Bank of America 2002 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

32 BANK OF AMERICA 2002

Consumer and Commercial Banking

Consumer and Commercial Banking provides a wide range of products

and services to individuals, small businesses and middle market com-

panies through multiple delivery channels.

The major components of Consumer and Commercial Banking

are Banking Regions, Consumer Products and Commercial Banking.

Banking Regions serves consumer households and small busi-

nesses in 21 states and the District of Columbia through its network of

4,208 banking centers, 13,013 ATMs, telephone, and Internet channels

on www.bankofamerica.com. Banking Regions provides a wide range

of products and services, including deposit products such as check-

ing, money market savings accounts, time deposits and IRAs, debit

card products and credit products such as home equity, mortgage and

personal auto loans. It also provides treasury management, credit

services, community investment, check card, e-commerce and broker-

age services to nearly two million small business relationships across

the franchise. Banking Regions also includes Premier Banking, which

provides high-touch banking and investment solutions to affluent

clients with balances up to $3 million.

Consumer Products provides specialized services such as the

origination, fulfillment and servicing of residential mortgage loans,

issuance and servicing of credit cards, direct banking via telephone

and Internet, student lending and certain insurance services.

Consumer Products also provides retail finance and floorplan pro-

grams to marine, RV and auto dealerships.

Commercial Banking provides commercial lending and treasury

management services primarily to middle market companies with

annual revenue between $10 million and $500 million. These services

are available through relationship manager teams as well as through

alternative channels such as the telephone via the commercial service

center and the Internet by accessing Bank of America Direct.

Commercial Banking also includes the Real Estate Banking Group,

which provides project financing and treasury management to private

developers, homebuilders and commercial real estate firms across the

U.S. Commercial Banking also provides lending and investing services

to develop low- and moderate-income communities.

Consumer and Commercial Banking drove our financial results in

2002 as total revenue increased $1.9 billion, or nine percent. Net

income rose $1.1 billion, or 23 percent. The increase in net income and

lower economic capital, as a result of reductions in commercial loan

levels in specific industries, drove the 23 percent increase in share-

holder value added.

Throughout the year our Consumer and Commercial Banking

strategy has been to attract, retain and deepen customer relation-

ships. A critical component of that strategy includes improvement of

customer satisfaction. Customers reporting that they were delighted

with their service increased 10.4 percent during the year. As a result

of this improvement, we added 528,000 net new checking accounts

for the year, which exceeded our goal, compared to 193,000 for

2001. Access to our services through on-line banking which saw a

63 percent increase in customers, our network of domestic banking

centers, ATMs, telephone and internet channels, and our product

innovations such as an expedited mortgage application process

through LoanSolutions

®

were factors contributing to revenue growth

and success with our customers.

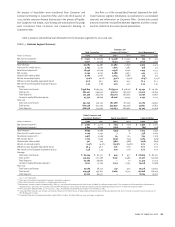

A favorable shift in loan mix from commercial to credit card and

residential mortgage, overall loan and deposit growth and the results

of ALM activities contributed to the $1.3 billion, or ten percent,

increase in net interest income. These increases were partially offset

by the compression of deposit interest margins.

Net interest income was positively impacted by the $5.2 billion,

or three percent, increase in average loans and leases compared to

2001. Average on-balance sheet credit card outstandings increased

29 percent, primarily due to balance transfers, the reduction in volun-

tary attrition and an increase in new advances on previously securi-

tized balances that are recorded on the Corporation’s balance sheet

after the revolving period of the securitization. Average residential

mortgage loans increased 38 percent primarily driven by the refinanc-

ing environment that began in the fourth quarter of 2001. Offsetting

these increases was a decline in average commercial loans of 12 per-

cent driven by liquidations, lower hold levels, reduced utilization of

existing facilities and soft loan demand.

Deposit growth also positively impacted net interest income.

Higher consumer deposit balances due to significant growth in net

checking accounts, increased money market accounts due to an

emphasis on total relationship balances and customer preference for

stable investments in these uncertain economic times drove

the

$17.2 billion, or seven percent, increase in average deposits to

$283.3 billion in 2002.

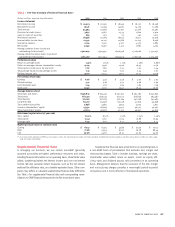

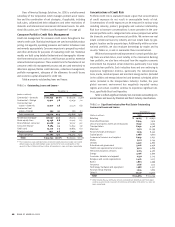

Significant Noninterest Income Components

(Dollars in millions)

2002 2001

Service charges $ 4,070 $ 3,779

Card income 2,620 2,422

Mortgage banking income 751 593

Increases in service charges, card income and mortgage banking

income drove the $636 million, or eight percent, increase in nonin-

terest income. These increases were partially offset by a decrease in

trading account profits within Consumer Products. In 2002, a

trad-

ing loss of $24 million was recorded compared to a trading gain of

$165 million in the prior year. The amount recorded in trading account

profits represents the net mark-to-market adjustments on

certain

mortgage banking assets and the related derivative instruments. See

Note 1 of the consolidated financial statements for additional infor-

mation on mortgage banking assets.

Both corporate and consumer service charges attributed to the

$291 million, or eight percent, increase in service charges. Corporate

service charges increased $163 million, or 17 percent, as customers

opted to pay service charges rather than maintain additional deposit

balances in the lower rate environment. Increased customer account