RBS 2006 Annual Report Download - page 247

Download and view the complete annual report

Please find page 247 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

-

259

-

260

-

261

-

262

|

|

RBS Group • Annual Report and Accounts 2006

246

Additional information continued

Additional information

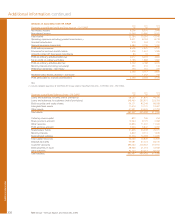

Economic and monetary environment

The Group’s earnings are affected by the economic and

monetary environment in its key markets.

The UK interest rate cycle turned in 2006, with the Monetary

Policy Committee (“MPC”) lifting the Bank Rate from 4.5% to

4.75% in August, and to 5% in November. Despite market

expectations that there would be more to come from the MPC

in 2007, longer-term interest rates were below the policy rate at

year-end, as was the case for most of 2006 (e.g. the 10-year

benchmark gilt yield was 4.74%). The Bank Rate was

increased in response to the threat that stronger economic

activity posed to the medium-term inflation outlook, and the risk

that the energy-induced increase in CPI inflation during 2006

would dislodge expectations ahead of the 2007 wage

bargaining round (CPI inflation was 3% in December 2006; the

government-set target is 2%).

Even after 17 interest rate rises over the past two-and-a-half

years, to 5.25%, monetary conditions remain fairly supportive

in the US. A weak dollar and low long-term interest rates have

partially offset the effect of a higher fed funds rate on

economic activity – though 5.25% is not high by historic

standards. The US economy grew by a respectable 3.4% in

2006, though sluggish growth towards the end of the year –

largely attributed to a sharp slowdown in the housing and

auto sectors – led markets to price in rate cuts in 2007. This

helped to exacerbate the yield curve inversion that prevailed

for most of 2006.

The European Central Bank lifted the Refi Rate to 2.25% in

January 2006. Prior to that, the Refi had been on hold at 2% for

two and a half years. Four more quarter-point increases followed,

taking the Refi to 3.25% by year-end. Markets expect this

‘normalisation’ to continue in 2007, as the improved economic

environment meant that ultra-low interest rates were no longer

needed to stimulate demand.

Exchange rates are an important driver of monetary conditions;

they also affect earnings reported by the Group’s non-UK

subsidiaries, and the value of non-sterling denominated assets

and liabilities. The pound rose by 25c against the dollar over the

course of the year, or 14%, in response to the unexpected (at

the start of 2006) increase in UK interest rates. Sluggish growth

in the US towards the end of the year, and the market’s

perception that this would lead to lower interest rates in 2007,

also put downward pressure on the dollar.

Supervision and regulation

1 United Kingdom

1.1 The regulatory regime applying to the UK financial

services industry

The Financial Services and Markets Act 2000 (“FSMA

2000”), containing an integrated legislative framework for

regulating most of the UK financial services industry, came

into force at the end of 2001. This and subsequent

amendments established the Financial Services Authority

(the “FSA”) as the single statutory regulator responsible for

regulating deposit taking, insurance, mortgage and

investment business in the UK.

Under the FSMA 2000, businesses require the FSA's

permission to undertake specified types of activities

including entering into and carrying out contracts of

insurance; managing, dealing in or advising on,

investments; mortgage business; accepting deposits; and

issuing electronic money (‘regulated activities’). The FSA

has published detailed regulatory requirements contained

in a Handbook of Rules and Guidance.

The FSA’s statutory objectives are to maintain confidence

in, and to promote public understanding of, the UK

financial system; to secure an appropriate degree of

consumer protection; and to reduce the scope for financial

crime. In achieving these objectives, the FSA must take

account of certain ‘principles of good regulation’ which

include recognising the responsibilities of authorised firms’

own management, facilitating innovation and competition

and acting proportionately in imposing burdens on the

industry.

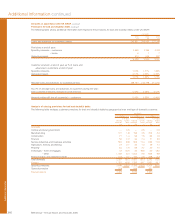

1.2 Authorised firms in the Group

As at 31 December 2006, 33 companies in the Group,

spanning a range of financial services sectors (banking,

insurance and investment business), are authorised to

conduct activities regulated by the FSA. These companies

are referred to as 'authorised firms'.

The FSA supervises the banking business of the UK based

banks in the Group, including The Royal Bank of Scotland,

NatWest, Coutts & Co, Ulster Bank Limited and Tesco

Personal Finance Limited.

General insurance business is principally undertaken by

companies in the RBS Insurance division, whilst life

assurance business is undertaken by Royal Scottish

Assurance plc and National Westminster Life Assurance

Limited (with the Group’s partner, the AVIVA Group) and

Direct Line Life Insurance Company Limited. Investment

management business is principally undertaken by

companies in the Retail Markets division, including Adam &

Company Investment Management Limited and Coutts &

Co Investment Management Limited, and in the Corporate

Markets division, RBS Asset Management Limited.