Bank of America 2002 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

40 BANK OF AMERICA 2002

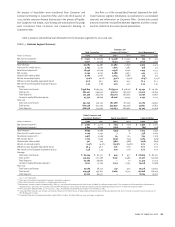

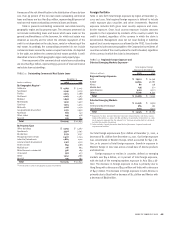

We manage our credit risk on these commitments by subjecting

them to our normal underwriting and risk management processes. At

December 31, 2002 and 2001, the Corporation had off-balance sheet

liquidity commitments and SBLCs to these financing entities of

$34.2 billion and $36.1 billion, respectively. Substantially all of these

liquidity commitments and SBLCs mature within one year. These

amounts are included in Table 8. Net revenues earned from fees

associated with these financing entities were approximately $484 mil-

lion and $256 million for 2002 and 2001, respectively.

We generally do not purchase any commercial paper issued by

these financing entities other than during the underwriting process

when we act as issuing agent nor do we purchase any of the commer-

cial paper for our own account. We do not consolidate these types of

entities based on the accounting guidance contained in ARB No. 51,

“Consolidated Financial Statements”, SFAS No. 94, “Consolidation of

All Majority-Owned Subsidiaries”, EITF Issue No. D-14, “Transactions

Involving Special Purpose Entities”, and EITF Issue No. 90-15,

“Impact of Nonsubstantive Lessors, Residual Value Guarantees, and

Other Provisions in Leasing Transactions”. Derivative instruments

related to these entities are marked to market through the statement

of income. SBLCs and liquidity commitments are accounted for pur-

suant to SFAS No. 5, “Accounting for Contingencies”(SFAS 5), and are

discussed further in Note 13 to the consolidated financial statements.

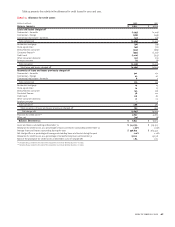

In January 2003, the FASB issued a new rule that addresses off-

balance sheet financing entities. As a result, we expect that we will

have to consolidate our multi-seller asset backed conduits beginning in

the third quarter of 2003, as required by the rule. As of December 31,

2002, the assets of these entities were approximately $25.0 billion. The

actual amount that will be consolidated is dependent on actions taken

by the Corporation and our customers between December 31, 2002

and the third quarter of 2003. Management is assessing alternatives

with regards to these entities including restructuring the entities

and/or alternative sources of cost-efficient funding for our customers

and expects that the amount of assets consolidated will be less than

the $25.0 billion due to these actions and those of our customers.

Revenues from administration, liquidity, letters of credit and other

services provided to these entities were approximately $121 million in

2002 and $125 million in 2001. The new rule requires that for entities

to be consolidated that those assets be initially recorded at their car-

rying amounts at the date the requirements of the new rule first apply.

If determining carrying amounts as required is impractical, then the

assets are to be measured at fair value the first date the new rule

applies. Any difference between the net amount added to the

Corporation’s balance sheet and the amount of any previously recog-

nized interest in the newly consolidated entity shall be recognized as the

cumulative effect of an accounting change. Had we adopted the rule in

2002, there would have been no material impact to net income. See

Note 1 of the consolidated financial statements for a discussion regard-

ing management’s estimated impact of the new rule in 2003.

In addition, to control our capital position, diversify funding

sources and provide customers with commercial paper investments,

from time to time we will sell assets to off-balance sheet commercial

paper entities. The commercial paper entities are special purpose

entities that have been isolated beyond our reach or that of our

creditors, even in the event of bankruptcy or other receivership.

Assets sold to the entities consist primarily of high-grade corporate or

municipal bonds, collateralized debt obligations and asset-backed

securities. These entities issue collateralized commercial paper to

third party market participants and passive derivative instruments to

us. Assets sold to the entities typically have an investment rating rang-

ing from Aaa/AAA to Aa/AA. We may provide liquidity, SBLCs or similar

loss protection commitments to the entity, or we may enter into a

derivative with the entity in which we assume certain risks. The liq-

uidity facility and derivative have the same legal standing with the

commercial paper.

The derivative provides interest rate, currency and a pre-spec-

ified amount of credit protection to the entity in exchange for the

commercial paper rate. This derivative is provided for in the legal

documents and helps to alleviate any cash flow mismatches. In some

cases, if an asset’s rating declines below a certain investment quality

as evidenced by its investment rating or defaults, we are no longer

exposed to the risk of loss. At that time, the commercial paper holders

assume the risk of loss. In other cases, we agree to assume all of the

credit exposure related to the referenced asset. Legal documents for

each entity specify asset quality levels that require the entity to auto-

matically dispose of the asset once the asset falls below the speci-

fied quality rating. At the time the asset is disposed, we are required

to reimburse the entity for any credit-related losses depending on the

pre-specified level of protection provided.

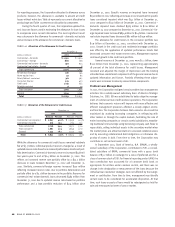

We also receive fees for the services we provide to the entities,

and we manage any credit or market risk on commitments or deriva-

tives through normal underwriting and risk management processes.

Derivative activity related to these entities is included in Note 5 of the

consolidated financial statements. At December 31, 2002 and 2001, the

Corporation had off-balance sheet liquidity commitments, SBLCs and

other financial guarantees to the financing entities of $4.5 billion and

$4.3 billion, respectively. Substantially all of these liquidity commit-

ments, SBLCs and other financial guarantees mature within one year.

These amounts are included in Table 8. Net revenues earned from fees

associated with these entities were $37 million and $49 million in

2002 and 2001, respectively.

We generally do not purchase any of the commercial paper

issued by these types of financing entities other than during the

underwriting process when we act as issuing agent nor do we pur-

chase any of the commercial paper for our own account. We do not

consolidate these types of entities because they are considered

Qualified Special Purpose Entities as defined in SFAS No. 140,

“Accounting for Transfers and Servicing of Financial Assets and

Extinguishments of Liabilities”. Derivative instruments related to

these entities are marked to market through the statement of

income. SBLCs and liquidity commitments are accounted for pur-

suant to SFAS 5 and are discussed further in Note 13 to the con-

solidated financial statements.