Bank of America 2002 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

BANK OF AMERICA 2002 81

Credit card loans are charged off at 180 days past due or 60

days from notification of bankruptcy filing and are not classified as

nonperforming. Unsecured consumer loans and deficiencies in non

real estate secured loans are charged off at 120 days past due and

not

classified as nonperforming. Real estate secured consumer loans are

placed on nonaccrual and classified as nonperforming at 90 days past

due. The amount deemed uncollectible on real estate secured loans is

charged off at 180 days past due.

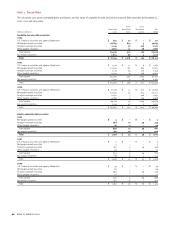

Loans Held for Sale

Loans held for sale include residential mortgage, loan syndications,

and to a lesser degree commercial real estate, consumer finance and

other loans, and are carried at the lower of aggregate cost or market

value. Loans held for sale are included in other assets.

Premises and Equipment

Premises and equipment are stated at cost less accumulated depreci-

ation and amortization. Depreciation and amortization are recognized

primarily using the straight-line method over the estimated useful

lives of the assets. Estimated lives range up to 40 years for buildings,

up to 12 years for furniture and equipment and the shorter of lease

term or estimated useful life for leasehold improvements.

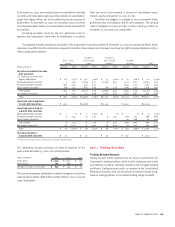

Mortgage Banking Assets

In the first quarter of 2001, the Corporation amended certain of its

Mortgage Selling and Servicing Contracts whereby its previously

reported mortgage servicing rights were bifurcated into a mortgage

servicing right (MSR) and Excess Spread Certificates (the Certificates).

The servicing component represents the contractually specified ser-

vicing fees net of the fair market value of the cost to service, and the

Certificates represent a retained financial interest in certain cash flows

of the underlying mortgage loans. The MSR and the Certificates are

classified as mortgage banking assets (MBAs). The Certificates are

carried at estimated fair value with the corresponding adjustment

reported in trading account profits. The Corporation seeks to manage

changes in value of the Certificates due to changes in prepayment

rates by entering into derivative financial instruments such as pur-

chased options and interest rate swaps. The derivative instruments

are carried at estimated fair value with the corresponding adjustment

reported in trading account profits. The Corporation values the

Certificates using an option-adjusted spread model which requires

several key components including, but not limited to, proprietary pre-

payment models and term structure modeling via Monte Carlo simu-

lation. The fair value of MBAs was $2.1 billion and $3.9 billion at

December 31, 2002 and 2001, respectively. Total loans serviced

approximated $264.5 billion, $320.8 billion and $335.9 billion at

December 31, 2002, 2001 and 2000 respectively, including loans

serviced on behalf of the Corporation’s banking subsidiaries.

The Corporation allocated the total cost of mortgage loans orig-

inated for sale or purchased between the cost of the loans, and when

applicable, the Certificates and the MSRs based on the relative fair

values of the loans, the Certificates and the MSR. MSR acquired

separately are capitalized at cost. The Corporation recorded $884 mil-

lion, $1.1 billion and $836 million of MBAs during 2002, 2001 and 2000,

respectively. The cost of MSR was amortized in proportion to and over

the estimated period that servicing revenues were recognized.

Amortization was $540 million during 2000.

Mortgage banking income includes certificate and servicing

fees, gains from selling originated mortgages, ancillary servicing

income, mortgage production fees and gains and losses on sales to

the secondary market.

Goodwill and Other Intangibles

Net assets of companies acquired in purchase transactions are

recorded at fair value at the date of acquisition, as such, the historical

cost basis of individual assets and liabilities are adjusted to reflect

their fair value. Identified intangibles are amortized on an accelerated

or straight-line basis over the period benefited. Goodwill is not amor-

tized but is reviewed for potential impairment on an annual basis at the

reporting unit level. The impairment test is performed in two

phases. The first step of the goodwill impairment test compares the

fair value of the reporting unit with its carrying amount, including

goodwill. If the fair value of the reporting unit exceeds its carrying

amount, goodwill of the reporting unit is considered not impaired;

however, if the carrying amount of the reporting unit exceeds its fair

value, an additional procedure must be performed. That additional pro-

cedure compares the implied fair value of the reporting unit’s goodwill

(as defined in SFAS 142) with the carrying amount of that goodwill. An

impairment loss is recorded to the extent that the carrying amount of

goodwill exceeds its implied fair value. In 2002, goodwill was tested for

impairment and no impairment charges were recorded.

Other intangible assets are evaluated for impairment if events

and circumstances indicate a possible impairment. Such evaluation of

other intangible assets is based on undiscounted cash flow pro-

jections. At December 31, 2002, intangible assets included in the

Consolidated Balance Sheet consist primarily of core deposit intangi-

bles that are amortized using an estimated range of anticipated lives

of 6 to 20 years.