Bank of America 2002 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

36 BANK OF AMERICA 2002

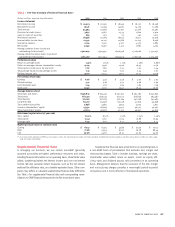

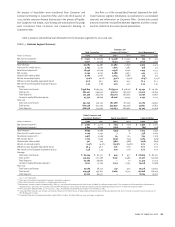

Net interest income consists primarily of the internal funding

cost associated with the carrying value of investments.

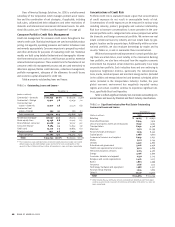

Equity Investment Gains in Principal Investing

(Dollars in millions)

2002 2001

Cash gains $432 $ 425

Impairments (708) (335)

Fair value adjustments (10) (40)

Total $ (286) $50

Noninterest income primarily consists of equity investment gains

(losses). Weakness in equity markets in 2002 and a $140 million gain

in the strategic investments portfolio in the first quarter of 2001

related to the sale of an interest in the Star Systems ATM network

were the primary drivers for the decline in equity investment gains

(losses). Impairments recorded in both 2002 and 2001 were driven by

continuing depressed levels of economic activity across many sectors

and a lack of liquidity in the private or public equity markets which

were compounded in 2001 by the terrorist attack on September 11.

The Corporation recognized a reduction in values of certain equity

positions primarily within the technology, media and telecom portfo-

lios as well as value adjustments across many other industries both

domestically and internationally.

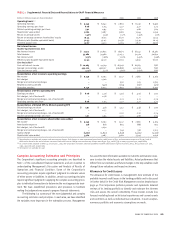

Risk Management

Overview

Our corporate governance structure enables us to manage all major

aspects of our business through an integrated planning and review

process that includes strategic, financial, associate and risk planning.

We derive our revenue from assuming and managing customer risk

for profit. Through a robust governance structure, risk and return is

evaluated to produce sustainable revenue, to reduce earnings volatil-

ity and increase shareholder value. Our business exposes us to four

major risks: liquidity, credit, market and operational.

Liquidity risk is the inability to accommodate liability maturities

and withdrawals, fund asset growth and otherwise meet contractual

obligations at reasonable market rates. Credit risk is the inability of a

customer to meet its repayment or delivery obligations. Market risk is

the fluctuation in asset values caused by changes in market prices

and yields. Operational risk is the potential for loss resulting from

events involving people, processes, technology, legal issues, external

events, execution, regulatory or reputation.

Board Committees

Our governance structure begins with our Board of Directors. The

Board of Directors evaluates risk through the Chief Executive Officer

(CEO) and three Board committees:

•Finance Committee reviews market, credit, liquidity and

operational risk

•Asset Quality Committee reviews credit risk

•Audit Committee reviews scope and coverage of external

and corporate audit activities

Three Lines of Defense

Management has established control processes and procedures to

align risk-taking and risk management throughout our organization.

These control processes and procedures are designed around “three

lines of defense”: lines of business; Risk Management joined by other

units such as Finance and Legal; and Corporate Audit.

The lines of business are responsible for identifying, quantifying,

mitigating and managing all risks. Except for trading-related business

activities within Global Corporate Investment Banking, interest rate risk

associated with our business activities is managed centrally in the

Corporate Treasury function. Line of business management makes

and executes the business plan, which puts it closest to the changing

nature of risks and therefore best able to take actions to manage and

mitigate those risks. Our management processes, structures and

policies help us comply with laws and regulations and provide clear

lines of sight for decision-making and accountability. Wherever practi-

cal, we attempt to house decision-making authority as close to the

customer as possible.

The Risk Management organization translates approved busi-

ness plans into approved limits, approves requests for changes to

those limits, approves transactions as appropriate and works closely

with business units to establish and monitor risk parameters. Each of

the four business segments has a Risk Executive assigned to it who is

responsible for oversight for all risks of the line of business.

Corporate Audit provides an independent assessment of our

management systems and internal control systems. Corporate Audit

activities are designed to provide reasonable assurance that

resources are adequately protected; significant financial, managerial

and operating information is complete, accurate, and reliable; and

employees’ actions are in compliance with Corporate policies, stan-

dards, procedures, and applicable laws and regulations.

Senior Management Committees

To ensure our risk management goals and objectives are accomplished,

oversight of our risk-taking and risk management activities is conducted

through three senior management committees.

The Risk and Capital Committee (RCC) establishes long-term strat-

egy and short-term operating plans. RCC also establishes the risk

appetite through corporate performance measures, capital allocations,

aggregate risk levels, and overall capital planning. RCC reviews actual

performance to plan and actual risk incurred to forecasted risk levels,

including information regarding credit, market and operational risk.

The Asset and Liability Committee (ALCO), a subcommittee of the

Finance Committee, reviews portfolio hedging used for managing liq-

uidity, market and credit portfolio risks as well as interest rate risk

inherent in our balance sheet and trading risk inherent in our customer

and proprietary trading portfolio. ALCO approves Value at Risk (VAR)

limits for various trading activities in the Corporation.

The Credit Risk Committee (CRC) establishes corporate credit

practices and limits, including industry and country concentration lim-

its, approval requirements and exceptions. CRC also reviews business

asset quality results versus plan, portfolio management, hedging

results and the adequacy of the allowance for credit losses.