RBS 2006 Annual Report Download - page 221

Download and view the complete annual report

Please find page 221 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

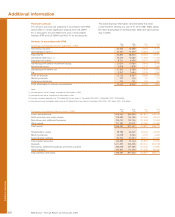

Financial statements

RBS Group • Annual Report and Accounts 2006

220

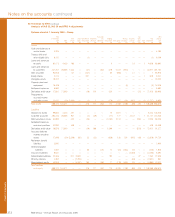

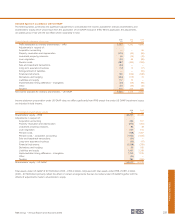

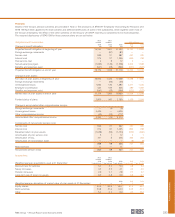

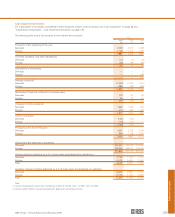

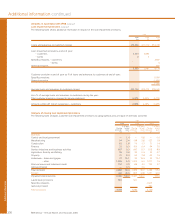

Notes on the accounts continued

47 Significant differences between IFRS and US GAAP (continued)

Recent developments in US GAAP

In February 2006, the Financial Accounting Standards Board

(“FASB”) issued SFAS 155 ‘Accounting for Certain Hybrid

Financial Instruments – an amendment of FASB Statement No

133 and 140’ which is effective for all financial instruments

acquired or issued by the Group after 1 January 2007. This

statement allows any hybrid financial instrument that contains

an embedded derivative that would otherwise require

bifurcation to be measured at fair value. The statement also

eliminates the exemption from applying SFAS 133 to interests

in securitised financial assets.

In July 2006, the FASB issued Interpretation No.48 ‘Accounting

for Uncertainty in Income Taxes – an interpretation of FASB

Statement No.109’ which clarifies the accounting for uncertainty

in taxes and addresses the recognition and measurement of

tax positions taken or expected to be taken. This Interpretation

is effective from 1 January 2007 for the Group.

In September 2006, the FASB issued SFAS 157 ‘Fair Value

Measurements’. This statement establishes a framework for fair

value measurement and prescribes extended disclosures.

SFAS 157 does not extend the scope of fair value

measurement in financial statements. The statement will be

effective from 1 January 2008 for the Group and will be

applied prospectively except for: trades in an active market

held by a broker-dealer or investment company where

blockage factors were used in determining fair value,

instruments recognised at fair value using transaction price in

accordance with EITF 02-03, and hybrid instruments measured

at fair value at initial recognition.

In February 2007, the FASB issued SFAS 159 ‘Fair Value Option

for Financial Assets and Financial Liabilities, Including an

amendment of FASB Statement No. 115’ which allows

companies to report certain financial assets and liabilities at

fair value. The statement’s objective is to reduce complexity in

accounting for financial instruments and volatility in earnings

caused by measuring related assets and liabilities differently.

SFAS 159 also establishes presentation and disclosure

requirements. The statement is effective from 1 January 2008;

early adoption is permitted from 1 January 2007 provided

certain conditions are met.

The Group is evaluating the implications of the above

standards and interpretation on its US GAAP reporting.

The FASB issued SFAS 156 ‘Accounting for Servicing of

Financial assets – an amendment of FASB Statement No. 140’

in March 2006. This statement simplifies the accounting for

servicing rights and related financial instruments used to

economically hedge risks associated with those rights. The

Group applied SFAS 156 to servicing rights recognised on or

after 1 January 2006.

In September 2006, the FASB issued SFAS 158 ‘Employers’

Accounting for Defined Benefit Pension and Other

Postretirement Plans – an amendment of FASB Statements No.

87, 88, 106 and 132(R)’. SFAS 158 requires an employer to (i)

recognise the overfunded or underfunded status of a defined

benefit plan as an asset or liability with changes in that funded

status recognised through comprehensive income; and (ii)

measure the funded status of a plan as of the year-end date. It

also specifies additional disclosures. It is effective for the

Group’s 2006 US GAAP reporting.

In September 2006, the Securities and Exchange Commission

issued Staff Accounting Bulletin No. 108 (‘SAB No. 108’)

‘Financial Statements – Considering the Effects of Prior Year

Misstatements when Quantifying Misstatement in Current

Year Financial Statements’. SAB 108 requires a company

to consider the amount by which the current year income

statement may be misstated (‘rollover approach’) and the

cumulative amount by which the current year balance sheet

may be misstated (‘iron-curtain approach’) when assessing

prior year misstatements. SAB 108 is effective for the Group’s

2006 consolidated financial statements; its adoption did not

have a material effect.