Bank of America 2002 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2002 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

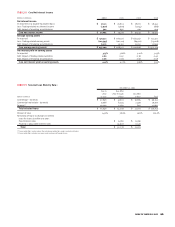

54 BANK OF AMERICA 2002

The approach described above allows the Corporation to have a dis-

cipline that anticipates and mitigates the losses from operational risks.

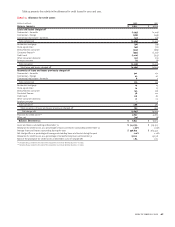

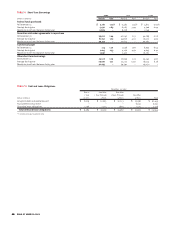

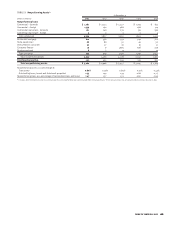

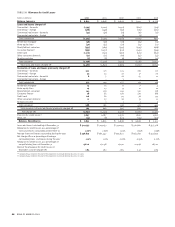

2001 Compared to 2000

The following discussion and analysis provides a comparison of the

Corporation’s results of operations for 2001 and 2000. This discussion

should be read in conjunction with the consolidated financial state-

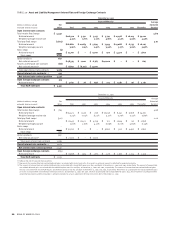

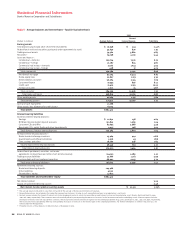

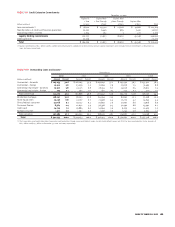

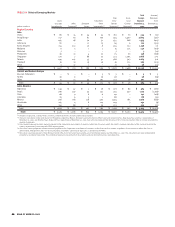

ments and related notes on pages 72 through 111. In addition, Tables 1

and 2 contain financial data to supplement this discussion.

Overview

Net income totaled $6.8 billion, or $4.18 per common share (diluted),

in 2001 compared to $7.5 billion, or $4.52 per common share

(diluted), in 2000. The return on average common shareholders’

equity was 13.96 percent in 2001 compared to 15.96 percent in 2000.

Earnings excluding charges related to the Corporation’s strate-

gic decision to exit certain consumer finance businesses in 2001 and

restructuring in 2000 were $8.0 billion, or $4.95 per common share

(diluted), in 2001 compared to $7.9 billion, or $4.72 per common

share (diluted), in 2000. Excluding these charges, the return on

average common shareholders’ equity was 16.53 percent in 2001

compared

to 16.70 percent in 2000. Shareholder value added (SVA),

which excludes exit and restructuring charges, remained essentially

unchanged at $3.1 billion. For additional information on the use of

non-GAAP financial measures and reconciliations to corresponding

GAAP measures, see the Supplemental Financial Data section begin-

ning on page 27.

Total revenue was $34.6 billion, an increase of $1.7 billion from

2000. Net interest income increased $1.9 billion to $20.3 billion. The

increase was primarily due to changes in interest rates on the

Corporation’s asset and liability positions and investment portfolio

repositioning, an increased trading-related contribution, higher

deposit and equity levels and a favorable shift in loan mix. These fac-

tors were partially offset by the impact of the money market deposit

pricing initiative and a decrease in auto lease financing contributions.

Noninterest income was $14.3 billion, a $234 million decrease.

Service charges increased $401 million, or nine percent, driven by

higher business volumes and corporate customers opting to pay

higher fees rather than maintain additional deposit balances in the

lower rate environment. Income from investment and brokerage

services increased $183 million, or ten percent, largely due to higher

corporate investment and brokerage services, new asset manage-

ment business and the completed acquisition of Marsico Capital

Management LLC (Marsico), partially offset by lower broker activity

due to decreased trade volume. Mortgage banking income increased

$81 million, or 16 percent, primarily reflecting higher origination

activity and increased gains from higher loan sales to the secondary

market, partially offset by increased prepayments on mortgage loans

as a result of the declining interest rate environment. Investment

banking income increased $67 million, or four percent, as strong

growth in fixed income origination was offset by weaker demand for

syndications, equity underwriting and advisory services. Equity

investment gains decreased $763 million, or 72 percent, driven by

the

weaker equity markets. Card income increased $192 million, or

nine

percent, primarily due to new account growth in both credit and debit

card and increased purchase volume on existing accounts.

Trading

account profits decreased $81 million, or four percent, as the

SFAS

133 transition adjustment net loss and declines in trading results in

Corporate Treasury were offset by improved trading results in Global

Corporate and Investment Banking and favorable net mark-to-mar-

ket adjustments on mortgage banking certificates and the related

derivative instruments.

The provision for credit losses increased $1.8 billion in 2001 and

included $395 million associated with exiting the subprime real

estate

lending business. Net charge-offs increased $1.8 billion to $4.2 bil-

lion, or 1.16 percent of average loans and leases, primarily

due to

credit quality deterioration in the commercial – domestic portfolio and

an increase in credit card charge-offs as well as $635 million in charge-

offs associated with exiting the subprime real estate lending business.

Nonperforming assets were $4.9 billion, or 1.49 percent of loans,

leases and foreclosed properties at December 31, 2001, a $549 million

decrease from December 31, 2000. The decrease was primarily a

result of the transfer of $1.2 billion of nonperforming subprime real

estate loans to loans held for sale as well as nonperforming loan

sales, partially offset by increases in the commercial – domestic loan

portfolio that resulted from credit deterioration as companies were

affected by the weakening economic environment. The allowance for

credit losses totaled $6.9 billion or 2.09 percent of total loans and

leases at December 31, 2001, a 35 basis point increase from 1.74 per-

cent of total loans and leases at December 31, 2000.