Bank of America 2002 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

48 BANK OF AMERICA 2002

For reporting purposes, the Corporation allocates its allowance across

products; however, the allowance is available to absorb all credit

losses without restriction. Table 16 represents our current allocation by

product type and Table 17 presents an allocation by component.

During the fourth quarter of 2002, the Corporation updated his-

toric loss rate factors used in estimating the allowance for loan losses

to incorporate more current information. The most significant result

was a decrease in the allowance for commercial – domestic real estate

and an increase in the allowance for commercial – domestic loans.

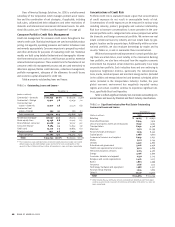

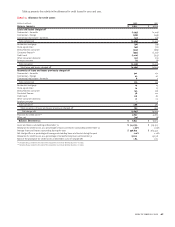

TABLE 16 Allocation of the Allowance for Credit Losses

December 31

(Dollars in millions)

2002 2001

Commercial – domestic $ 2,392 $ 1,974

Commercial – foreign 886 766

Commercial real estate – domestic 439 924

Commercial real estate – foreign 98

Total commercial 3,726 3,672

Residential mortgage 108 145

Home equity lines 49 83

Direct/Indirect consumer 361 367

Consumer finance 323 433

Credit card 1,031 821

Foreign consumer 910

Total consumer 1,881 1,859

General 1,244 1,344

Total $ 6,851 $ 6,875

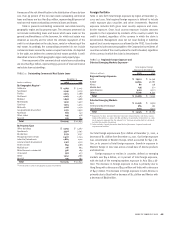

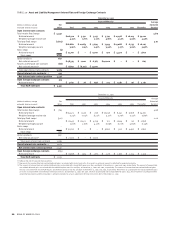

TABLE 17 Allocation of the Allowance for Credit Losses

December 31

2002 2001

(Dollars in millions) Amount Percent Amount Percent

Commercial non-impaired $ 2,807 41.0% $ 2,909 42.3%

Commercial impaired 919 13.4 763 11.1

Total commercial 3,726 54.4 3,672 53.4

Total consumer 1,881 27.5 1,859 27.0

General 1,244 18.2 1,344 19.5

Total $ 6,851 100% $ 6,875 100%

While the allowance for commercial credit losses remained relatively

flat at $3.7 billion, individual product reserves changed as a result of

updated reserve rates based on a review of performance trends and port-

folio deterioration. Commercial–domestic reserves increased $418 mil-

lion year-to-year to end at $2.4 billion on December 31, 2002. This

reflects an increased reserve rate partially offset by a $13.2 billion

decrease in loans between December 31, 2002 and December 31,

2001. Similarly, commercial-foreign reserves increased $120 million

reflecting increased reserve rates due to portfolio deterioration and

partially offset by a $3.1 billion decrease in the portfolio. Reserves for

commercial real estate-domestic loans decreased $485 million from

December 31, 2001 due to updated reserve rates based on portfolio

performance and a loan portfolio reduction of $2.4 billion since

December 31, 2001. Specific reserves on impaired loans increased

$156 million in 2002 reflecting an increase in our investment in specific

loans considered impaired which was $4.1 billion at December 31,

2002 compared to $3.9 billion at December 31, 2001. Commercial –

domestic impaired loans declined $585 million to $2.6 billion at

December 31, 2002 compared to December 31, 2001. Commercial – for-

eign impaired loans increased $854 million to $1.4 billion. Commercial

real estate impaired loans decreased $81 million to $159 million.

The allowance for credit losses in the consumer portfolio was

$1.9 billion at December 31, 2002, consistent with December 31,

2001. Growth in the credit card and residential mortgage portfolios

was offset by the application of updated performance trends that

decreased consumer real estate reserve rates. Management expects

continued growth in the credit card portfolio.

General reserves at December 31, 2002 were $1.2 billion, down

$100 million from December 31, 2001, representing approximately

18 percent of the total allowance for credit losses. Management

reviewed and adjusted the margin of imprecision and the binding

unfunded loan commitment components of the general reserve due to

updated information and factors. Partially offsetting these adjust-

ments were increases to industry concentration components.

Problem Loan Management

In 2001, the Corporation realigned certain problem loan management

activities into a wholly-owned subsidiary, Banc of America Strategic

Solutions, Inc. (SSI). SSI was established to better align the manage-

ment of commercial loan credit workout operations. The Corporation

believes that economic returns will improve with more effective and

efficient management processes afforded a closely aligned end-to-

end function. The Corporation believes that economic returns will be

maximized by assisting borrowing companies in refinancing with

other lenders or through the capital markets, facilitating the sale of

entire borrowing companies or certain assets/subsidiaries, negotiat-

ing traditional restructurings using borrowing company cash flows to

repay debts, selling individual assets in the secondary market when

the market prices are attractive relative to assessed collateral values

and by executing collateralized debt obligations or otherwise dis-

posing of assets in bulk. From time to time, the Corporation may

contribute or sell certain loans to SSI.

In September 2001, Bank of America, N.A. (BANA), a wholly-

owned subsidiary of the Corporation, contributed to SSI, a consoli-

dated subsidiary of BANA, commercial loans with a gross book

balance of $3.2 billion in exchange for a class of preferred and for a

class of common stock of SSI. For financial reporting under GAAP, the

loan contribution was accounted for at carryover book basis as

appropriate for entities under common control, and there was no

change in the designation or measurement of the loans because the

individual loan resolution strategies were not affected by the realign-

ment or contribution. From time to time, management may identify

certain loans to be considered for accelerated disposition. At that

time, such loans or pools of loans would be redesignated as held for

sale and remeasured at lower of cost or market.