Bank of America 2002 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

92 BANK OF AMERICA 2002

Amortization expense on core deposit intangibles and other intangibles

was $218 million, $216 million and $229 million in 2002, 2001 and 2000,

respectively. The Corporation estimates that aggregate amortization

expense will be $212 million for 2003, $209 million for 2004, $208 mil-

lion for 2005, $207 million for 2006 and $118 million for 2007.

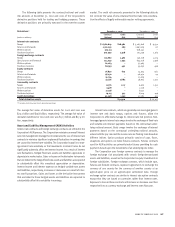

The gross carrying value and accumulated amortization related to core deposit intangibles and other intangibles at December 31, 2002 and

2001 are presented below:

December 31, 2002 December 31, 2001

Gross Carrying Accumulated Gross Carrying Accumulated

(Dollars in millions)

Value Amortization Value Amortization

Core deposit intangibles $ 1,495 $ 726 $ 1,495 $ 566

Other intangibles 757 431 730 365

Total $ 2,252 $ 1,157 $ 2,225 $ 931

Variable Interest Entities

In January 2003, the FASB issued a new rule that addresses off-

balance sheet financing entities. As a result, the Corporation expects

that it will have to consolidate its multi-seller asset backed conduits

beginning in the third quarter of 2003, as required by the rule. As of

December 31, 2002, the assets of these entities were approximately

$25.0 billion. The actual amount that will be consolidated is depend-

ent on actions taken by the Corporation and its customers between

December 31, 2002 and the third quarter of 2003. Management is

assessing alternatives with regards to these entities including restruc-

turing the entities and/or alternative sources of cost-efficient funding

for the Corporation’s customers and expects that the amount of assets

consolidated will be less than the $25.0 billion due to these actions

and those of its customers. Revenues from administration, liquidity,

letters of credit and other services provided to these entities were

approximately $121 million in 2002 and $125 million in 2001. The new

rule requires that for entities to be consolidated that those assets be

initially recorded at their carrying amounts at the date the require-

ments of the new rule first apply. If determining carrying amounts as

required is impractical, then the assets are to be measured at fair

value the first date the new rule applies. Any difference between the

net amount added to the Corporation’s balance sheet and the amount

of any previously recognized interest in the newly consolidated entity

shall be recognized as the cumulative effect of an accounting change.

Had the Corporation adopted the rule in 2002, there would have been

no material impact to net income. See Note 1 of the consolidated finan-

cial statements for a discussion regarding management’s estimated

impact of the new rule in 2003. At December 31, 2002, the

Corporation’s liquidity and letter of credit exposure associated with

the multi-seller conduits administered by the Corporation was approx-

imately $21.3 billion. Management does not believe losses resulting

from its administration of these conduits will be material.

Additionally, the Corporation has significant involvement with

other VIEs that it will not likely consolidate because it is not consid-

ered the primary beneficiary. In all cases, the Corporation does not

absorb the majority of the entities’ losses nor does it receive a major-

ity of the entities’ expected residual returns, or both. These entities

facilitate client transactions, and the Corporation functions as

administrator for all of these and provides either liquidity and letters

of credit or derivatives to the VIE. Total assets of these entities at

December 31, 2002 were approximately $11.1 billion; revenues

associated with administration, liquidity, letters of credit and other

services were approximately $341 million in 2002. At December 31,

2002, the Corporation’s loss exposure associated with these VIEs was

approximately $5.1 billion. Management does not believe losses

resulting from its involvement with these entities will be material.

The Corporation consolidates certain SPEs under current account-

ing guidance when it believes that consolidation is appropriate. At

December 31, 2002, assets of consolidated SPEs were approximately

$2.9 billion.

See Note 1 for additional discussion of special purpose financ-

ing entities.

NOTE 9 Goodwill and Other Intangibles

In accordance with SFAS 142, no goodwill amortization was recorded in

2002. Goodwill amortization expense in 2001 was $662 million. Net

income in 2001 was $6.8 billion or $4.26 per share ($4.18 per share

diluted). Net income adjusted to exclude goodwill amortization expense

would have been $7.4 billion or $4.64 per share ($4.56 per share

diluted) in 2001. The impact of goodwill amortization on net income in

2001 was $616 million or $0.38 per share (basic and diluted). Goodwill

amortization expense in 2000 was $635 million. Net income in 2000 was

$7.5 billion or $4.56 per share ($4.52 per share diluted). Net income

adjusted to exclude goodwill amortization expense would have been

$8.1 billion or $4.93 per share ($4.88 per share diluted) in 2000. The

impact of goodwill amortization on net income in 2000 was $602 million

or $0.37 per share ($0.36 per share diluted).

At December 31, 2002 and 2001, goodwill was $7.7 billion in

Consumer and Commercial Banking, $2.0 billion in Global Corporate

and Investment Banking and $134 million in Equity Investments.

Goodwill in Asset Management at December 31, 2002 and 2001 was

$1.5 billion and $943 million, respectively, reflecting a $550 million

addition representing final contingent consideration in connection

with the acquisition of the remaining 50 percent of Marsico Capital

Management, LLC in 2001 for $1.1 billion. All conditions related to

this contingent consideration have been met.