experience heightened distress, particularly the telecommunica-

tions, media, merchant power

and merchant energy sectors (included

in the utilities and energy industries)

and domestic scheduled airline

sector (included in the transportation industry). Further, the poor

global economic environment has negatively impacted various

regions and certain countries continue to experience significant dis-

tress, specifically Brazil and Argentina.

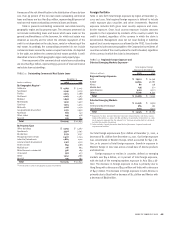

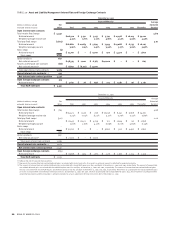

Table 10 reflects significant industry non-real estate outstanding com-

mercial loans and leases by Standard and Poor’s industry classifications.

TABLE 10 Significant Industry Non-Real Estate Outstanding

Commercial Loans and Leases

December 31

(Dollars in millions)

2002 2001

Retailing $ 10,165 $ 10,651

Diversified financials 8,344 7,916

Leisure and sports, hotels and restaurants 8,139 9,193

Transportation 8,030 9,508

Materials 7,972 10,399

Food, beverage and tobacco 7,335 8,543

Capital goods 7,088 9,691

Commercial services and supplies 6,449 7,637

Media 5,911 5,244

Utilities 5,590 4,860

Education and government 5,206 4,936

Health care equipment and services 3,912 4,809

Telecommunications services 3,105 4,560

Energy 3,076 3,800

Consumer durables and apparel 2,591 3,725

Religious and social organizations 2,426 2,213

Banks 1,881 2,999

Insurance 1,616 2,113

Technology hardware and equipment 1,368 2,527

Food and drug retailing 1,344 1,603

Other(1) 23,417 24,317

Total $ 124,965 $ 141,244

(1) Other includes $5,134 and $6,032 of loans outstanding to Individuals and Trusts repre-

senting 1.5 percent and 1.8 percent of total loans outstanding at December 31, 2002 and

2001, respectively.