Bank of America 2002 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 79BANK OF AMERICA 2002 79BANK OF AMERICA 2002 79

The Corporation formally documents at inception all relation-

ships between hedging instruments and hedged items, as well as its

risk management objectives and strategies for undertaking various

hedge transactions as required by SFAS 133. Additionally, the

Corporation uses regression analysis at the hedge’s inception and

quarterly thereafter to assess whether the derivative used in its hedg-

ing transaction is expected to be or has been highly effective in offset-

ting changes in the fair value or cash flows of the hedged items. The

Corporation discontinues hedge accounting when it is determined that

a derivative is not expected to be or has ceased to be highly effective as

a hedge, and then reflects changes in fair value in earnings.

The Corporation uses its derivatives designated for hedging

activities as either fair value hedges, cash flow hedges or hedges of net

investments in foreign operations. The Corporation primarily man-

ages interest rate and foreign currency exchange rate sensitivity

through the use of derivatives. Fair value hedges are used to limit the

Corporation’s exposure to changes in the fair value of its fixed interest-

bearing assets or liabilities that are due to interest rate volatility. Cash

flow hedges are used to minimize the variability in cash flows of inter-

est-bearing assets or liabilities or anticipated transactions caused by

interest rate fluctuations. Changes in the fair value of derivatives des-

ignated for hedging activities that are highly effective as hedges are

recorded in earnings or other comprehensive income, depending on

whether the hedging relationship satisfies the criteria for a fair value

or cash flow hedge, respectively. A highly effective hedging relationship

is one in which the Corporation achieves offsetting changes in fair value

or cash flows between 80 percent and 120 percent for the risk being

hedged. Hedge ineffectiveness and gains and losses on the excluded

component of a derivative in assessing hedge effectiveness are

recorded in earnings. SFAS 133 retains certain concepts under

Statement of Financial Accounting Standards No. 52, “Foreign

Currency Translation,” (SFAS 52) for foreign currency exchange hedg-

ing. Consistent with SFAS 52, the Corporation records changes in the

fair value of derivatives used as hedges of the net investment in

foreign operations as a component of other comprehensive income.

The Corporation from time-to-time purchases or issues financial

instruments containing embedded derivatives. The embedded deriva-

tive is separated from the host contract and carried at fair value if the

economic characteristics of the derivative are not clearly and closely

related to the economic characteristics of the host contract. To the

extent that the Corporation cannot reliably identify and measure the

embedded derivative, the entire contract is carried at fair value on

the balance sheet with changes in fair value reflected in earnings.

If a derivative instrument in a fair value hedge is terminated or

the hedge designation removed, the difference between a hedged

item’s then carrying amount and its face amount is recognized into

income over the original hedge period. Similarly, if a derivative

instrument in a cash flow hedge is terminated or the hedge designa-

tion removed, related amounts accumulated in other comprehensive

income are reclassified into earnings in the same period during

which the hedged item affects income.

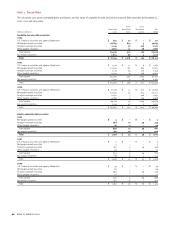

Securities

Debt securities are classified based on management’s intention on

the date of purchase and recorded on the balance sheet as of the

trade date. Debt securities which management has the intent and

ability to hold to maturity are classified as held-to-maturity and

reported at amortized cost. Securities that are bought and held princi-

pally for the purpose of resale in the near term are classified as trad-

ing instruments and are stated at fair value with unrealized gains and

losses included in trading account profits. All other debt securities

are classified as available-for-sale and carried at fair value with net

unrealized gains and losses included in shareholders’ equity on an

after-tax basis.

Interest and dividends on securities, including amortization of

premiums and accretion of discounts, are included in interest income.

Realized gains and losses from the sales of securities are determined

using the specific identification method.

Marketable equity securities, which are included in other assets,

are carried at fair value. Net unrealized gains and losses are included

in shareholders’ equity, net of tax; income is included in noninterest

income. Venture capital investments for which there are active market

quotes are carried at estimated fair value, subject to liquidity dis-

counts, sales restrictions or regulatory rules. Net unrealized gains

and losses are recorded in noninterest income. Venture capital invest-

ments for which there are not active market quotes are initially valued

at cost. Subsequently, these investments are adjusted to reflect

changes in valuation as a result of initial public offerings or other-

than-temporary declines in value.