Bank of America 2002 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

34 BANK OF AMERICA 2002

Assets under management, which consist largely of mutual funds, equi-

ties and bonds, generate fees based on a percentage of their market

value. Compared to the prior year, assets under management remained

relatively flat, as the decline in equity funds due to the weakened eco-

nomic environment was partially offset by an increase in money market

and other short-term fixed income funds. Client brokerage assets, a

source of commission revenue, decreased $8.5 billion, or nine percent,

compared to the prior year. Client brokerage assets consist largely of

investments in bonds, mutual funds, annuities and equities. Assets in

custody represent trust assets managed for customers. Trust assets

encompass a broad range of asset types including real estate, private

company ownership interest, personal property and investments.

Net interest income increased $32 million, or four percent,

primarily due to results of ALM activities, partially offset by the

impact of declines in loan balances and loan yields. Average loans and

leases declined $1.1 billion, or five percent.

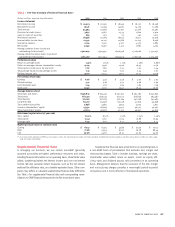

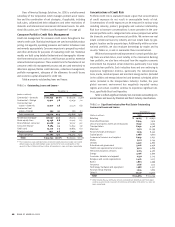

Significant Noninterest Income Components

(Dollars in millions)

2002 2001

Asset management fees(1) $ 1,087 $ 1,129

Brokerage income 435 450

■■■■■■■■■■

Total investment and brokerage services $ 1,522 $ 1,579

(1) Includes personal and institutional asset management fees, mutual fund fees and

fees earned on assets in custody.

The increase in net interest income was offset by a $108 million, or six

percent, decline in noninterest income. This decline was primarily due

to a decrease in investment and brokerage services activities, which

reflected the current market environment. Declines in personal asset

management fees and brokerage income more than offset an increase

in mutual fund fees.

Provision expense increased $197 million, driven principally by

the charge-off of one large credit in the Private Bank.

The elimination of goodwill amortization of $51 million and lower

revenue-related incentive compensation of $44 million were the pri-

mary drivers of the $64 million, or four percent, decrease in noninterest

expense. These decreases were partially offset by increased expenses

related to the growth of the segment’s distribution capabilities.

Global Corporate and Investment Banking

Global Corporate and Investment Banking provides a broad range of

financial services such as investment banking, capital markets, trade

finance, treasury management, lending, leasing and financial advi-

sory services to domestic and international corporations, financial

institutions and government entities. Clients are supported through

offices in 30 countries in four distinct geographic regions: U.S. and

Canada; Asia; Europe, Middle East and Africa; and Latin America.

Products and services provided include loan origination, merger and

acquisition advisory, debt and equity underwriting and trading, cash

management, derivatives, foreign exchange, leasing, leveraged

finance, structured finance and trade services.

Global Corporate and Investment Banking offers clients a com-

prehensive range of global capabilities through three components:

Global Investment Banking, Global Credit Products and Global

Treasury Services.

Global Investment Banking includes the Corporation’s invest-

ment banking activities and risk management products. Global

Investment Banking underwrites and makes markets in equity securi-

ties, high-grade and high-yield corporate debt securities, commercial

paper, and mortgage-backed and asset-backed securities as well as

provides correspondent clearing services for other securities bro-

ker/dealers and prime-brokerage services. Debt and equity securi-

ties research, loan syndications, mergers and acquisitions advisory

services and private placements are also provided through Global

Investment Banking.

In addition, Global Investment Banking provides risk management

solutions for our global customer base using interest rate, equity, credit

and commodity derivatives, foreign exchange, fixed income and mort-

gage-related products. In support of these activities, the businesses will

take positions in these products and capitalize on market-making activ-

ities. The Global Investment Banking business also takes an active role

in the trading of fixed income securities and is a primary dealer in the

U.S. as well as in several international locations.

Global Credit Products provides credit and lending services for

our clients with our corporate industry-focused portfolios, which also

include leasing. Global Credit Products is also responsible for actively

managing loan and counterparty risk in our portfolios using available

risk mitigation techniques, including credit default swaps.

Global Treasury Services provides the technology, strategies

and

integrated solutions to help financial institutions, government

agencies and our corporate clients manage their operations and cash

flows on a local, regional, national and global level.

Total revenue within Global Corporate and Investment Banking

declined $753 million, or eight percent, primarily driven by a decline in

trading–related revenue. Net income decreased $233 million, or 12

percent. The decline in cash basis earnings, partially offset by lower

economic capital due to reductions in loan levels, drove the 19 per-

cent decline in shareholder value added.

Net interest income increased by $265 million, or six percent, as

a result of higher net interest income from trading related activities and

the results of ALM activities. Partially offsetting this increase were

lower levels of commercial loans. Average loans and leases declined

$19.4 billion, or 24 percent to $62.9 billion.

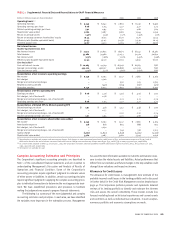

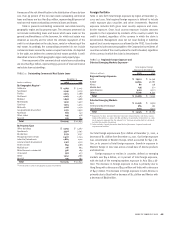

Significant Noninterest Income Components

(Dollars in millions)

2002 2001

Service charges $1,170 $ 1,130

Investment and brokerage services 636 473

Investment banking income 1,481 1,526

Trading account profits 830 1,818