RBS 2006 Annual Report Download - page 250

Download and view the complete annual report

Please find page 250 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

-

262

|

|

249

RBS Group • Annual Report and Accounts 2006

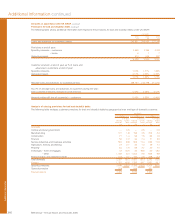

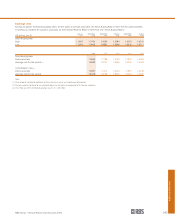

Additional information

On 26 October 2001, the President of the United States

signed into law the Uniting and Strengthening America by

Providing Appropriate Tools Required to Intercept and

Obstruct Terrorism Act of 2001 (the “Patriot Act”). The

Patriot Act was renewed on 2 March 2006 and signed into

law by the President of the United States on 9 March 2006.

The Patriot Act significantly expanded the responsibilities

of financial institutions in preventing the use of the US

financial system to fund terrorist activities. Title III of the

Patriot Act (officially, the “International Money Laundering

Abatement and Anti-Terrorist Financing Act of 2001”) is the

anti-money laundering portion of the Patriot Act. Title III

provided for a sweeping overhaul of the US anti-money

laundering regime. Among other provisions, it requires

financial institutions operating in the United States to (i)

give special attention to correspondent and payable-

through bank accounts, (ii) implement enhanced reporting,

due diligence and “know your customer” standards for

private banking and correspondent banking relationships,

(iii) scrutinise the beneficial ownership and activity of

certain non-US and private banking customers and (iv)

develop new anti-money laundering programmes, due

diligence policies and controls to ensure the detection and

reporting of money laundering. The Patriot Act requires all

US financial institutions to develop anti-money laundering

programmes. Such required compliance programmes are

intended to supplement any existing compliance

programmes for purposes of requirements under the Bank

Secrecy Act and the Office of Foreign Assets Control

Regulations.

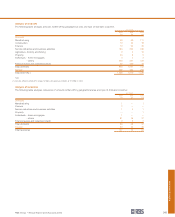

4 Other jurisdictions

Through its Corporate Markets and Wealth Management

divisions, the Group conducts business in various other

jurisdictions and is regulated by many financial and other

regulatory bodies around the world. These jurisdictions

include among others China, Hong Kong, Japan,

Singapore and Australia in the Asia Pacific region;

Abu Dhabi, Dubai and Bahrain where the Group has

branches and representative offices; and Switzerland

and the Channel Islands.

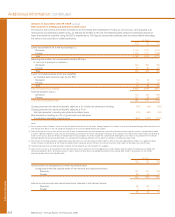

5 Regulatory developments for capital and risk

management

The Basel Committee on Banking Supervision issued new

requirements for firms’ risk weighted asset (“RWA”)

calculations in June 2004. These rules are generally

referred to as Basel 2.

In the EU, this new framework became law through the

Capital Requirements Directive and associated changes to

national laws or regulatory guidelines (e.g. the FSA’s

GENPRU and BIPRU). Within the US, regulators have the

flexibility to implement Basel 2 directly, after their final

Notice of Proposed Rulemaking. Full adoption of these

rules comes into force across the EU on 1 January 2008

and the US from 1 January 2009.

Application of Basel 2 differs between jurisdictions. The EU

is applying Basel 2 to all banks and investment firms. The

US is taking a different approach, mandating that the

largest internationally active US banks use the ‘Advanced’

approaches for credit and operational risk calculations;

other US banks will remain on the pre-existing standards or

a modified version thereof (Basel 1 or Basel 1a) or decide

to ‘opt-into’ Basel 2. Our US subsidiary, Citizens Financial

Group, is an ‘opt-in’ firm for these purposes.

The Group has submitted a request to the FSA (generally

referred to as a ‘waiver’) to adopt the Advanced Internal

Ratings-Based approach (“AIRB”) for the majority of the

Group’s EU credit risk exposures from the earliest possible

date, January 2008. In order to satisfy the requirements for

AIRB, which is the most sophisticated option available to

firms, banks are required to have risk grading, scoring and

validation approaches that calculate the Probability of

Default, Exposure at Default and Loss Given Default for

each facility. Outputs from these models, along with other

factors, such as maturity, are then used to calculate

RWAs according to regulatory formulas.

The implications of the new rules are becoming clearer.

Assuming average risk profiles, banks will require less

capital to support lending to residential mortgages and

other retail and small and medium enterprises. Good

quality corporate lending should also see a reduction in

capital requirements. Conversely banks, on average, will be

required to hold more regulatory capital for some

specialised lending and equity exposures, sovereigns and

poorer quality bank and corporate credits, although the

actual capital requirements under Basel 2 depend on a

number of factors, including collateral.

Basel 2 introduces, for the first time, an explicit

requirement to hold capital for operational risk. Of the

available options, the Group is adopting ‘The Standardised

Approach’ initially, with the objective of migrating to the

more sophisticated ‘Advanced Measurement Approach’, in

line with the US implementation. In addition, Basel 2 also

introduces two new elements – a formal supervisory review

process (Pillar 2) and more extensive market disclosures

(Pillar 3). The Group is making good progress in both

areas, in advance of formal implementation in 2008.