Bank of America 2002 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 77BANK OF AMERICA 2002 77BANK OF AMERICA 2002 77

In determining the pro forma disclosures above, the fair value of

options granted was estimated on the date of grant using the Black-

Scholes option-pricing model and assumptions appropriate to each

plan. The Black-Scholes model was developed to estimate the fair value

of traded options, which have different characteristics than employee

stock options, and changes to the subjective assumptions used in the

model can result in materially different fair value estimates. The

weighted average grant date fair values of the options granted during

2002, 2001 and 2000 were based on the following assumptions:

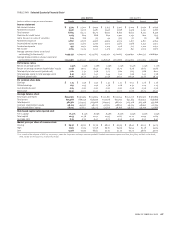

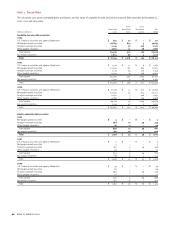

As Reported Pro Forma

(Dollars in millions, except per share data)

2002 2001 2000 2002 2001 2000

Net income $ 9,249 $ 6,792 $ 7,517 $ 8,836 $ 6,441 $ 7,215

Net income available to common shareholders 9,244 6,787 7,511 8,831 6,436 7,209

Earnings per common share 6.08 4.26 4.56 5.81 4.04 4.38

Diluted earnings per common share 5.91 4.18 4.52 5.64 3.96 4.34

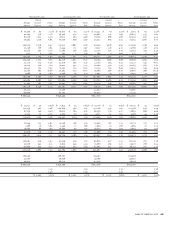

Risk-Free Interest Rates Dividend Yield

2002 2001 2000 2002 2001 2000

Key Employee Stock Plan 5.00% 5.05% 6.74% 4.76% 4.50% 4.62%

Broad-based plans 4.14 4.89 6.57 4.37 5.13 4.62

Expected Lives (Years) Volatility

2002 2001 2000 2002 2001 2000

Key Employee Stock Plan 77726.86% 26.68% 25.59%

Broad-based plans 44431.02 31.62 30.27

Compensation expense under the fair-value based method is

recognized over the vesting period of the related stock options.

Accordingly, the pro forma results of applying SFAS 123 in 2002,

2001 and 2000 may not be indicative of future amounts.

In November 2002, the Emerging Issues Task Force (EITF) finalized

the minutes to its discussion of EITF Issue 02-3, “Accounting for

Contracts Involved in Energy Trading and Risk Management Activities”

(EITF 02-3), which included clarification of the FASB staff’s view that an

entity should not recognize an unrealized gain or loss at inception of a

derivative instrument unless the fair value of that instrument is

obtained from a quoted market price in an active market or is other-

wise evidenced by comparison to other observable current market

transactions or based on a valuation technique incorporating observ-

able market data. This view is applicable to all derivative instruments

held for trading purposes entered into on or after November 21, 2002.

EITF 02-3 did not have a material impact on the Corporation’s results of

operations or financial condition.

FASB Interpretation No. 45, “Guarantor’s Accounting and

Disclosure Requirements for Guarantees,” (FIN 45) was issued in

November 2002. FIN 45 requires that a liability be recognized at the

inception of certain guarantees for the fair value of the obligation,

including the ongoing obligation to stand ready to perform over the

term of the guarantee. Guarantees, as defined in FIN 45, include

contracts that contingently require the Corporation to make payments

to a guaranteed party based on changes in an underlying that is

related to an asset, liability or equity security of the guaranteed party,

performance guarantees, indemnification agreements or indirect guar-

antees of indebtedness of others. This new accounting is effective for

certain guarantees issued or modified after December 31, 2002. In

addition, FIN 45 requires certain additional disclosures that are

located in Notes 8 and 13. Management does not expect that the adop-

tion of FIN 45 will have a material impact on the Corporation’s results

of operations or financial condition.

In June 2001, the FASB issued Statement of Financial Accounting

Standards No. 142, “Goodwill and Other Intangible Assets,” (SFAS 142).

SFAS 142 became effective for the Corporation on January 1, 2002 and

primarily addresses the accounting for goodwill and intangible assets

subsequent to their acquisition. SFAS 142 requires that goodwill be

recorded at the reporting unit level. The Corporation defines reporting

units as an operating segment or one level below. The Corporation has

evaluated the lives of intangible assets as required by SFAS 142 and no

change was made regarding lives upon adoption. SFAS 142 prohibits

the amortization of goodwill but requires that it be tested for impair-

ment at least annually at the reporting unit level. Goodwill was tested

for impairment and no impairment charges were recorded.

In accordance with SFAS 123, the Corporation provides dis-

closures as if the Corporation had adopted the fair value-based

method of measuring all outstanding employee stock options in

2002,

2001 and 2000 as indicated in the following table. The

disclosure

requirement of SFAS 123 recognizes the impact of all outstanding

employee stock options while the prospective method that the

Corporation intends to follow under SFAS 148 recognizes the impact of

only newly issued employee stock options.