Bank of America 2002 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 33

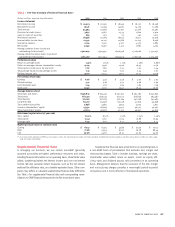

charges, partially offset by the impact of new and existing customers

choosing accounts with lower or no service charges drove the $128 mil-

lion, or five percent, increase in consumer service charges.

Increases in both debit and credit card income drove the eight

percent increase in card income. The increase in debit card income

within Banking Regions of $143 million, or 22 percent, was driven by

increases in purchase volumes. Higher annual, late, cash advance and

overlimit fees partially offset by the impact of reduced securitized

balances attributed to the $55 million, or three percent, increase in

credit card income within Consumer Products. Card income included

activity from the securitized portfolio of $168 million and $193 million

in 2002 and 2001, respectively. Noninterest income, rather than net

interest income, is recorded for assets that have been securitized as

we take on the role of servicer and record servicing income and

gains or losses on securitizations, where appropriate. New

advances under these previously securitized balances will be

recorded on our balance sheet after the revolving period of the secu-

ritization, which has the effect of increasing loans on our balance

sheet and increasing net interest income and charge-offs, with a cor-

responding reduction in noninterest income.

An increase in net mortgage production income driven by higher

mortgage sales, partially offset by declines in servicing volume due to

portfolio run-off were the main contributors to the $158 million, or

27 percent, increase in mortgage banking income within Consumer

Products. An increase in total production of first mortgage loans origi-

nated of $11.5 billion to $88.1 billion in 2002, is primarily attributed to

the current refinancing boom and the successful deployment of

LoanSolutions.

®

These factors more than offset our decision in the

second quarter of 2001 to exit the correspondent loan origination

channel in an effort to focus on the retail channel. We believe the

retail channel allows us to be more customer focused and deepen

our relationships with our customers as well as being more prof-

itable. First mortgage loan origination volume was composed of

approximately $60.0 billion of retail loans and $28.1 billion of whole-

sale loans in 2002. Retail first mortgage origination volume was 68 per-

cent of total volume in 2002 compared to 61 percent in 2001. An

increase in mortgage prepayments resulting from the significant

decrease in mortgage interest rates during 2002 drove the $28.4 bil-

lion decline in the average portfolio of first mortgage loans serviced to

$283.0 billion in 2002. Total consumer real estate originations

surpassed $100 billion in 2002. Mortgage banking assets declined

$1.8 billion or 46 percent from a year ago also due to higher prepay-

ments in the lower interest rate environment.

Higher provision in the credit card loan portfolio, partially offset

by a decline in provision within Commercial Banking resulted in a

$223 million, or 14 percent, increase in the provision for credit losses.

The increase in credit card provision was primarily attributable to the

increase in average on-balance sheet outstandings, portfolio seasoning

of outstandings from new account growth in 2000 and 2001 and a

weaker economic environment. Seasoning refers to the length of time

passed since an account was opened. The reduction in the Commercial

Banking provision was driven by the reduction in average commercial

loans and leases and improved credit quality during 2002.

Noninterest expense increased slightly, primarily attributable to

increases in processing/support costs (which included increases

related to e-commerce and debit card processing), marketing and

promotional fees, data processing expense and personnel expense as

well as the change in assumptions for the Bank of America Pension

Plan. The increase in marketing and promotional fees for the segment

was primarily due to increased advertising and marketing invest-

ments in mortgage, online banking and bill pay and card products.

The increase in data processing expense was primarily due to costs

associated with terminated contracts on discontinued software

licenses and due to an increase in online bill payers. An increase in

employee benefits expense for the segment and an increase in incen-

tive compensation due to higher mortgage production drove the

increase in personnel expense. See Note 16 of the consolidated finan-

cial statements for additional discussion of the change in assumption

for the Bank of America Pension Plan. These increases were partially

offset by the elimination of goodwill amortization. Goodwill amorti-

zation expense in 2001 was $452 million.

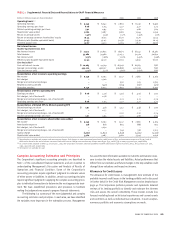

Asset Management

Asset Management includes the Private Bank, Banc of America

Investments and Banc of America Capital Management. The Private

Bank’s goal is to assist individuals and families in building and pre-

serving their wealth by providing investment, fiduciary, comprehensive

credit and banking expertise to high-net-worth clients. Banc of America

Investments provides investment, securities and financial planning

services and includes both the full-service network of investment advi-

sors and an extensive on-line investor service. Banc of America Capital

Management is an asset management organization serving the needs of

institutional clients, high-net-worth individuals and retail customers.

Banc of America Capital Management manages money and distribution

channels, provides investment solutions, offers institutional separate

accounts and wrap programs and provides advice to clients through

asset allocation expertise and software.

Despite the 23 percent drop in the S&P 500 Index from a year

ago, total revenue only declined $76 million, or three percent, in 2002.

Net income decreased $118 million, or 23 percent. The decrease in net

income drove the 64 percent decline in shareholder value added.

During 2002, Asset Management grew its distribution capabilities

to better serve the financial needs of its clients across the franchise,

surpassing its goal of increasing the number of advisors by more than

20 percent. In addition, we continue to enhance the financial planning

tools used to assist clients with their financial goals, and these financial

planning tools have received industry recognition in the market place.

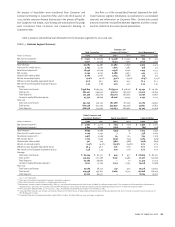

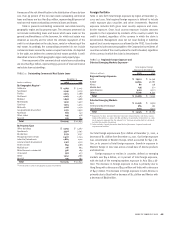

Client Assets

December 31

(Dollars in billions)

2002 2001

Assets under management $ 310.3 $ 314.2

Client brokerage assets 90.9 99.4

Assets in custody 46.6 46.9

Total client assets $ 447.8 $ 460.5