Bank of America 2002 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116

|

|

During 2002, the Corporation reached a tax settlement agree-

ment with the Internal Revenue Service. This agreement resolved

issues for numerous tax returns of the Corporation and various prede-

cessor companies and finalized all federal income tax liabilities

through 1999. As a result of the settlement, a $488 million reduction in

income tax expense was recorded resulting from a reduction in pre-

viously accrued taxes.

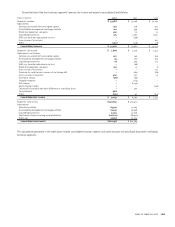

Significant components of the Corporation’s deferred tax (liabili-

ties) assets at December 31, 2002 and 2001 were as follows:

(Dollars in millions)

2002 2001

Deferred tax liabilities:

Equipment lease financing $ (5,817) $(6,907)

Investments (902) (559)

Securities valuation (531) (369)

Intangibles (457) (818)

State taxes (326) (457)

Available-for-sale securities (266) –

Depreciation (190) (166)

Employee retirement benefits (121) –

Deferred gains and losses (101) (92)

Employee benefits (69) (112)

Other (223) (104)

Gross deferred tax liabilities (9,003) (9,584)

Deferred tax assets:

Allowance for credit losses 2,742 2,991

Accrued expenses 428 482

Net operating loss carryforwards 347 143

Loan fees and expenses 91 93

Basis difference in subsidiary stock –418

Available-for-sale securities –311

Employee retirement benefits –56

Other 37 438

Gross deferred tax assets 3,645 4,932

Valuation allowance (114) (107)

Gross deferred tax assets,

net of valuation allowance 3,531 4,825

Net deferred tax liabilities $ (5,472) $(4,759)

The valuation allowance included in the Corporation’s deferred tax

assets at December 31, 2002 and 2001 represented net operating loss

carryforwards for which it is more likely than not that realization will

not occur and expire in 2004 to 2009. The net change in the valuation

allowance for deferred tax assets resulted from net operating losses

being generated by foreign subsidiaries in 2002 where realization is

not expected to occur.

At December 31, 2002 and 2001, federal income taxes had not

been provided on $899 million and $859 million, respectively, of

undistributed earnings of foreign subsidiaries, earned prior to 1987

and after 1997, that have been reinvested for an indefinite period of

time. If the earnings were distributed, an additional $198 million and

$188 million of tax expense, net of credits for foreign taxes paid on

such earnings and for the related foreign withholding taxes, would

result in 2002 and 2001, respectively.

NOTE 19 Fair Value of Financial Instruments

Statement of Financial Accounting Standards No. 107, “Disclosures

About Fair Value of Financial Instruments” (SFAS 107), requires the dis-

closure of the estimated fair value of financial instruments. The fair

value of a financial instrument is the amount at which the instrument

could be exchanged in a current transaction between willing parties,

other than in a forced or liquidation sale. Quoted market prices, if avail-

able, are utilized as estimates of the fair values of financial

instruments. Since no quoted market prices exist for certain of the

Corporation’s financial instruments, the fair values of such instru-

ments have been derived based on management’s assumptions, the

estimated amount and timing of future cash flows and estimated

discount rates. The estimation methods for individual classifications of

financial instruments are described more fully below. Different

assumptions could significantly affect these estimates. Accordingly, the

net realizable values could be materially different from the estimates

presented below. In addition, the estimates are only indicative of the

value of individual financial instruments and should not be considered

an indication of the fair value of the combined Corporation.

The provisions of SFAS 107 do not require the disclosure of the

fair value of lease financing arrangements and nonfinancial instru-

ments, including intangible assets such as goodwill, franchise, and

credit card and trust relationships.

Short-Term Financial Instruments

The carrying value of short-term financial instruments, including cash

and cash equivalents, time deposits placed, federal funds sold and

purchased, resale and repurchase agreements, commercial paper

and other short-term investments and borrowings, approximates the

fair value of these instruments. These financial instruments generally

expose the Corporation to limited credit risk and have no stated

maturities or have an average maturity of less than 30 days and carry

interest rates which approximate market.

Financial Instruments Traded in the Secondary Market

Held-to-maturity securities, available-for-sale securities, trading

account instruments, long-term debt and trust preferred securities

traded actively in the secondary market have been valued using

quoted market prices. The fair values of securities and trading

account instruments are reported in Notes 3 and 4.

Derivative Financial Instruments

All derivatives are recognized on the balance sheet at fair value,

taking into consideration the effects of legally enforceable master

netting agreements which allow the Corporation to settle positive

and negative positions with the same counterparty on a net basis. For

exchange traded contracts, fair value is based on quoted market

prices. For non-exchange traded contracts, fair value is based on

dealer quotes, pricing models or quoted prices for instruments with

similar characteristics. The fair value of the Corporation’s derivative

assets and liabilities is presented in Note 5.

106 BANK OF AMERICA 2002