RBS 2006 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

RBS Group • Annual Report and Accounts 2006

138

Accounting policies continued

Financial statements

which is based on historical trends and, therefore, allows for

some increase due to changes in common law and statute.

Costs for both direct and indirect claims handling expenses are

also included. Outward reinsurance recoveries are accounted for

in the same accounting period as the direct claims to which they

relate. The outstanding claims provision is based on information

available to management and the eventual outcome may vary

from the original assessment. Actual claims experience may differ

from the historical pattern on which the estimate is based and

the cost of settling individual claims may exceed that assumed.

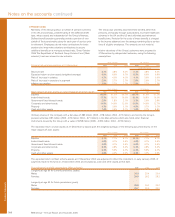

Goodwill

The Group capitalises goodwill arising on the acquisition of

businesses, as discussed in accounting policy 5. The carrying

value of goodwill as at 31 December 2006 was £17,889 million

(2005 – £18,823 million).

Goodwill is the excess of the cost of an acquisition over the fair

value of its net assets. The determination of the fair value of

assets and liabilities of businesses acquired requires the exercise

of management judgement; for example those financial assets

and liabilities for which there are no quoted prices, and those

non-financial assets where valuations reflect estimates of

market conditions such as property. Different fair values would

result in changes to the goodwill arising and to the post-acquisition

performance of the acquisition. Goodwill is not amortised but

is tested for impairment annually or more frequently if events or

changes in circumstances indicate that it might be impaired.

For the purposes of impairment testing, goodwill acquired in a

business combination is allocated to each of the Group’s cash-

generating units or groups of cash-generating units expected to

benefit from the combination. Goodwill impairment testing

involves the comparison of the carrying value of a cash-

generating unit or group of cash generating units with its

recoverable amount. The recoverable amount is the higher of the

unit’s fair value and its value in use. Value in use is the present

value of expected future cash flows from the cash-generating

unit or group of cash-generating units. Fair value is the amount

obtainable for the sale of the cash-generating unit in an arm’s

length transaction between knowledgeable, willing parties.

Impairment testing inherently involves a number of judgmental

areas: the preparation of cash flow forecasts for periods that

are beyond the normal requirements of management reporting;

the assessment of the discount rate appropriate to the

business; estimation of the fair value of cash-generating units;

and the valuation of the separable assets of each business

whose goodwill is being reviewed.

Accounting developments

International Financial Reporting Standards

The IASB issued IFRS 7 ‘Financial Instruments: Disclosures’ in

August 2005. The standard replaces IAS 30 ‘Disclosures in the

Financial Statements of Banks and Similar Financial

Institutions’ and the disclosure provisions in IAS 32. IFRS 7

requires disclosure of the significance of financial instruments

for an entity’s financial position and performance and of

qualitative and quantitative information about exposure to risks

arising from financial instruments. The standard is effective for

annual periods beginning on or after 1 January 2007.

In August 2005, the IASB issued an amendment, ‘Capital

Disclosures’, to IAS 1 ‘Presentation of Financial Statements’.

It requires disclosures about an entity’s capital and the way

it is managed. This amendment is also effective for annual

periods beginning on or after 1 January 2007.

The Group is reviewing IFRS 7 and the amendment to IAS 1 to

determine their effect on its financial reporting.

The International Financial Reporting Interpretations Committee

(‘IFRIC’) issued interpretation IFRIC 9 ‘Reassessment of

Embedded Derivatives’ in March 2006. Entities are required to

assess financial instruments for the existence of embedded

derivatives; this interpretation prohibits subsequent

reassessment unless there is a change of terms that

significantly changes the terms of the financial instrument. The

interpretation is effective for accounting periods starting on or

after 1 June 2006 and is not expected to have a material effect

on the Group or company.

The IFRIC issued interpretation IFRIC 10 ‘Interim Financial

Reporting and Impairment’ in July 2006. Entities recognising an

impairment of an intangible asset, goodwill or a financial asset

in their interim financial statements are not allowed to reverse

that impairment if the asset had recovered its value at the next

reporting date. The interpretation is effective for accounting

periods beginning on or after 1 November 2006 and is not

expected to have a material effect on the Group or company.

The IFRIC issued interpretation IFRIC 11 ‘Group and Treasury

Share Transactions’ in November 2006. Entities which buy their

own shares, or whose shareholders buy shares in the reporting

entity, in order to provide incentives to employees shall account

for those incentives on an equity-settled basis. This principle

applies also to the accounting by subsidiaries. The

interpretation is effective for annual accounting periods

beginning on or after 1 March 2007 and is not expected to

have a material effect on the Group or company.

The IFRIC issued interpretation IFRIC 12 ‘Service Concession

Arrangements’ in December 2006. Entities providing

infrastructure and services to governments under concession

arrangements shall account for each component of the

arrangement separately. Infrastructure provided under these

arrangements may be recognised as either a financial asset

or an intangible asset. The interpretation is effective for

accounting periods beginning on or after 1 January 2008 and is

not expected to have a material effect on the Group or company.

The IASB issued IFRS 8 ‘Operating Segments’ in December

2006. This will replace IAS 14 ‘Segment Reporting’ for

accounting periods beginning on or after 1 January 2009. IFRS

8 is very similar to US Statement of Financial Accounting

Standards No. 131 ‘Disclosures about Segments of an

Enterprise and Related Information’ and requires entities to

report segment information as reported to management and

reconcile it to the financial statements. Disclosures required by

SFAS 131 are included on pages 203 to 207.

US GAAP

For a discussion of recent developments in US GAAP relevant

to the Group, see Note 47 on the accounts.