Bank of America 2002 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

76 BANK OF AMERICA 200276 BANK OF AMERICA 200276 BANK OF AMERICA 2002

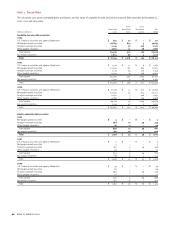

Bank of America Corporation and its subsidiaries (the Corporation)

through its banking and nonbanking subsidiaries, provide a diverse

range of financial services and products throughout the U.S. and in

selected international markets. At December 31, 2002, the Corporation

operated its banking activities primarily under two charters: Bank of

America, N.A. and Bank of America, N.A. (USA).

NOTE 1 Significant Accounting Principles

Principles of Consolidation and Basis of Presentation

The consolidated financial statements include the accounts of the

Corporation and its majority-owned subsidiaries. All significant inter-

company accounts and transactions have been eliminated. Results of

operations of companies purchased are included from the dates of

acquisition. Certain prior period amounts have been reclassified to

conform to current year classifications. Assets held in an agency or

fiduciary capacity are not included in the consolidated financial state-

ments. The Corporation accounts for investments in companies that it

owns a voting interest of 20 percent to 50 percent and for which it

may have significant influence over operating and financing decisions

using the equity method of accounting. These investments are

included in other assets and the Corporation’s proportionate share of

income or loss is included in equity investment gains.

The preparation of the consolidated financial statements in

conformity with accounting principles generally accepted in the

United States requires management to make estimates and assump-

tions that affect reported amounts and disclosures. Actual results

could differ from those estimates. Significant estimates made by

management are discussed in these notes as applicable and in

Complex Accounting Estimates and Principles beginning on page 29.

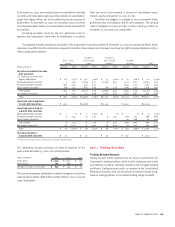

Recently Issued Accounting Pronouncements

In January 2003, the Financial Accounting Standards Board (FASB)

issued FASB Interpretation 46 “Consolidation of Variable Interest

Entities, an interpretation of ARB No. 51” (FIN 46). FIN 46 provides a new

framework for identifying variable interest entities (VIEs) and deter-

mining when a company should include the assets, liabilities, noncon-

trolling interests and results of activities of a VIE in its consolidated

financial statements. FIN 46 is effective immediately for VIEs created

after January 31, 2003 and is effective beginning in the third quarter of

2003 for VIEs created prior to issuance of the interpretation.

As a result, Management expects that the Corporation will have

to consolidate its multi-seller asset backed conduits. As of December

31, 2002, the assets of these entities were approximately $25.0 billion.

The actual amount that will be consolidated is dependent on actions

taken by the Corporation and its customers between December 31,

2002 and the third quarter of 2003. Management is assessing alterna-

tives with regards to these entities including restructuring the entities

and/or alternative sources of cost-efficient funding for our customers

and expects that the amount of assets consolidated will be less than

the $25.0 billion due to these actions and those of our customers. The

new rule requires that for entities to be consolidated that those assets

be initially recorded at their carrying amounts at the date the require-

ments of the new rule first apply. If determining carrying amounts as

required is impractical, then the assets are to be measured at fair

value the first date the new rule applies. Any difference between the

net amount added to the Corporation’s balance sheet and the amount

of any previously recognized interest in the newly consolidated entity

shall be recognized as the cumulative effect of an accounting change.

Management is currently evaluating the impact of this new rule on the

financial statements. See Note 8 for additional disclosure regarding

these types of entities.

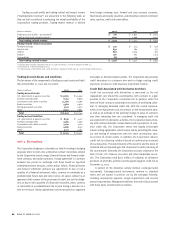

Statement of Financial Accounting Standards No. 148, “Accounting

for Stock-Based Compensation – Transition and Disclosure – an

amendment of FASB Statement No. 123,” (SFAS 148) was adopted by

the Corporation on January 1, 2003. SFAS 148 provides alternative

methods of transition for a voluntary change to the fair value-based

method of accounting for stock-based employee compensation.

SFAS 148 also amends the disclosure requirements of Statement of

Financial Accounting Standards No. 123, “Accounting for Stock-Based

Compensation,” (SFAS 123) to require prominent disclosures in both

annual and interim financial statements about the method of

accounting for stock-based employee compensation and the effect

of the method used on reported results. Under the provisions of

SFAS 148, the Corporation is transitioning to the fair value-based

method of accounting for stock-based employee compensation costs

using the prospective method. Under the prospective method, all

stock options granted under plans before the adoption date will con-

tinue to be accounted for under Accounting Principles Board Opinion

No. 25, “Accounting for Stock Issued to Employees,” (APB 25) unless

these stock options are modified or settled subsequent to adoption.

SFAS 148 will be effective for all stock option awards granted in 2003

and thereafter. Management estimates that the impact of this new

accounting will be approximately $115 million additional pre-tax

compensation expense in 2003. Prior to January 1, 2003, the

Corporation accounted for its stock-based employee compensation

plans under the recognition and measurement provisions of APB 25.

Under APB 25, the Corporation accounted for stock options using the

intrinsic value method and no compensation expense was recognized

as the grant price was equal to the strike price. Under the fair value

method, stock option compensation expense is measured on the date

of grant using an option-pricing model. The option-pricing model is

based on certain assumptions and changes to those assumptions

may result in different fair value estimates.

Notes to Consolidated Financial Statements

Bank of America Corporation and Subsidiaries