Bank of America 2002 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

46 BANK OF AMERICA 2002

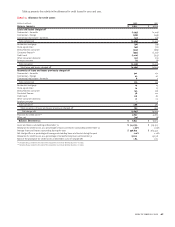

Credit card net charge-offs increased $422 million to $1.1 billion

in 2002 compared to 2001. The increase in net charge-offs was prima-

rily a result of portfolio seasoning of outstandings from new account

growth in 2000 and 2001, new advances on previously securitized bal-

ances, and a weaker economic environment. New advances under

these previously securitized balances are recorded on our balance

sheet after the revolving period of the securitization, which has the

effect of increasing loans on our balance sheet, increasing net inter-

est income and increasing charge-offs, with a corresponding reduc-

tion in noninterest income.

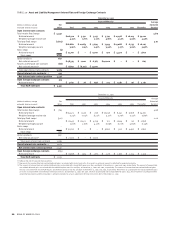

Allowance for Credit Losses

To help us identify credit risks and assess the overall collectibility of

our lending portfolios, we conduct periodic and systematic detailed

reviews. The allowance for credit losses represents management’s

estimate of probable losses in the portfolio.

Within the allowance, reserves are allocated to each product

type based on specific and formula components, as well as a general

reserve. See Note 1 of the consolidated financial statements for addi-

tional discussion on the Corporation’s allowance for credit losses.

The specific component of the allowance for credit losses covers

those commercial loans that are our nonperforming or impaired. An

allowance is established when the discounted cash flows (or col-

lateral value or observable market price) is lower than the carrying

value of that loan. For purposes of computing the specific loss com-

ponent of the allowance, larger impaired loans are evaluated indi-

vidually and smaller impaired loans are evaluated as a pool using

historical loss experience for the respective product type and risk

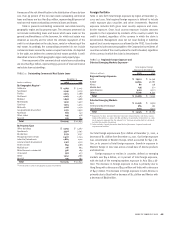

rating of the loan. In Table 17, this component of the allowance is

characterized as commercial impaired.

The formula component of the allocated allowance covers per-

forming commercial loans and leases, letters of credit and consumer

loans. The allowance for commercial loans and letters of credit is

established by credit type by analyzing historical loss experience,

by

internal risk rating, current economic conditions and performance

trends within each portfolio segment. The formula component

allowance for consumer loans is based on aggregated portfolio seg-

ment evaluations generally by credit product type. Loss forecast mod-

els are utilized for consumer products which consider a variety of

factors including, but not limited to, historical loss experience, esti-

mated defaults or foreclosures based on portfolio trends, delinquen-

cies and credit scores. These components of the allowance are

characterized as commercial non-impaired and total consumer,

respectively, in Table 17.

A general portion of allowance for credit losses is maintained to

cover uncertainties that affect our estimate of probable losses. These

uncertainties include the imprecision inherent in the forecasting

methodologies, certain industry and geographic concentrations

(including global economic uncertainty) and exposures related to

legally binding commitments that have not yet been drawn. Manage-

ment assesses each of these components to determine the overall

level of the general portion. The relationship of the general com-

ponent to the total allowance for credit losses may fluctuate from

period to period. Management evaluates the adequacy of the allowance

for credit losses based on the combined total of specific, formula and

general components.

The Corporation monitors differences between estimated and

actual incurred credit losses. This monitoring process includes

periodic assessments by senior management of credit portfolios and

the models used to estimate incurred losses in those portfolios.

Additions to the allowance for credit losses are made by charges

to the provision for credit losses. Credit exposures (excluding deriva-

tives) deemed to be uncollectible are charged against the allowance

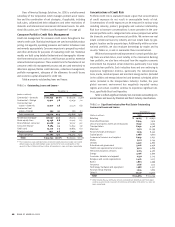

for credit losses. Table 15 presents a rollforward of the allowance for

credit losses. Recoveries of previously charged off amounts are cred-

ited to the allowance for credit losses. The provision for credit losses

was $3.7 billion and $4.3 billion for 2002 and 2001, respectively. The

allowance for credit losses was $6.9 billion at December 31, 2002

and 2001. The allowance for credit losses as a percentage of total

outstanding loans and leases was 2.00 percent at December 31, 2002

compared to 2.09 percent at December 31, 2001.