RBS 2006 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

Financial statements

RBS Group • Annual Report and Accounts 2006

216

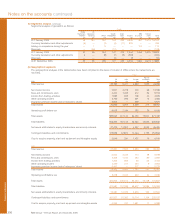

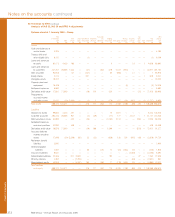

Notes on the accounts continued

IFRS

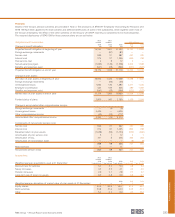

Foreign exchange gains and losses on monetary available-for-

sale financial assets

For the purposes of recognising foreign exchange gains and

losses, a monetary available-for-sale debt security is treated as

if it were carried at amortised cost in the foreign currency.

Accordingly, for such financial assets, exchange differences

resulting from retranslating amortised cost are recognised in

profit or loss.

Financial liabilities

All financial liabilities held-for-trading are classified as such

and carried at fair value with changes in fair value recognised

in net income. A financial liability may be designated as at fair

value through profit or loss.

(j) Derivatives and hedging

Gains and losses arising from changes in fair value of a

derivative are recognised as they arise in profit or loss unless

the derivative is the hedging instrument in a qualifying hedge.

The Group enters into three types of hedge relationship:

hedges of changes in the fair value of a recognised asset or

liability or firm commitment (fair value hedges); hedges of the

variability in cash flows from a recognised asset or liability or a

forecast transaction (cash flow hedges); and hedges of the net

investment in a foreign entity.

(k) Liabilities and equity

Certain preference shares issued by the company where

distributions are not discretionary are classified as debt.

(l) Consolidation

All entities controlled by the Group are consolidated including

those special purpose entities (SPEs) where the substance of

the relationship between the reporting entity and the SPE

indicates that it is controlled by the Group.

(m) Offset arrangements

A financial asset and a financial liability are offset and the net

amount reported in the balance sheet when, and only when,

the Group currently has a legally enforceable right to set off

the recognised amounts; and intends either to settle on a net

basis, or to realise the asset and settle the liability

simultaneously.

Arrangements such as master netting agreements do not

generally provide a basis for offsetting.

US GAAP

Exchange differences are included with other unrealised gains

and losses on available-for-sale securities and reported in a

separate component of equity.

Only financial liabilities that are derivatives and short positions

are carried at fair value with changes in fair value recognised

in net income.

US GAAP principles are similar to IFRS. There are however

differences in their detailed application. The Group has not

recognised any hedge relationships for US GAAP purposes

except hedges of net investments in overseas operations.

All derivatives are measured at fair value with changes in fair

value recognised in net income.

Under US GAAP, preference shares issued by the company

are classified as equity, as they are perpetual and redeemable

only at the option of the company.

US GAAP requires consolidation by the primary beneficiary of

a variable interest entity (VIE). An enterprise is the primary

beneficiary of a VIE if it will absorb the majority of the VIE’s

expected losses, receive a majority of expected residual

returns, or both.

This GAAP difference has no effect on net income or

shareholders’ equity.

Under US GAAP, debit and credit balances with the same

counterparty may be offset only where there is a legally

enforceable right of set-off and the intention to settle on a net

basis. However, fair value amounts for forward, interest rate

swap, currency swap, option, and other conditional or

exchange contracts executed with the same counterparty

under a master netting agreement may be offset as may

repurchase and reverse repurchase agreements that are

executed under a master netting agreement with the same

counterparty and have the same settlement date.

This GAAP difference has no effect on net income or

shareholders’ equity.

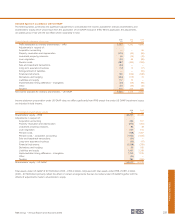

47 Significant differences between IFRS and US GAAP (continued)