Bank of America 2002 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

30 BANK OF AMERICA 2002

Principal Investing

Principal Investing within the Equity Investments segment, discussed

in more detail in Business Segment Operations, is comprised of a

diversified portfolio of investments in privately held and publicly

traded companies at all stages, from start-up to buyout. Some of

these companies may need access to additional cash to support

their long-term business models. Market conditions as well as com-

pany performance may impact whether such funding is sourced from

private investors or via capital markets. As of December 31, 2002,

we had non-public investments of $5.4 billion.

Trading Assets and Liabilities

The Corporation engages in a variety of trading-related activities that

are either for clients or our own accounts. The management process

related to the trading positions is discussed in detail in the Market

Risk Management section beginning on page 49. Positions recorded

on the balance sheet are valued at fair value and the majority of the

positions are based on or derived from actively quoted markets prices

or rates. Valuations for trading account assets and liabilities are

obtained from actively traded markets where valuations can be

obtained from quoted market prices or observed transactions. The

most significant factor affecting the valuation of trading assets or

liabilities is the lack of liquidity, where trading in a position or a mar-

ket sector has slowed significantly or ceased and quotes may not be

available. Liquidity situations generally are triggered by the market’s

perception of credit regarding a single company or a specific market

sector, for example airlines or sub-prime. In these instances, valua-

tions are derived from the limited market information available and

other factors, principally from reviewing the issuer’s financial state-

ments and changes in credit ratings made by one or more of the rating

agencies. Valuations for derivative assets and liabilities not traded

on an exchange, or over the counter, are obtained using

mathematical models that require inputs of external rates and prices

to generate continuous yield or pricing curves used to value the

position. This “pricing risk” is greater for positions with either option-

based or longer dated attributes where inputs are not readily available

and model-based extrapolations of rate and price scenarios are used

to generate valuations. In these situations, this risk is mitigated

through the use of valuation adjustments.

Accrued Taxes

Management estimates tax expense based on the amount it expects to

owe various tax authorities. Taxes are discussed in more detail in Note

18 of the consolidated financial statements. Accrued taxes represent

the net estimated amount due or to be received from taxing authori-

ties. In estimating accrued taxes, management assesses the relative

merits and risks of the appropriate tax treatment of transactions tak-

ing into account statutory, judicial and regulatory guidance in the

context of our tax position.

Goodwill

The nature and accounting for goodwill is discussed in detail in Notes 1

and 9 of the consolidated financial statements. Assigned goodwill is

subject to a market value recoverability test that records a loss if the

value of goodwill is less than the amount recorded in the financial

statements. Estimating the value of goodwill requires assumptions

regarding future cash flows and comparable business valuations.

Accounting Standards

Our accounting for hedging activities, securitizations and off-balance

sheet special purpose entities requires significant judgment in inter-

preting and applying the accounting principles related to these mat-

ters. Judgments include, but are not limited to, the determination of

whether a financial instrument or other contract meets the definition

of a derivative in accordance with Statement of Financial Accounting

Standards No. 133, “Accounting for Derivative Instruments and Hedging

Activities,” (SFAS 133) and the applicable hedge criteria, the accounting

for the transfer of financial assets and extinguishments of liabilities in

accordance with Statement of Financial Accounting Standards No. 140,

“Accounting for Transfers and Servicing of Financial Assets and

Extinguishments of Liabilities – a replacement of FASB Statement

No. 125” (SFAS 140) and the determination of when certain special

purpose entities should be consolidated in the Corporation’s balance

sheet and statement of income. For a more complete discussion of these

principles, see Notes 1, 5 and 8 of the consolidated financial statements.

The remainder of management’s discussion and analysis of the

Corporation’s results of operations and financial position should be

read in conjunction with the consolidated financial statements and

related notes presented on pages 72 through 111. See Note 1 for

Recently Issued Accounting Pronouncements.

Business Segment Operations

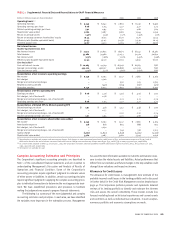

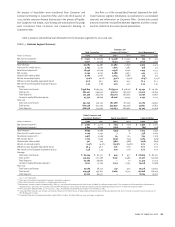

We provide to our clients both traditional banking and nonbanking

financial products and services through four business segments:

Consumer and Commercial Banking, Asset Management, Global

Corporate and Investment Banking and Equity Investments.

In managing our four business segments, we evaluate results

using both financial and non-financial measures. Financial measures

consist primarily of revenue, net income and shareholder value

added. Non-financial measures include, but are not limited to, market

share and customer satisfaction. Total revenue includes net interest

income on a taxable-equivalent basis and noninterest income. The

net interest income of the business segments includes the results of a

funds transfer pricing process that matches assets and liabilities

with similar interest rate sensitivity and maturity characteristics. Net

interest income also reflects an allocation of net interest income gen-

erated by certain assets and liabilities used in our asset and liability

management (ALM) activities.

From time to time we refine the business segment strategy and

reporting. As we continued to refine our business segment strategy in

2001, we moved a portion of our thirty-year mortgage portfolio from

the Consumer and Commercial Banking segment to Corporate Other.

The mortgages designated solely for ALM activities were moved to

Corporate Other to reflect the fact that management decisions regard-

ing this portion of the mortgage portfolio are driven by corporate ALM

considerations and not by the business segments’ management. In

the first quarter of 2002, certain commercial lending businesses in